Removing the Noise – Macro Themes to Watch H2 2019 - What to Expect

The U.S. economy is certainly maturing, and many economists and asset managers are of the opinion that the economy will continue to mature for couple more years. During this period, the world’s largest economy is expected to grow at a decelerating rate, and this will have reverberating effects on the global economy as well. On the back of lower economic growth assumptions, many strategists including David Kelly of J.P. Morgan, Alicia Levine of BNY Mellon, and Paul McCulley who worked with PIMCO, are all predicting a rate cut or even couple of rate cuts in 2019. However, these strategists continue to believe that cutting rates to support growth at this point in time would lead to adverse effects in the future.

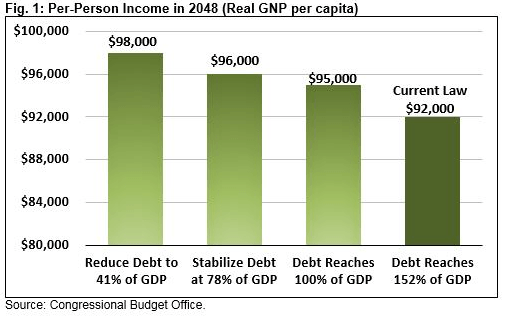

Government indebtedness is increasingly becoming a worry in our opinion, even though a fear of default is uncalled for. Economic growth achieved through a higher level of debt is not entirely sustainable and could hurt the global economy if a crisis hits within the next 5 years as predicted by many economists. A higher level of indebtedness leads to higher debt service costs in the future, and this would result in a lower level of income available for governments. This is true for corporations and individuals as well. As debt-to-GDP continues to rise, the real income available per person would drastically decline in the future.

(Source – Committee for a Responsible Federal Budget)

Assuming more debt to service existing debt is only a temporary solution in our view, and we believe this will aggravate the situation in the future and lead to a lower rate of economic growth.

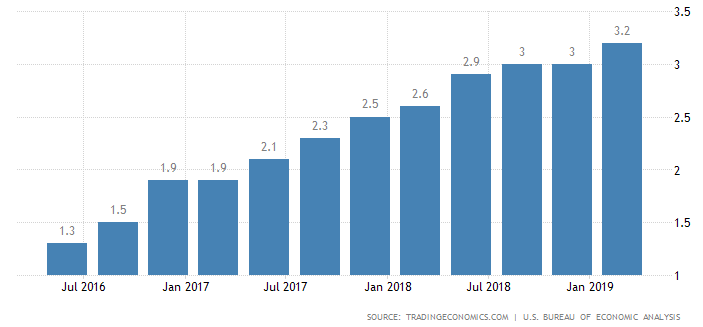

In the first quarter of 2019, the U.S. economy outperformed analyst estimates and grew at an annualized rate of 3.2%. The reported rate of growth easily outperformed the growth expectations of economists polled by the Dow Jones, which was reported at 2.5%. The significant outperformance of expectations came in as a result of higher than expected decline in the trade deficit and robust growth of inventories.

Annualized GDP growth rate in the U.S.

(Source – Trading Economics)

Notably, personal spending in the U.S. rose 1.2% in the first quarter, which was again an improvement from analyst estimates. However, the growth rate of consumer spending remains at a low level. An increase in spending on services and nondurable goods was offset by a decline in spending on durable goods.

The stellar rate at which the American economy grew in the first quarter has certainly revived the hopes of higher than expected economic growth for 2019. However, it is likely that the economic growth rate will decelerate in the future and settle to a more sustainable level. In fact, the World Bank expects the U.S. economy to grow at a substantially lower rate in 2019 in comparison to the last couple of years, and further expects the economic growth rate to decelerate continuously through 2021.

(Source – World Bank)

The U.S. economy is certainly maturing and the rate hikes that continued since the latter half of 2015 are having its toll on the economic growth of the country. The quantitative easing policies adopted by the Fed since the fallout from the financial crisis helped the U.S. economy recover through 2015, and the monetary policy tightening that followed was a response to the higher than desirable inflation rates seen in the country. Even though the Fed Chair, Jerome Powell, has confirmed the patient stance of the Fed regarding future interest rate hikes, investors should not leave out the possibility of further rate hikes as a higher than expected growth in the economy would prompt the Federal Open Market Committee (FOMC) to hike rates once again. This will not only affect economic growth in the U.S, but also other developed and emerging countries including China, Eurozone countries, and Japan as the U.S. is the primary trading partner of these countries.

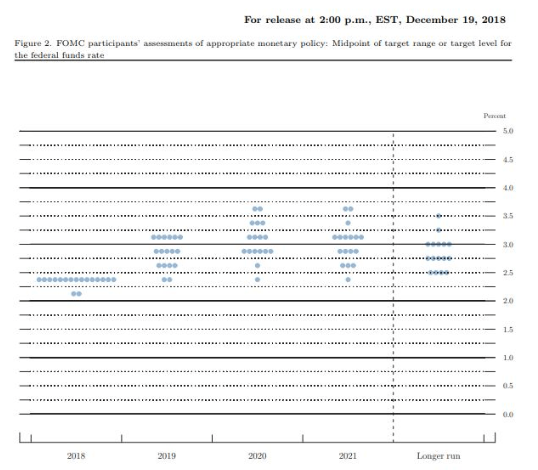

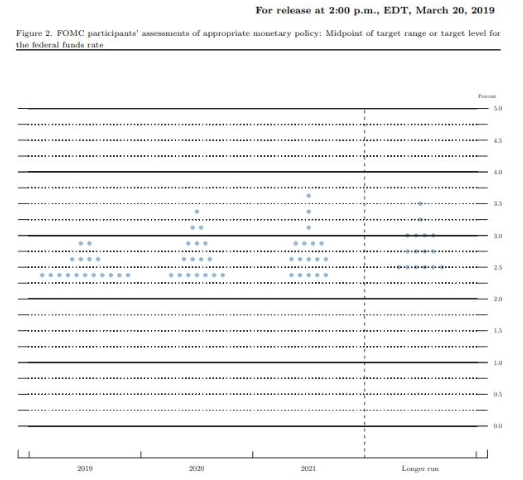

More than 2 rate hikes were expected in 2019, but as things stand today, the Fed sees no rate hikes in 2019 anymore. This confirms the belief of the Fed that economic growth will remain at a suppressed rate, and that inflation will remain at a desirable level as well.

The dot plot as of December 2018

The dot plot as of March 2019

(Source – Bloomberg)

Clearly, the Fed is expecting no upside pressure for inflation in the remaining periods of 2019. However, economic activities in the country could receive a boost from the expected trade deal with China, and this might lead to higher than anticipated inflation as well.

The core Personal Consumption Expenditure Index (PCE) remains well below the target rate of 2% as well.

(Source – Bureau of Economic Analysis)

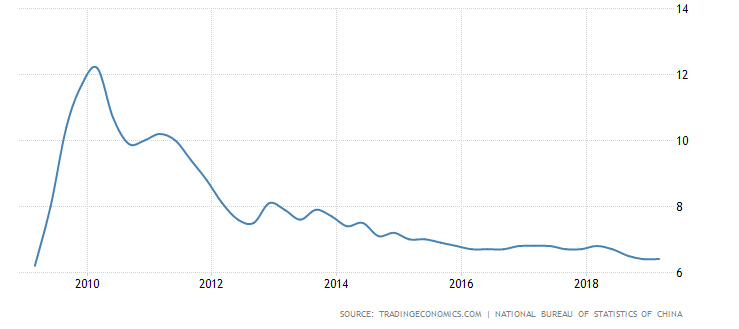

The Chinese economy on the other hand gained widespread attention in the latter half of 2018 as many renowned economists predicted a significant slowdown in the Chinese economy in 2019 and beyond. In the first quarter of 2019, Chinese banks issued a record $865 billion of new loans, and investors are optimistic of further growth of the Chinese economy supported by the massive infusion of funds by Chinese banks through loans to consumers and businesses. On the contrary, we believe that the boost provided by the infusion of capital would be short-lived in China, and the benefits will slowly but surely diminish in the next couple of quarters, leading to a slower rate of economic growth in the remainder of the year. This thesis is consistent with our belief that the global economy will slowdown in 2019 and beyond, driven by a plethora of geopolitical and macro-economic reasons.

The International Monetary Fund (IMF) was quick to reassess growth projections in China, following the higher than expected loan growth in Q1. As per the most recent World Economic Outlook report published by the IMF, the Chinese economy is now projected to grow at 6.3% in 2019, an upgrade from the previous projection of 6.2%. In any case, the Chinese economy will grow at a much lower rate than it grew in the last decade, and in fact the economic growth rate has already declined.

GDP growth rate in China

The Chinese government is doing everything in its capacity to provide a boost to the economy, which was imminent in its boost to the federal budget in 2018.

The yield curve in China has flattened considerably over the years, which provides another reason of concern to investors. The yield curve inverted in the U.S. in March, which is an ominous sign as yield curve inversions have preceded the last 7 economic recessions in the country.

We believe the Chinese economy is near its peak, so is the U.S. economy. Higher than expected economic growth that lasts a short period is a feature of a maturing economy, and investors should not be thrilled to see better than expected numbers and assume that growth will continue to break records for many years to come. Rather, it’s better to stay cautious and remain open for new developments.

In conclusion, countries around the world including the U.S. and China are focused on providing a necessary boost to economic activities in their countries through monetary policy softening. However, I believe the positive effects of lower rates for purchasing power will be completely offset by rising asset prices. The real interest earned on savings could drastically decline as well, which is one of the primary risks every investor should be considering at present.

Global risk assets are now worth over 5 times the size of the global economy, and this confirms the belief that asset prices have already gone through the roof and sky-rocketed over the last decade.

Despite the patient stance of the Fed, and the optimism surrounding a rate cut in the investing community, I do not believe a rate cut is imminent in 2019 but, this is probably the next future action of the FED . Nevertheless, because of the actions of the FED and the state of the global economy, I believe the USD should climb higher especially against EM currencies.

Gold prices have gained traction in the last several months as well, and the rally could continue further moving forward.

Finally, it’s worthwhile to remember that every cycle comes to an end, and it’s irrational to believe that the global economy will continue to grow at breakneck speeds.It’s not a question of whether the cycle would come to an end, but rather, a question about when the cycle would come to an end. Various geopolitical and macro-economic developments can put an end to this business cycle, as it has been the case throughout the history.

Author

Fotis Papatheofanous, MBA

Fotis Trading Academy

Fotis, as you would expect from his name is the key trainer at the Fotis Trading Academy. Fotis is a highly reputed, driven and successful Global Macro Trader and Portfolio Manager.