Reforming eu economic governance: The start of a marathon

The European Commission has relaunched a comprehensive review of the economic governance framework of the European Union. This initiative is necessary considering the impact of the Covid-19 pandemic on public finances as well as the investment needs in the context of green and digital transformation. The review process comes with several challenges: an agenda that is particularly broad, the inclusive nature of the debate, involving many stakeholders, and, as far as fiscal governance is concerned, the necessity for EU member states to strike a balance between committing to policy discipline whilst keeping national fiscal policy leeway. Given the state of public finances in most EU countries, sensible fiscal rules are necessary to gradually create the much-needed fiscal room for maneuver.

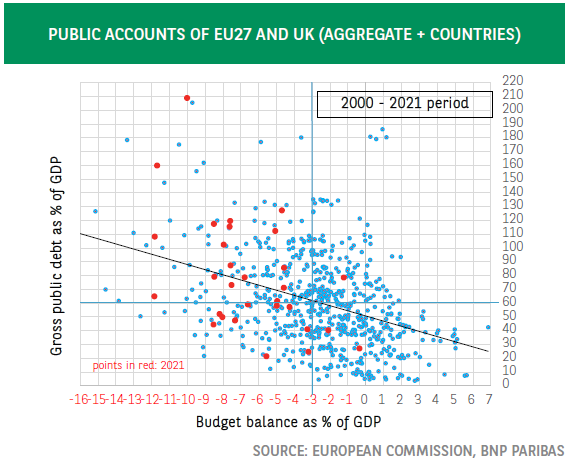

The Stability and Growth Pact (SGP) – the budgetary pillar of the Economic and Monetary Union but with the application for the whole EU without exception –, has been adopted in 1997. Since then, it has been amended on a number of occasions. Although it consists of a complex set of rules, the focus in the public debate on the SGP tends to be on the Maastricht criteria of a budget deficit of 3% of GDP and public debt of 60% of GDP.

Judging by the annual performance of EU member states on these two dimensions, it is clear that very often the objectives have not been met (see chart). Quite understandably, this is particularly the case at the current juncture. The Covid-19 pandemic necessitated major fiscal efforts, which led to the activation in March 2020 of the general escape clause. This allowed countries to deviate from the budgetary paths that had been defined pre-Covid-19. The SGP is scheduled to be restored in 20231, which calls for an assessment and possibly a revision of the fiscal rules.

This will be part of a comprehensive review of the economic governance framework of the European Union that was recently relaunched by the European Commission. This initiative faces multiple challenges. One, finding a balance between meeting public investment needs – which will remain high for years to come in the context of the green and digital transition- and the necessity to reduce budget deficits to create fiscal space in order to have sufficient leeway for a counter-cyclical discretionary fiscal policy when the next recession hits. Two, the agenda is particularly broad, covering a large number of topics, grouped in 11 open questions2. Three, the review process will be based on an inclusive debate with many stakeholders3. This should be welcomed but it may reduce the time available to reach a political agreement. Inviting citizens and organizations to submit their contributions to the debate is reminiscent of the ‘ECB listens’ events that were organized by the ECB in the preparation of its strategic review. However, the debate on economic governance and fiscal governance is far more complex than the one on monetary policy strategy, with the former having an important distributional dimension – levels of taxation, income transfers, expenditures – as well as an intertemporal angle (the conditions for debt sustainability). Finally, as far as fiscal governance is concerned, EU member states will need to strike a balance between committing to policy discipline whilst keeping national fiscal policy leeway. In its list of 11 questions, the European Commission raises the question about the possible role of financial sanctions, reputational costs, and positive incentives. It is probably the most difficult question to tackle and agree upon. Yet, given the state of public finances in most EU countries, sensible fiscal rules are very much necessary to gradually create the much-needed fiscal room for maneuver.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.