Restoring balance in the post-pandemic economy

Summary

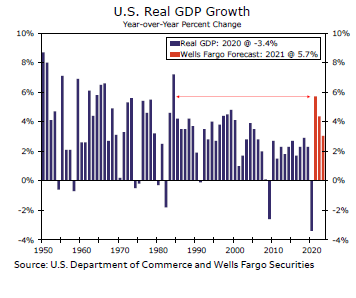

The global economy continues to be whipsawed by the ups and downs of the pandemic. The initial collapse in economic activity was followed by sharp rebounds as economies reopened amid strong policy support. But economic growth has waxed and waned as new case counts continue to actuate, and the imbalances that have arisen have led to an almost-forgotten phenomenon: inflation. We project that U.S. real GDP will grow 5.7% in 2021 before downshifting to about 4.4% next year. But we also forecast that consumer priceinfiation will exceed 5% in 2022, a rate that hasn't been experienced since 1990. Many foreign economies likely will post solid rates of economic growth, but with relatively high rates of inflation in 2022 as well. Will economies be able to restore some semblance of "balance" in the foreseeable future?

Introduction and summary

Regaining Balance in the Wake of Unprecedented Demand and Inadequate Supply

The global economy has been materially affected by the COVID pandemic over the past two years. The nosedive in economic activity in spring 2020, which was caused by the lockdowns that most governments imposed, was followed by sharp rebounds as economies reopened amid unprecedented policy support. But economic growth has waxed and waned in many economies as upswings and retreats in new COVID cases have come and gone. Meanwhile, meaningful increases in aggregate demand coupled with gummed-up supply chains have led to the highest inflation rates that many economies have experienced in a generation. How do economies and balance again?

There are some tentative signs that balance is starting to be restored, at least on the demand side of the economy. Because many parts of the service economy were more or less shut down during the darkest days of the pandemic, consumer spending on goods became supercharged. For example, the level of U.S. retail sales currently stands about 21% above its pre-pandemic peak. During the previous cycle, it took almost nine years for retail spending to rise by a similar amount above the previous peak. But real spending on durable goods, which was pulled significantly forward, has declined by more than9% on balance since its peak in March. Meanwhile, real spending on services, which usually accounts for about two-thirds of consumer spending, continues to make steady gains.

But restoring balance in the U.S. economy will not happen overnight due to the outsized imbalances that developed. We project that real GDP grew at a blistering pace of 5.7% this year, which would be the strongest year of economic growth since 1984 (Figure 1). Looking forward, we forecast that real GDP growth will downshift to about 4.4% in 2022, which is still an above-trend rate of growth. However, supply chains remain clogged, and they likely will not be restored to "normal" anytime soon. As we discuss further in the U.S. Economic Outlook, we believe that inflation will continue to be an issue for the U.S. economy through much of 2022, and we forecast that the overall rate of U.S. CPI inflation will average 5.3% next year, which is markedly higher than the consensus forecast. We project that real GDP grew at a blistering pace of 5.7% this year and will downshift to about4.4% in 2022.

The recent emergence of the Omicron variant clouds the outlook, but we do not believe it will lead to wide-scale lockdowns à la the early days of the pandemic. There seems to be little public support for the reimposition of onerous restrictions. But the variant poses a downside risk to our GDP growth forecast and upside risk to our inflation forecast, which are diflcult to quantify until we know more about its virulence. Under our base-case scenario, which we detail in our U.S. Monetary & FiscalPolicies section, we look for the Fed to begin tightening monetary policy in the second half of 2022. Although monetary policy tightening will not unclog supply chains, it can help ensure that inflationary expectations, which could lead to even higher inflation in coming years, do not become unmoored. We forecast that the FOMC will hike rates by a cumulative 50 bps in the second half of next year followed by 75 bps more tightening over the course of 2023.

Author

Wells Fargo Research Team

Wells Fargo