Smashing Fed day

S&P 500 turned decisively lower, with only a very brief spike that got reversed within an hour. No room for bullish misinterpretation, Powell didn‘t say really anything that could feed buy the dip sentiment – he delivered. Treasuries are getting accustomed to the soft landing not turning out so soft in the future actually – yields at the long end of the curve have finally turned down while Fed tightening keeps being reflected on the short end, and junk bonds are suffering.

In all the risk-off, the dollar was unable to hold on to sharp gains both yesterday and today, and together with the crypto premarket upswing and real asset resiliency, this points to a reprieve in paper asset selling later this week. SPX 3,825 is the key level to watch today. I like the message commodities and precious metals are sending here – once it gets accompanied by miners and oil sector stocks, things would get brighter, but we are not there yet. Suffice to say that sharp downside is being decisively rejected.

Keep enjoying the lively Twitter feed serving you all already in, which comes on top of getting the key daily analytics right into your mailbox. Plenty gets addressed there, but the analyses (whether short or long format, depending on market action) over email are the bedrock, so make sure you‘re signed up for the free newsletter and that you have Twitter notifications turned on so as not to miss anything intraday.

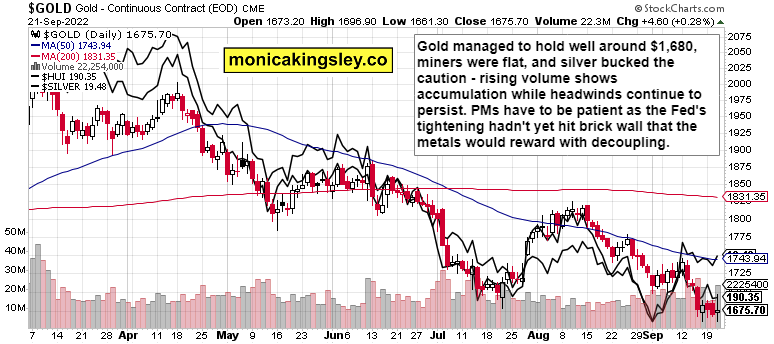

Gold, silver and miners

Silver did indeed well in the wake of FOMC, and gold looks fairly well bid here. The bears are definitely looking tired, and the direction for the next couple of days, is modestly up in the sector.

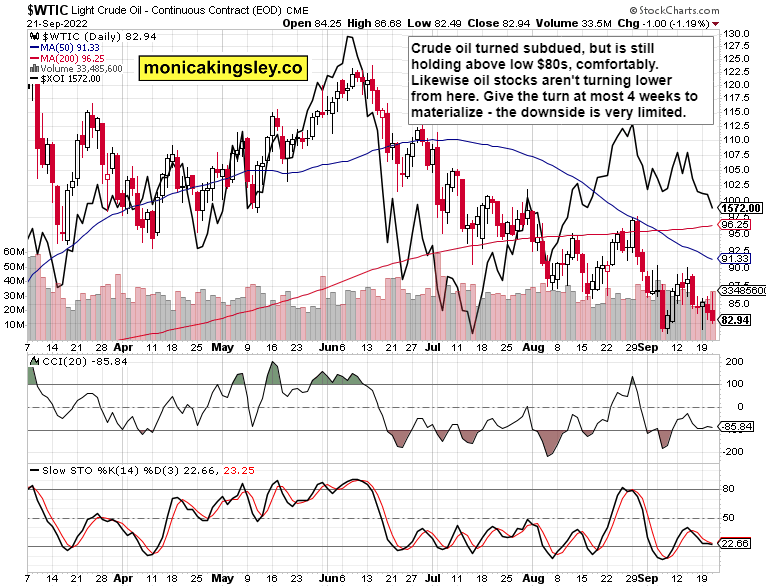

Crude oil

Crude oil is looking very fine, carving out the protracted bottom before launching higher. The downtrend is simply long in the tooth.

Copper

Copper is also fairly well bid, and odds are it would break higher from the range mentioned in the caption.

Bitcoin and Ethereum

Cryptos are leading the risk asset retracement that‘s ahead, and the volume gives both Bitcoin and Ethereum a good chance of lasting through the weekend as a minimum.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.