Silver's supply problem: Paying for ounces not yet mined

A silver developer that will not produce an ounce until 2031 just raised over $300 million and pulled in Fresnillo, the world's largest primary silver producer, because dedicated silver supply has grown so scarce that investors are now paying for ounces still in the ground.

Silver has corrected hard this year, trading near $60 after touching $121.62 in late January, though it remains well above where it stood a year ago, with a hawkish Federal Reserve and a firm dollar behind the recent slide. On a tape like that, the more revealing signal came not from the metal but from the capital markets, where a silver-mining IPO tested how investors value future supply in a market that is short of it.

At Golden Meadow®, where I publish the Silver Catalyst newsletter, the lens I apply is structural rather than day to day, and the structure of silver supply is what matters here. A new mine cannot be willed into existence, and most silver is not even mined on purpose.

An IPO That Prices Scarcity, Not Supply

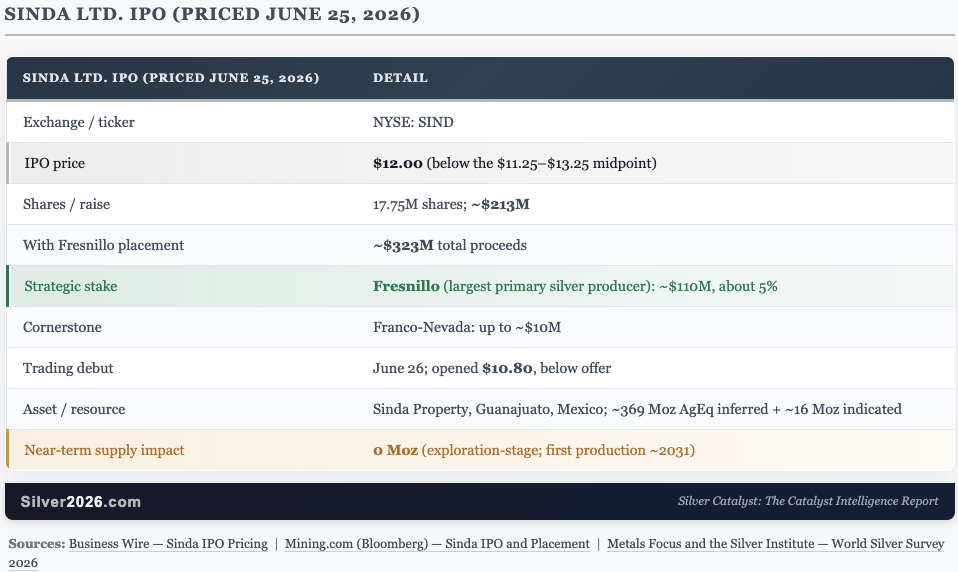

On June 25, Sinda Ltd., a Mexico-focused primary-silver developer, priced its initial public offering on the New York Stock Exchange under the ticker SIND at $12.00 a share, below the midpoint of its $11.25 to $13.25 range, raising about $213 million. A concurrent private placement from Fresnillo, the world's largest primary silver producer, added up to $110 million, lifting total proceeds to roughly $323 million, and the gold royalty company Franco-Nevada indicated interest in up to $10 million as a cornerstone investor. The stock opened at $10.80 on its June 26 debut, below the offer price, and the pricing had been pulled forward from a planned June 30 date to lock in the capital.

Strip away the tape, and the detail that matters is Fresnillo. The world's largest primary silver producer paying roughly $110 million for about 5% of a company that has never earned revenue is a strategic bet on one of the few large primary silver assets in the development pipeline. That behavior only makes sense against one number: only about 26% of the silver mined in 2025 came from primary silver mines, a new low, according to Metals Focus and the Silver Institute. The rest arrives as a by-product of mining lead, zinc, copper, and gold, where the silver is incidental and the production decision is made for another metal entirely. Primary silver, the kind a dedicated mine produces on purpose, is the scarce part, and a large standalone silver asset is rare enough to draw strategic capital.

What the IPO does not do is add supply. Sinda is exploration-stage, with no mine plan, no production, and no revenue; its resource is inferred and indicated rather than proven, and the proceeds fund drilling and an underground decline. The company targets first production around 2031. Under the development timelines the industry actually runs, where standing up a new primary mine takes well over a decade, this asset cannot touch the deficit this decade. Its near-term supply impact is zero, which is exactly why it reinforces the scarcity case instead of resolving it.

The honest counterweight is in the pricing. The deal came at the low end of its range and the stock slipped on its first day, so the market is not paying any price for silver exposure, and the broader correction clearly capped the enthusiasm. But the deal got done, and the world's largest primary producer chose to buy into future supply in a falling market. That is the signal worth keeping.

Sources: Business Wire — Sinda IPO Pricing | Mining.com (Bloomberg) — Sinda IPO and Placement | Metals Focus and the Silver Institute — World Silver Survey 2026

What this means to Silver investors

The most important thing about this IPO is the thing it does not do. It will not add a single ounce to the market this decade, and that is precisely the point. The supply side of the silver story is not that miners are choosing to hold back; it is that they physically cannot respond quickly. When roughly three-quarters of mined silver comes out of the ground as a by-product of other metals, a higher silver price does not summon more silver, because the mining decision is being made for zinc or copper or gold. And when a dedicated silver project does come along, it takes more than a decade to build. Both halves of that are visible in a single transaction.

That is why the deficit is so stubborn. For 2026, Metals Focus and the Silver Institute project a market shortfall of 46.3 million ounces, the sixth consecutive annual deficit, and new mine supply is not positioned to close it any time this decade. A pre-revenue company that just raised more than $300 million, with the largest incumbent in the business paying in, is the market acknowledging that scarcity by paying for ounces years before they can be produced.

For an investor, the takeaway is to watch where the strategic capital is going rather than where the ticker sits this week. The soft pricing and the first-day dip say the near-term tape is difficult, and that is honest. But a strategic producer and a cornerstone royalty investor backing distant, unmined silver says something about the longer arc. The longer-term case for silver rests on that structural scarcity of supply, which no single IPO can fix and this one plainly illustrates.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Przemyslaw Radomski, CFA

Gold Price Forecast

Przemyslaw Radomski, CFA (PR) is a precious metals investor and analyst who takes advantage of the emotionality on the markets, and invites you to do the same. His company, Sunshine Profits, publishes analytical software that any