Rotation – Where to?

At this moment, when I sit down at my desk, the first things I look at are the US crude and the Kospi charts. This morning, the former is looking relatively calm, with US crude consolidating its gains just below $80 per barrel, albeit with looming upside risks due to the re-escalation of tensions between the US and Iran, with no end in sight. The latter, the Kospi index, is doing poorly today—to put it politely. The Korean index is down by around 7% at the time of writing. (And I insist on the latter because volatility in the Korean market, dominated by two memory chip makers, is such that it can swing from -3% to +3% in the blink of an eye.) So, by the time I started writing, the Kospi was down by nearly 7%.

Why? ASML announced strong results yesterday and its Q2 and full-year sales forecasts blew past investor expectations. The stock initially rallied 7–8%, but gave back all of those gains to finish the session 0.41% lower in Amsterdam. Huh. The Information later reported that ASML plans price increases for its chipmaking equipment despite resistance from TSMC, a development that may explain the rapid souring of post-earnings enthusiasm. Even if AI-related demand remains robust, raising prices into slowing demand growth doesn't sound particularly appealing at a time when chipmakers are priced for perfection—and beyond.

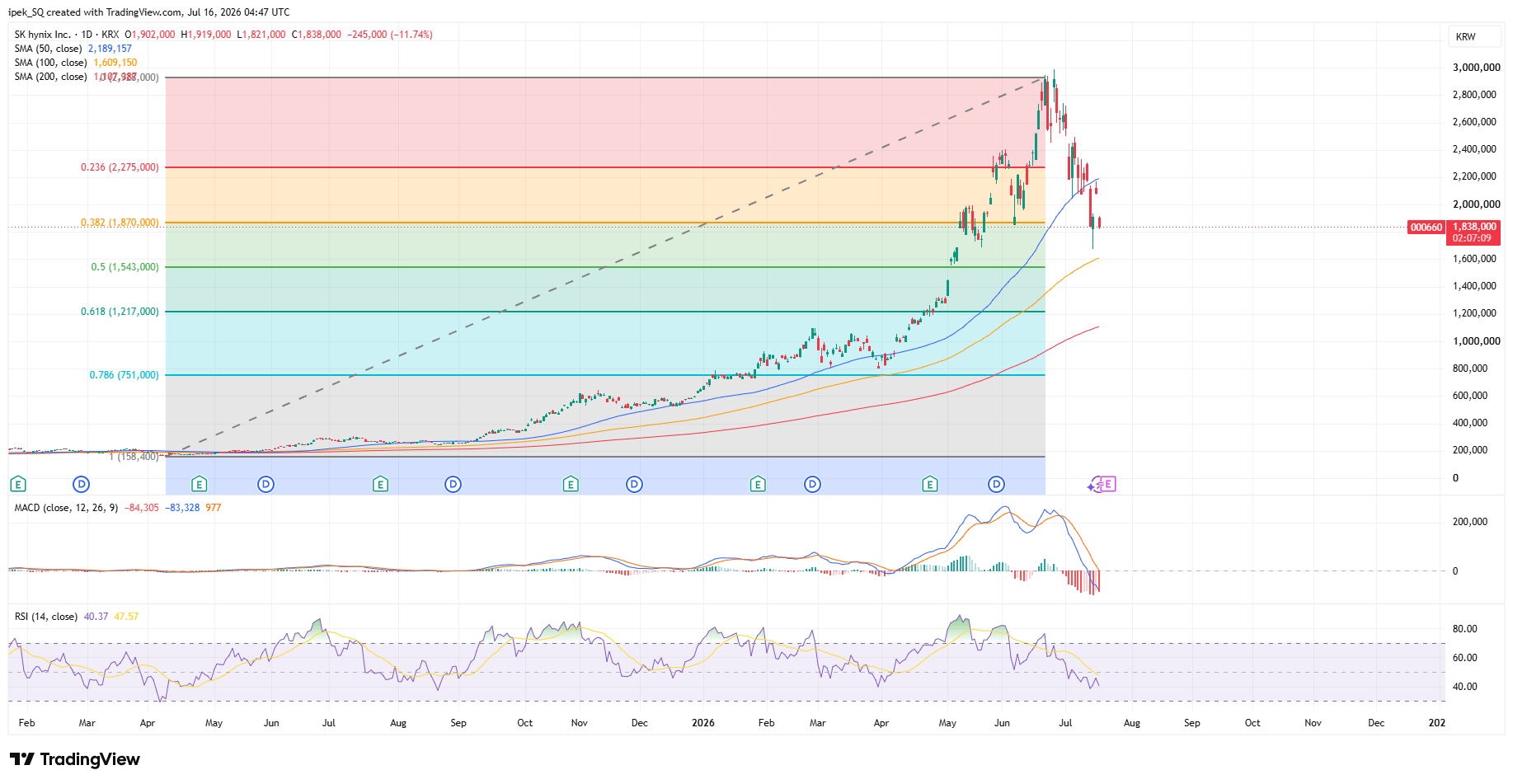

As a result, SK Hynix is down nearly 12% this morning. More importantly, it is now breaking through a key Fibonacci support level—the major 38.2% retracement of the rally from last April to this June. Entering the medium-term consolidation zone could pave the way for a deeper correction and eat into part of the roughly 50% premium that SK Hynix ADRs trade at relative to the underlying Korean shares—a reflection of the US market's superior liquidity. Alas, the highly leveraged nature of Korean chipmakers, combined with ETF, leveraged ETF flows constantly rebalancing positions, keeps both Samsung and SK Hynix firmly in the "ultra-risky" category for investors seeking portfolio stability.

Read the full article here.

Author

Ipek Ozkardeskaya

ipekScope

Ipek Ozkardeskaya began her financial career in 2010 in the structured products desk of the Swiss Banque Cantonale Vaudoise. She worked in HSBC Private Bank in Geneva in relation to high and ultra-high-net-worth clients.