Robust high inflation story is still on track: Expectations of a hawkish Fed?

Outlook: If the new Omicron variant was driving traders to safe havens, why did the dollar tank on Friday? The only sensible explanation is fear that the variant would hold back the hand of the Fed. We took a quick look at the CME FedWatch tool and see very little change from Friday or a week ago except that second hike, where last week 25.2% expected it and as of 7:15 am today, it’s down to 19.2%. We honestly don’t know what this means but this week is chock-full of Fred speakers and we guess they will affirm that the robust growth/high inflation story is still on track and therefore so are expectations of a hawkish Fed.

About that robust growth: the Atlanta Fed’s latest Q4 GDPNow forecast is back to 8.6% (from 8.2%) due to a rise in real gross private domestic investment growth (from 10.3% to 12.5%), and a tiny gain in net exports, with offsets real personal consumption spending growth from (9.2% to 7.9%).

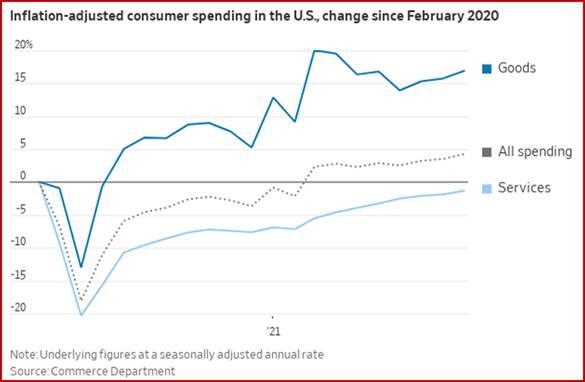

Separately, personal consumption spending in Q3 went up more than expected (1.7% from 1.6% in the earlier GDP estimate), and of course, the holiday season is upon us. Black Friday spending was already reported hog-wild and we will get fresh data on that in a day or so. The two big questions–does private capital pull back again because of the new variant, and do people keep spending like drunken sailors?

We say they keep spending, which appears to be the chief driver of inflation. A ray of light--the supply chain problem may have a short life and be ending in about 6 months. That’s the forecast embedded in the St. Louis Fed’s expected change in delivery times compared to the previous month for manufacturing firms. The 6-months in the future chart shows a level near historical levels (zero). In other words, manufacturers expect the supply chain bottlenecks to be smaller over the next six months, New York being the exception. Alas, the St. Louis Fed is depending on folks who had not heard of the Fifth wave or Omicron at the time they delivered their forecasts….

From the limited news about Omicron so far, it looks like it’s terribly more transmissible but has mild symptoms. It’s too soon to say, but we guess people in the US are fed up with restrictions and will not go back, no matter what, including a rise in cases. We have already seen that even when a virus kills people, a large percentage refuse vaccination and refuse inactivity. If this variant doesn’t kill, so much the better. So we may not get a chop in growth at the same time we do get a Fifth Wave. (Feel pity for Mr. Powell, who has to thread that needle.)

The lack of lethality of the new variant probably means a rapid and full recovery in just about everything–equities, oil, the dollar.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat