Risks Surrounding the U.S. Economic Outlook

Upside and Downside Risks to Our Base-Case Scenario

As discussed in our most recent Monthly Economic Outlook, we assume that trade policy tensions between the United States and China will continue for the foreseeable future. Under this assumption, we forecast that real GDP growth in the United States will slow in coming quarters as some businesses delay capital expenditures due to uncertainty over trade policy (top chart). Due to this economic deceleration and to some apparent changes in the way officials at the Federal Reserve think about monetary policy, we now look for the Federal Open Market Committee (FOMC) to cut rates 50 bps by the end of 2019 (middle chart). But these forecasts are predicated, at least in part, on the trade policy assumption that was previously noted. But what happens if our assumption about trade policy turns out to be not valid?

Let's start with the upside scenario in which President Trump and Chinese President Xi agree to a trade deal when they meet later this month. In that event, the tariffs that the two countries have already imposed on each other likely would be rescinded. With trade policy uncertainty removed, the stock market likely would rally and business fixed investment spending probably would accelerate. The resulting improvement in the economic outlook would mean that the case for more accommodative Fed policy would not be as compelling. In that event, we would probably remove the 50 bps of rate cuts that currently are included in our base-case scenario.

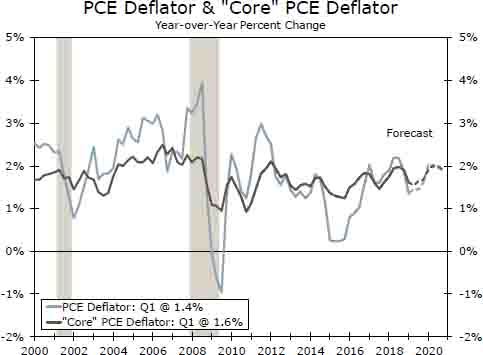

But what happens in the downside scenario in which President Trump and President Xi fail to find any common ground? In that case, higher American tariffs on approximately $300 billion of Chinese imports likely would go into effect in coming months. Tariffs on Chinese goods to date have been concentrated on industrial goods. But the remaining tariffs would fall largely on consumer goods, and we estimate that consumer price inflation would rise by about 1/2 percentage point above our base-case forecast (bottom chart). This rise in inflation would erode growth in real income, which would lead to slower growth in U.S. consumer spending. In short, real GDP growth next year would be noticeably slower than our base-case forecast. We believe the Fed would look through any tariff-induced rise in prices as being a one-off increase in the price level. In our view, the FOMC would respond to the growth-weakening effects of the tariff increase by slashing rates by more than the 50 bps that are included in our base-case forecast.

We would not be inclined to forecast an outright U.S. recession under this downside scenario. But there is a more pessimistic scenario still. Potential tariffs on auto imports from the European Union and Japan, which have been delayed until at least this autumn, could eventually go into effect. Auto tariffs in conjunction with tariffs on all Chinese goods would impart a sizeable shock to the economy that could potentially lead to recession.

Author

Wells Fargo Research Team

Wells Fargo