2.25% and holding: Why the BoC, not the barrel, moves the Loonie

The Bank of Canada (BoC) held its policy rate at 2.25% on Wednesday and published a Monetary Policy Report (MPR) whose entire disinflation path rests on one assumption: Brent falls to $75 and stays there. That assumption was finalised on Friday and was stale before Governor Tiff Macklem reached the podium, something he conceded himself, noting that the Crude Oil futures curve has moved higher since the forecast was locked in. Around it, the Strait of Hormuz has been shut (again), Brent ripped 8.7% through $80, sanctions on Iranian crude came back, and the futures curve flipped from contango into backwardation inside two sessions.

The reflex read this week is petrodollar: Crude up, Canada bid, USD/CAD more than 1% off its early-July highs. The reflex is wrong for the same reason it was wrong in June. The Loonie is trading the rate channel, and the Bank's own report now says so in writing.

The forecast died before the podium

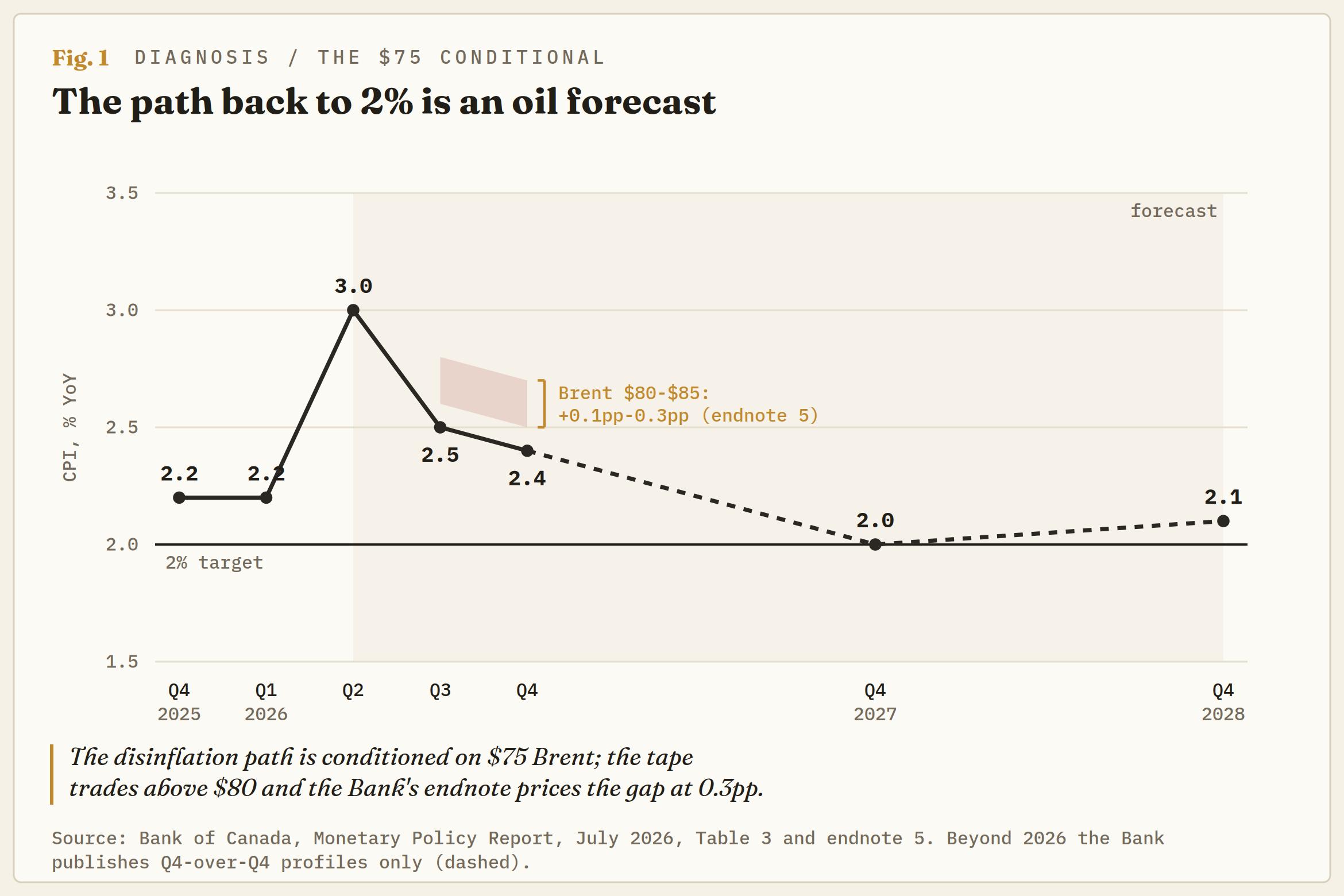

The July projection conditions everything on Crude Oil. Brent is assumed to average about $75 this quarter and drift toward $70 by the end of 2027, which allows headline inflation to ease to roughly 2.5% over the second half and land back on the 2% target in early 2027. The sequencing is damning in a quiet way: the Strait of Hormuz re-shut on a fresh escalation on July 8-9, and the Bank took its Oil assumption from the July 9 futures curve, mid-repricing, finalising the projection last Friday. By Macklem's own account, the curve has moved even higher since then. The conditioning snapshot was taken while the war was invalidating it.

The Bank even quantified its own miss in an endnote. Brent holding at $80-$85 in the coming months adds 0.1-0.3% to inflation. Q2 Consumer Price Index (CPI) inflation is already marked at 3.0% against the 2.6% pencilled in April, and the path needs 2.5% by the third quarter. On the Bank's own arithmetic, the war is currently charging up to 0.3% for the privilege of assuming it ends.

The risk chapter concedes what the base case ignores, acknowledging the Strait has shut once again in recent days while the projection keeps shipping gradually normalising. If the shape feels familiar, it should. Last week's Federal Reserve (Fed) Minutes rested the US disinflation case on Hormuz disruptions diminishing, a condition that inverted before the Minutes even printed. Two central banks inside five sessions have now published documents conditioned on a peace the war keeps declining.

Looking through, with a threat attached

What the Bank sees justifies the patience, for now. Headline inflation hit 3.2% in May after a year and a half near target, with gasoline doing nearly all the lifting; the direct gasoline effect peaks at 1.4% of inflation this quarter. Strip gasoline out, and the rate is 2.2%, and the Bank's core measures sit near 2%. Canada is running its own two-inflation split, and unlike Tokyo's version, the gap points the convenient way: The shock reads as imported, narrow, and temporary, so the Bank gets to look through it.

Macklem's caveat is where the trade lives. He was explicit that the tolerance is conditional: that the longer Oil stays elevated, the greater the risk it bleeds into other prices, and that the Bank will not allow a Crude shock to harden into persistent inflation. From an institution this measured, that is a threat.

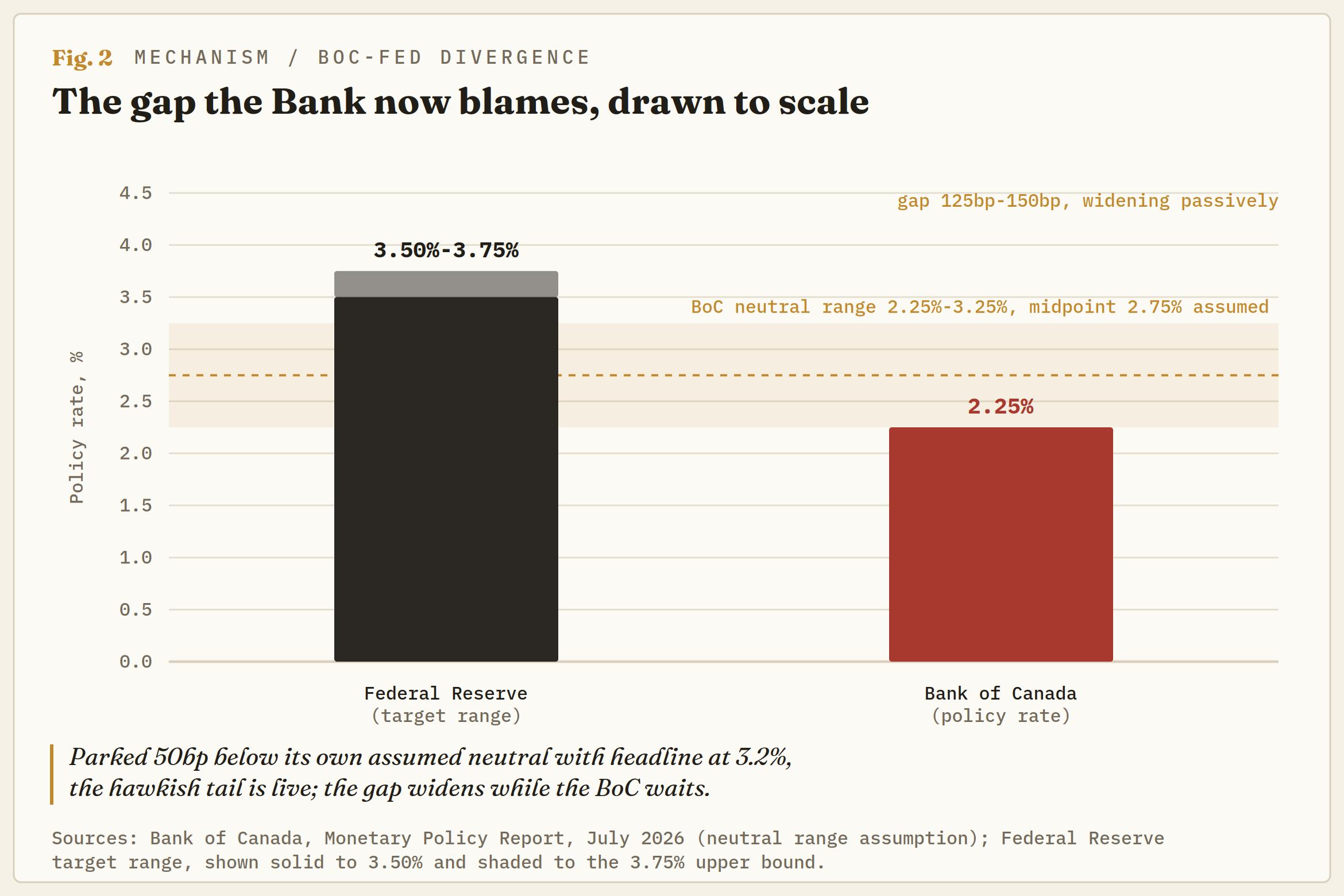

Now weigh the threat against the stance. The MPR assumes the neutral rate sits at the midpoint of a 2.25%-3.25% range. The policy rate is parked on the exact floor of that range, 50bps below the Bank's own midpoint assumption, while headline inflation runs 3.2%. On headline math, the real policy rate is roughly -1%. Strip the euphemism and the stance is mildly stimulative during a war-driven inflation spike, justified entirely by the $75 conditional. If the conditional fails, the distance from here to merely neutral is two full hikes, and the hike tail the market has been carrying stops looking like a tail.

The same report documents the channels that would break it. The war-cost annex tracks fertiliser, propylene, diesel and jet fuel as elevated, and the outlook keeps food inflation high on fuel and fertiliser input costs, with war passthrough peaking at 0.4pp on CPI in early 2027. Readers of our Fed coverage will recognise the mechanism: the fertiliser-to-food lag is the same one that turned the Federal Open Market Committee (FOMC) dot plot hawkish. The BoC charts the passthrough in one chapter and assumes it fades in another.

The Bank blames the rate gap now too

Buried in the financial conditions pages is a sentence Loonie watchers should frame. The Canadian Dollar has depreciated to around 71 cents US, and the report attributes the move partly to the widening spread between US and Canadian government bond yields. Not the barrel. The yield spread. The petrocurrency framing is absent from the central bank's account of its own currency, which is roughly where this desk landed three weeks ago.

The tape agrees. Through the spring war spike, with Brent north of $100, the Loonie refused to rally, and when Crude fell in June the Loonie fell with it. A currency that shrugs at triple-digit Brent is not a petrocurrency.

The gap itself keeps widening passively. The Fed is holding at 3.50%-3.75% with at least one 2026 hike still priced in money markets, the BoC holds at 2.25%, and the MPR itself notes US policy-rate pricing has risen since April. That leaves 125bps to 150bps of differential that stretches every time the US curve backs up while Ottawa stands still. By late June, money markets had begun leaning toward a BoC hike as soon as December. Today's hold, delivered alongside a dead Oil conditional, keeps that tail alive rather than killing it.

The barrel discounts twice

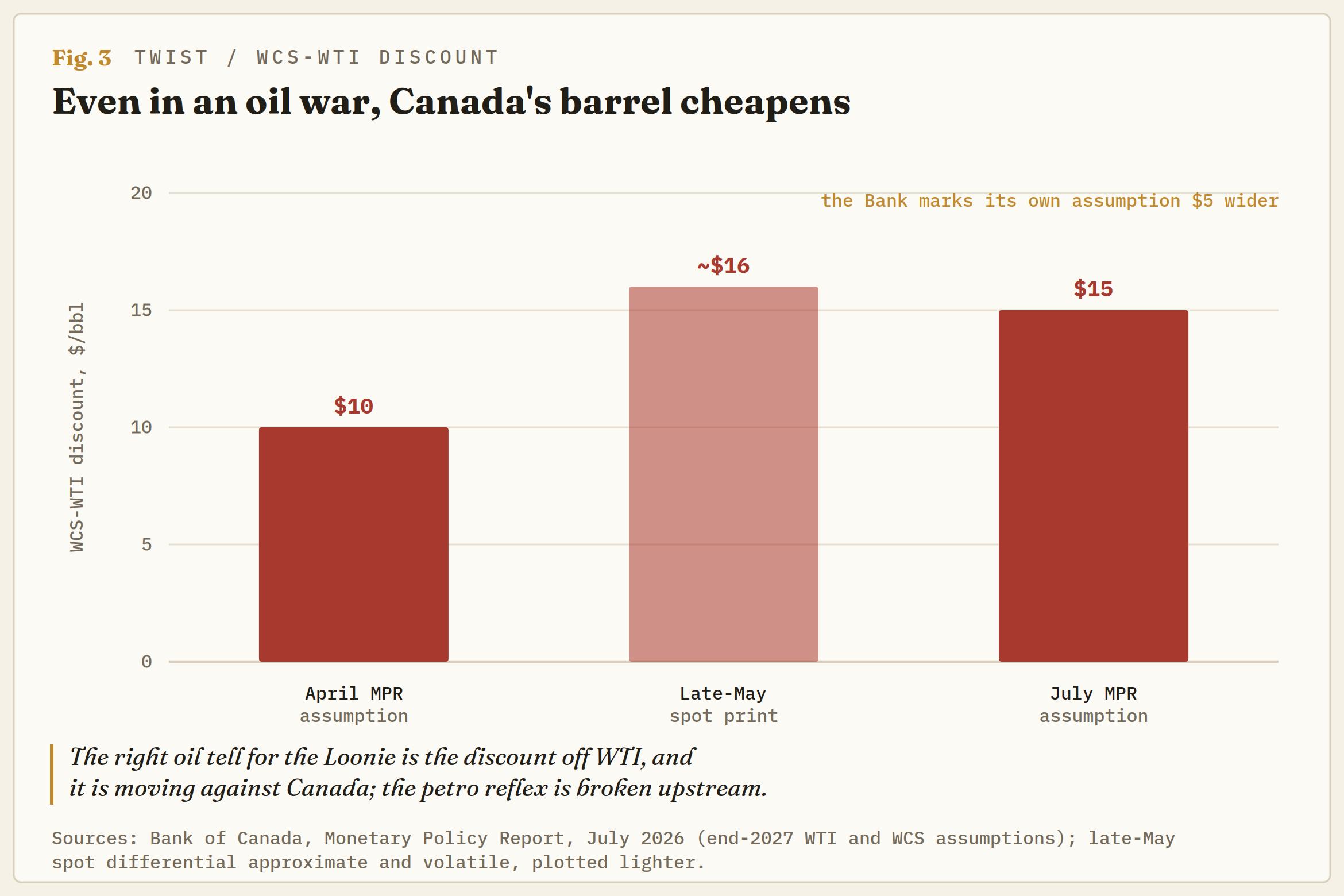

The July round also quietly widened the one Oil number that matters most for Canada. The Bank now assumes West Texas Intermediate (WTI) at $65 and Western Canadian Select (WCS) at $50 by the end of 2027, a $15 differential and $5 wider than the April projection carried. The reasons are unglamorous: Venezuelan heavy barrels returning to US Gulf refiners, strong US crude exports, and falling US commercial inventories propping WTI while Canada's grade cheapens against it.

The market got there first, with the discount printing near $16 in late May. Canada's netback is squeezed from both ends: The benchmark trades below what the war headlines imply, and the discount off the benchmark widens. Even in an Oil war, Canada's barrel is losing relative value, and the wider discount is now baked into the central bank's own projection.

This is why the correct Oil tell for the Loonie remains the WCS-WTI discount rather than the flat price. The discount says the petrodollar reflex is not resting. It is broken at the wellhead.

A rebound bought with one-offs

The hold leans on a growth story, and the growth story earns scepticism. Second-quarter gross domestic product (GDP) is estimated at 2.5% annualised after a flat first quarter, and Macklem argued the sources of growth are broadening. Read the Bank's own decomposition before buying it: the rebound largely reflects temporary factors unwinding, the first quarter's drop in government spending reversing, auto plants returning from retooling shutdowns, and Oil and gas investment snapping back with prices.

Households were also paid to spend. Second-quarter consumption got a lift from one-time transfers, a federal groceries benefit top-up and Quebec's special payment for groceries and energy. Beneath the bounce, wage growth runs 2.7% on the Bank's preferred microdata measure, unemployment sits at 6.5%, and the output gap is still estimated between -1.5% and -0.5%. Slack everywhere you look, which is why 2026 growth was marked down to 0.7% from April's 1.2% even as 2027 nudged up to 1.8%.

The rebound is real enough to justify holding and far too thin to absorb hikes. That tension cuts both ways for the currency: It is the bind that would make a forced hike so damaging, and it’s the strongest argument that the December tail eventually prices back out. An economy this soft is the standing risk case against chasing the Loonie bid.

Trading the conditional, not the barrel

USD/CAD trades near 1.4050, more than 1% off its early July highs above 1.4200 and back below 1.4150, the November 2025 peak the pair broke through on the way up in June. The pullback tracks the escalation almost candle for candle, which is exactly why the petrodollar read is tempting and exactly why it is incomplete. The same barrels that broke the Bank's conditional fattened the BoC hike tail. The Loonie is being bid on its own rate expectations, and Oil is merely the messenger.

The lean is a fight between two clocks. While the BoC sits 125bps-150bps below the Fed, the multi-month lean stays with USD/CAD upside, and 1.4000 is the line in the sand. The pair holds it on a closing basis, and the June uptrend off the 1.3550 launchpad is intact, with a reclaim of 1.4150 turning the past week into a failed breakdown and putting the July highs above 1.4200 back in play. The cycle extreme just shy of 1.4800 from February 2025 stays on the map as context, not a target.

The counter is the conditional itself. Every session Brent holds above $80 feeds the December-hike tail and squeezes the gap at the margin. A daily close below 1.4000 would say the market is pricing the conditional's failure in earnest, dropping the pair back into the spring range, where 1.3900 is the first marker and the 1.3550 launchpad is the full retrace objective.

The catalysts stack in order: The Hormuz tape itself, Canada's June CPI print, the first that can show the war moving from the pump to the grocery aisle, and the July 28-29 FOMC, where the other side of the gap gets its say.

Macklem promised the Bank will not let elevated Oil become persistent inflation. At 2.25%, on the floor of its own neutral range, the promise costs nothing to make. The first inflation print that shows fertiliser and freight in the food aisle presents the bill, and it is the Loonie, not the barrel, where the market decides whether the Bank pays it.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.