Risk assets exposed if the pandemic gets worse

The UK’s economy shrank a little more than expected in the first quarter – the 2.2% plunge was the joint worst since 1979. Of course, it will be dwarfed by the Q2 drop, with April already printing 20% lower. Meanwhile China’s PMI data showed a slight improvement and Japan’s industrial production plunged over 8%. Does any of this tell us much as investors and traders? In normal times, yes of course, as it might make a difference of a few points on the margins, but in the time of coronavirus there is an awful lot of noise around the data which makes it a lot more challenging, as well as of course all the stimulus, which muffles the notes that the data is trying to sound. Boris Johnson will launch an FDR-like New Deal infrastructure package today to distract us from the harsh reality of rising unemployment and ongoing restrictions on our liberties.

US Treasury yields declined as Federal Reserve chair Jay Powell said the outlook for the economy is ‘extraordinarily uncertain’. In prepared remarks for today’s Congressional hearing alongside Treasury Secretary Steve Mnuchin, Mr Powell said output and employment remain ‘far below their pre-pandemic levels’, adding: ‘The path forward for the economy is extraordinarily uncertain and will depend in large part on our success in containing the virus.’ He also noted that ‘a full recovery is unlikely until people are confident that it is safe to reengage in a broad range of activities’. San Francisco Federal Reserve President Mary Daly said it’s too early to tell and is just ‘watching the data’. Aren’t we all.

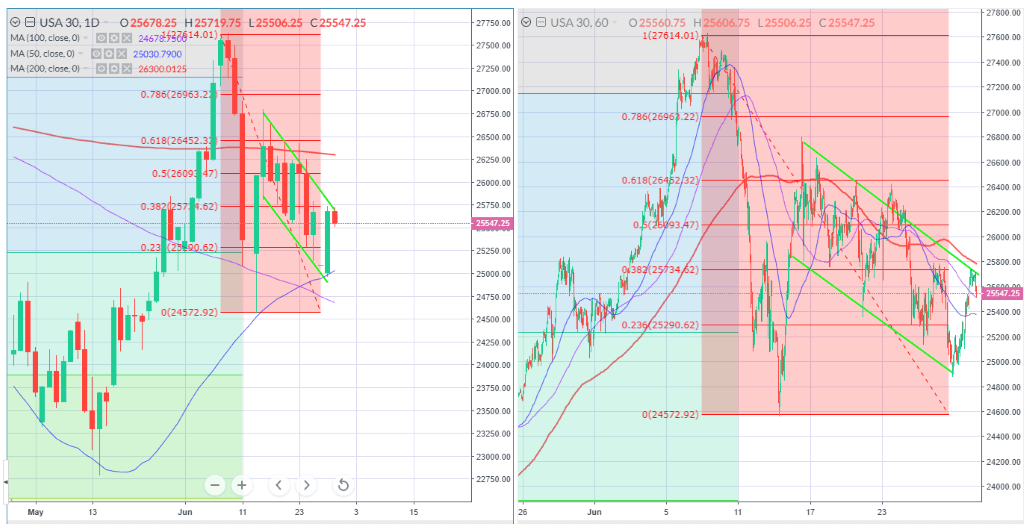

Stocks rallied on Monday despite a wobbly start, as US pending home sales jumped the most on record in May, whilst Boeing surged 14%, heaping dozens of points on the Dow as it restarted test flights on the 737 MAX aircraft yesterday. But as I keep stressing, this is a very rangebound market. The S&P 500 rose 1.5% but is caught between the 38.2% and 50% retracement of the pullback in the second week of June. The Dow added more than 2% but couldn’t even achieve the 38.2% line. Whilst indices are still trading this range, there is a downside bias evident lately and emerging down trend channels as we’ve made a couple of lower highs and lower lows. If this trend strengthens it could gain enough momentum to retest of the June lows. Indeed, during cash equity trading hours the last 5 sessions has produced a lower low and lower high on the S&P 500. Valuations still look too high and based on a far-too-optimistic view of an earnings rebound in 2021 and does not account for permanent productivity and demand destruction. Of course stimulus is making a big difference here, but risk assets are exposed if we see the pandemic get worse from here. World Health Organisation boss Tedros said the worst is yet to come. Cases across states like Arizona, Texas and Florida continue to surge and look to be completely out of control. A short, sharp pullback is a very real possibility.

Nevertheless, it’s been a solid month and an exceptionally strong quarter. US equities have enjoyed their best quarter in 20 years, whilst stocks in Europe have fared pretty well too as investors participated in the rebound off the March lows. It’s mirrored elsewhere in risk assets – copper is up a fifth, but is slightly weaker for the year. For instance, the S&P 500 is up 18% QTD, but down 5% YTD. The FTSE 100 is up almost 10% QTD, but down over 17% YTD.

On the open on Tuesday, European stocks were mixed and lacking direction as they traded either side of the flatline. The FTSE 100 was trading around the 50% retracement of the June pullback and took a little hit as Shell downgraded its oil outlook and warned it will need to take up to write down the value of its assets by as much as $22bn. This follows a similar move by BP, which moved lower apparently on the Shell read-across.

Chart: Dow tests 50-day SMA support, downtrend starts to gain momentum.

Elsewhere, gold was supported around $1770 but slightly below the recent 8-year high as the flag pattern starts to near completion following the leg up on Friday. Needless to say, we can look to US real rates and 10yr Treasury Inflation Protected Securities (TIPS) dipping to –0.7%, a new seven-year low. Across the curve real rates are more negative than they have been a decent while.

Crude oil recovered the $39 handle but has failed to ascend all the way to $40 and has peeled back this morning. The near-term rising trend is offering support but the double top still exerts its influence and may well result in a further pullback to $35.

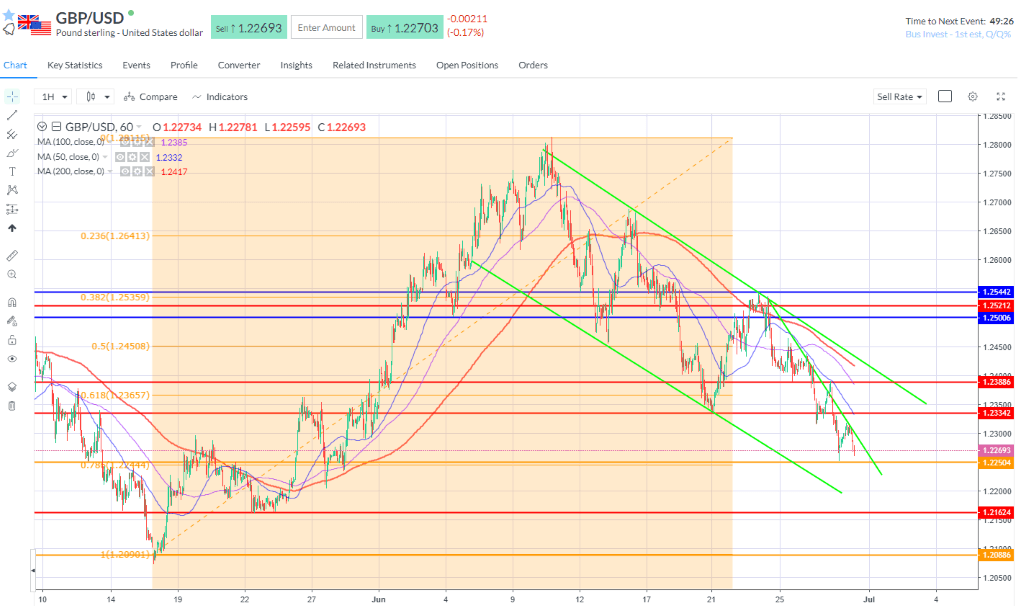

In FX, the dollar continues to find bid and the dollar index is making a nice little move off its lows still in a strong uptrend channel but is just running into horizontal resistance around the 97.65 area – breakout could see 98 handle again in short order. The downtrend dominates for cable as the pair continued south down the channel to test 1.2250. Whilst this held, the failure to recover 1.23150 on the swing higher may call for a further decline to the 1.22 round number support, and thence our old friend 1.2160 may come into play.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.