Silver is finally following Gold’s lead by breaking out to the upside

Highlights:

Market Recap: The market came roaring back yesterday after starting off down on the day. At one point the Dow Jones was down more than 100 points but finished the day flat. Transports were up 1.27% and were the strongest gainers for the day. Emerging markets were also strong, rising 0.61%.

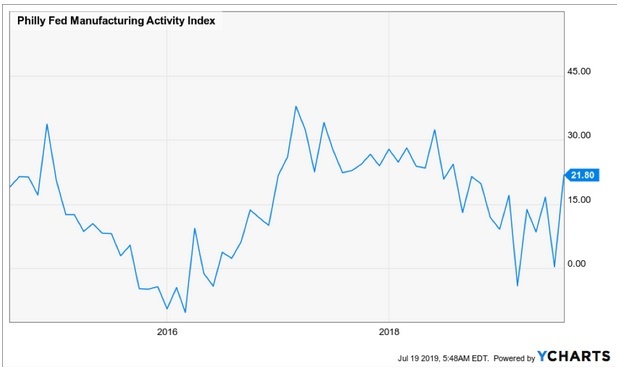

Economic Data: Philly Fed manufacturing activity index increased more than expected last month. It is up to 21.80 from 0.3 last month. This implies potential upside for broader manufacturing measures like the ISM.

Emerging Markets: Emerging markets gained 0.24% relative to the S&P 500 (EEM/SPY). Emerging markets have been relatively weak compared to the S&P 500, since the ratio peaked in early 2019. The ratio between emerging markets and the S&P 500 has been a reliable leading indicator for several years. This ratio peaked before the S&P 500 last year and bottomed in October, prior to the S&P bottoming in December. The ratio has re-tested the 2018 lows this year, diverging from the broad market. The question is whether this relationship has formed a double bottom and is set for more upside. If it has, emerging markets could be the place to be.

Silver: Silver is finally following Gold’s lead by breaking out to the upside. Silver is back above the 200-day moving average and is in a positive trend. Precious metals had a good day after the market interpreted several comments by key Fed members to imply that rate cuts would be deeper than expected.

Stocks vs Gold: Global stocks lost additional ground against Gold yesterday (VT/GLD). The trend is in favor of Gold and is suggestive of a defensive posturing among market participants. This is a negative divergence relative to the broad market.

Semiconductors: Semiconductors show little sign of slowing momentum. The sector was one of the top performers yesterday, gaining 1.19% in a flat market. Semiconductors are at all-time highs and continue to demonstrate strength.

Dividend Growth: Dividend growth is in a strong positive trend relative to the broad market (VIG/SPY). Dividend growth indices tend to express several defensive factors, like low volatility, value, and high quality. The continued relative strength in dividend growth is indicative of defensive positioning among market participants.

S&P 100: The top performer in the S&P 100 was Philip Morris, spiking over 8% on better than expected earnings. Philip Morris is in a positive trend and above its 200-day moving average. Netflix was the worst performer, dropping more than -10% on slowing subscriber growth and disappointing earnings. Netflix is in a negative trend.

Futures Summary:

News from Bloomberg:

President Trump's claim that the U.S. destroyed an Iranian drone near the Strait of Hormuz was dubbed "delusional and imaginary" by Iran. Officials said they aren't aware of any losses and even poked fun at America, saying it may have shot down one of its own drones by mistake. Even so, the International Energy Agency said it's "very worried" about recent events and the threat to energy security. Here's a look at why the U.S.-Iran conflict is coming to a head.

The New York Fed rushed out a statement after its boss, John Williams, excited markets with what looked like a call for sooner, deeper rate cuts. But it was "an academic speech on 20 years of research," not relating to the July FOMC, the bank said. The Fed's James Bullard and Eric Rosengren speak today. In a July 11 interview with Dow Jones published today, Bullard said he would support a quarter-point reduction.

Bayer is poised for a reduction of 90% or more in the $2 billion verdict it was hit with in the most recent trial over its Roundup weedkiller. A California judge is inclined to cut the awards to an elderly couple to about $250 million or lower because they're beyond legal limits. Our QuickTake looks at what's next for Bayer.

AB InBev kept hopes alive for an IPO of its Asia unit, saying the offering will still make sense so long as it gets the right valuation. It's also selling its Australian operations to Asahi for an enterprise value of about $11.3 billion. Carlton & United, whose brands include Foster's and Victoria Bitter, gives Asahi a major entree into the Australian market.

U.S. stock futures rose with shares in Europe and Asia. The dollar gained. Treasury yields came off their lows after the New York Fed tried to walk back the comments. Oil advanced to around $56 a barrel, trimming a weekly decline.

Author

Clint Sorenson, CFA, CMT

WealthShield

Managing Partner of Emerald Investment Partners, LLC and Co-Founder of WealthShield, Clint has long been dedicated to innovating and accelerating the investment landscape.