Seven fundamentals for the week: Angst rises ahead of tariff deadline and full buildup to Nonfarm Payrolls

- The fate of US tariffs on China, Mexico and Canada is critical for the next market moves.

- Nonfarm Payrolls are eyed for any potential drop in hiring after weak figures.

- The ECB is set to cut interest rates, and Fed Chair Powell weighs in toward the end of the week.

A reality show in the White House – the world is still digesting the dressing down of Ukraine's President Volodymyr Zelenskyy in the White House, but markets have to focus on other actions of US President Donald Trump: tariffs. The dramas come in a week of top-tier data. It is time to fasten your seatbelts.

1) Will Trump slap tariffs on his neighbors or will they do that to China?

The tariff decision is due by Tuesday. US President Donald Trump plans to slap 25% tariffs on all Mexican and almost all Canadian imports, with Oil being the exception, suffering only 10% duties. In addition, Trump also suggested 10% additional levies on Chinese goods – in addition to the 10% already imposed in early February.

Will a deal be reached at the last moment? That is what happened with Canada and Mexico last time after both countries pledged to do more to curb the entry of fentanyl and migrants into the US. Negotiators are scrambling to reach a deal. One option is that Canada and Mexico hit China with tariffs, strengthening the North American economy but hurting themselves. Both nations – like the US – trade heavily with China.

Markets currently believe that some deal will be reached, but that is far from guaranteed. If levies are imposed, the Canadian Dollar (CAD) and the Mexican Peso (MXN) are the immediate victims, but broad markets will also suffer. If accords are reached, these North American currencies would benefit, but broader Stocks would have other reasons to worry about. A delay in the talks beyond Tuesday cannot be ruled out.

2) ISM Manufacturing PMI to provide first hint of current vibes

Monday, 15:00 GMT. Soft data has been soft – two consumer confidence surveys missed estimates, and S&P Global Purchasing Managers Indexes (PMIs) also dropped. The most important business surveys come from the Institute for Supply Management (ISM), and the Manufacturing PMI comes early in the week.

The economic calendar points to a score of 50.8 in February compared to 50.9 in January. That is relatively upbeat, above the 50-point threshold which separates expansion from contraction. Given the other poor figures, a drop well below 50 cannot be ruled out, and would weigh on the broader mood.

Among the components, Prices Paid serves as an inflation gauge, and the Employment one is a minor hint toward Friday's Nonfarm Payrolls. However, the focus this time is on the headline – to gauge the broader US economy.

3) ADP jobs shape Nonfarm Payrolls expectations

Wednesday, 13:15. Automatic Data Processing (ADP) is America's largest provider of payslips, and has insights on employment trends. Its private-sector jobs report serves as leading indicator toward Friday's official Nonfarm Payrolls.

The weak correlation between data points results in a quick dismissal of the figures – a short-lived market reaction. Nevertheless, the data shapes expectations for Friday.

After reporting a healthy increase of 183K in January, economists expect a more modest rise of 140K. Any sub-100K figure would raise alarm bells among investors, unnerved by weak US data. An outcome above 200K would be a big beat.

4) ISM Services PMI may provide big disappointment

Wednesday, 15:00 GMT. Services is America's largest sector, and includes consumption, the backbone of the world's largest economy. While this is a survey, concerns about the resilience of the consumer also came from hard data: retail sales figures for January.

After the S&P Global Services PMI tumbled below 50 in February, economists' expectations of a small rise from 52.8 to 53 points in the ISM survey seem optimistic. Such a positive figure would send Stocks higher and weigh on the safe-haven US Dollar (USD), and a drop toward – and especially below 50 – would be a blow.

The Employment component is a significant hint for the Nonfarm Payrolls, and a drop from January's 52.3 to below 50 cannot be ruled out.

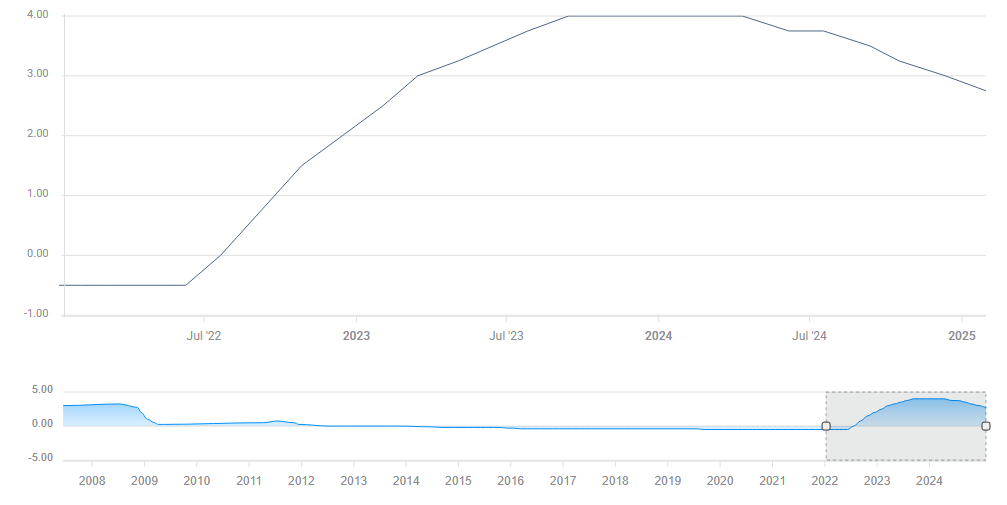

5) ECB set to cut rates on dark geopolitical backdrop

Thursday, decision at 13:15 GMT, press conference from 13:45 GMT. The European Central Bank (ECB) is set to cut interest rates by 25 basis points (bps), a move clearly telegraphed by officials. Falling inflation – both the headline and core are comfortably close to the 2% goal – serves as a good reason to cut rates.

ECB interest rates. Source: FXStreet.

However, there are also growing worries about the Eurozone economies, and especially Germany, the largest one. That would be a reduction to revive growth, a motive that is not encouraging for the Euro. ECB President Christine Lagarde's comments on the reasons for cutting interest rates would make a difference for the Euro (EUR).

In addition, the ECB announces its decision on the backdrop of the fallout between the US and Ukraine and, by extension, Europe. EU countries and the UK announced massive defense spending, which means higher debt. Are ECB officials contemplating buying bonds to lower borrowing costs? Falling inflation allows for that.

While Euro-printing would, in theory, weaken the common currency, any stimulus would boost the Eurozone economies and do the opposite, supporting the Euro. I do not expect ECB President Lagarde to make any dramatic announcement about such purchases, but she could leave the door open for such an option in response to a question from journalists.

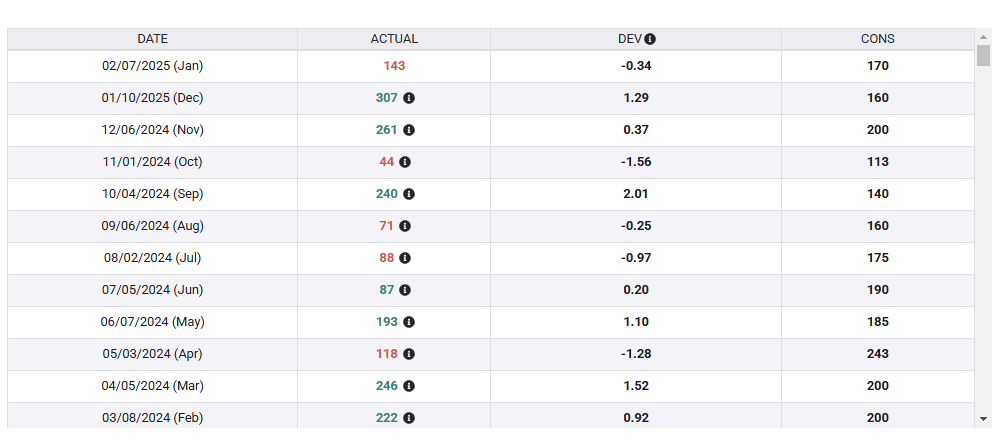

6) Nonfarm Payrolls are critical but may not show the full picture

Friday, 13:30 GMT. The "King" of economic indicators comes at a sensitive time, with signs of weakness emerging in the economy. This report includes many uncertainties. Will Elon Musk's cuts to the federal workforce show up in unemployment figures? That is unclear, as the fast-moving Department of Government Efficiency (DOGE) is moving fast, and the dust has not settled on its initial actions.

Nonfarm Payrolls surveys are held on the week including the 12th of the month, and in that period, weekly jobless claims remained low. The increase in claims was seen only in the week ending on February 21, and the rise to 242K from 220K is not especially alarming.

At the time of writing, the economic calendar points to a gain of 133K jobs in February, similar to January's 143K. The Unemployment Rate is set to hold at 4%.

US Nonfarm Payrolls. Source: FXStreet.

An increase of under 100K or a loss of jobs would scare investors, sending Stocks down and the US Dollar up. A surprising increase of 200K or higher would trigger some head-scratching, causing investors to doubt the predicting power of surveys, but it could also be temporary. March's figures could already be different.

All in all, this Nonfarm Payrolls report is unpredictable and would trigger massive volatility.

7) Fed Chair Powell has a chance to respond to the data

Friday, 17:30 GMT. The data matter, but so does their interpretation – especially from those who call the shots on interest rates. Fed Chair Jerome Powell speaks about the economy in Chicago, and he has a chance to comment on Nonfarm Payrolls and other developments.

Recent weak economic data led bond investors to price more rate cuts for 2025. Does Powell endorse this vision? If so, how much is he worried about the US economy?

If Powell raised concerns, markets would suffer, and they would also struggle with a hawkish message about the need to hold rates high to keep inflation down. The best scenario would be one of confidence in the current state of the economy and a willingness to act quickly to mitigate any downturn.

Final Thoughts

Any week under President Trump is turbulent in markets, but the mix of a tariff deadline – and top-tier data – promises high volatility.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.