Research: Sweden in political crisis

Monday, a majority in the Swedish Parliament (Riksdag) supported a non-confidence vote against the Prime Minister Stefan Löfven and his Social democrat-Green coalition government.

The constitution now gives the PM one week to choose between three options: 1) investigate the chances of forming a new government which is backed by the Riksdag 2) call for a snap-election (which then must be held within three months) or to resign. In the latter case, the task of investigating chances to find support for a new government is handed over to the speaker.

The speaker can present up to four propositions for a new Prime minister candidate. If all are rejected by Parliament (or if the speaker comes to the conclusion that a government with support from the Riksdag) can’t be found, the speaker is obliged to call for a snap election.

At this stage it is difficult to say where this will end because there are several complicating factors. One being that a snap-election hasn’t happened since 1958. No one knows if and how a snap election only about a year in advance of the next regular election (September 2022) could affect voter turnout and therefore the election result.

We don’t think this will have much of a market impact, in particular not for rates. It took four months after the September 2018 election before a new government was in place, the market didn’t take much notice. The fiscal policy framework which stipulates strict budget discipline is supported by a broad majority in Parliament, so no risk of a U-turn there. Perhaps one can see some (minor) risk premium in the SEK until this is resolved.

Why is this complicated?

Background: It took four months to form a new government after the 2018 election. Finally after an agreement with the Centre party and the Liberals on a list of 73 specific -" essentially liberal -" reforms (the January agreement), the latter two parties agreed to accept Stefan Löfven as Prime minister of a Social democratic -" Green party coalition government. Demand from the Centre Party and Liberals was also that the Left party must be excluded from political influence. This was a complicated factor from the outset since the government also needed the (passive) support from the Left party to reach majority.

What has happened: One of the issues in the 73-point list was a reform of the housing market (newly constructed rental apartments) which would give landlords a stronger position in setting rents without negotiations with the tenants’ representatives. This was a red line for the Left party which has made clear that if the government brings forward such a proposal they will pull their support. That happened today.

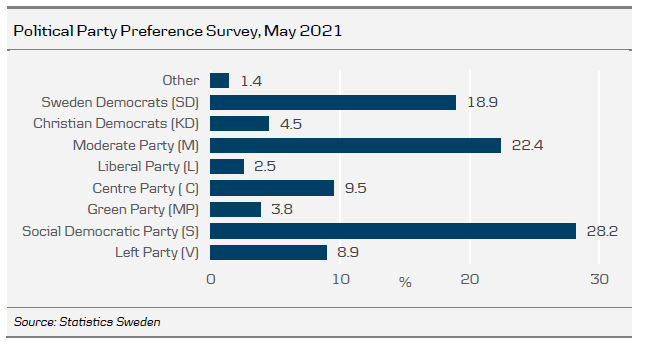

What makes things more complicated: In order to be represented in the Riksdag, a part must get at least 4% of votes in an election. Since the 2018 election, the Liberals have almost imploded (the latest poll shows 2.5%) and are very likely to lose their seats in Parliament in a snap-election. But even if they miraculously would remain in Parliament, the situation has changed since the party leader has explained that the Liberal no longer would support Stefan Löfven after an election. Also, the coalition partner (Greens) are also dangerously close to falling short of 4% according to polls.

In the meantime, the speaker has made clear that he will not allow it to take so long to get a new government in place as it did in 2018, this increases the risk of a snap-election but also suggests that the period of political uncertainty will be relatively short-lived.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.