Recovery is happening, but... Is it fast enough?

Equity markets look a tad bleary-eyed and hungover this morning after a bit of binge. Call it exuberance, but the strong rally in China stoked by the state-run press left markets with only way to travel on Monday and now the price has to be paid. Meanwhile we continue to monitor the rising cases in the US and an emerging spat between the UK and China over Hong Kong and Huawei which simply evinces the fact that Covid is reshaping the world.

European stocks handed back some of Monday’s gains on the open on Tuesday after the strong start to the trading week pushed the FTSE 100 back above 6200. Energy and financials led the fall but all Stoxx 600 sectors dropped in the first hour of trade. Tokyo and Hong Kong fell, but shares in China continued to rally on very high volumes.

Wall Street also rallied after the bump up in China, with the Nasdaq hitting a fresh all-time high, but yesterday had a feel of a frothy move based on nothing but fumes. The put/call ratio for the S&P 500, which reflects market positioning and sentiment, has fallen to levels that have in the past indicated a correction is in the offing. Speculators have also lately aggressively cut their net long positioning on S&P 500 futures. The upcoming earnings season will be crucial, and investors may see earnings estimates reduced given that many companies simply scrapped guidance, which could call for a rethink of valuations. Indices continue to track the ranges of June, so until we break out in either direction the pattern is one of a choppy but sideways market as investors try to figure out the balance on offer between reopening & stimulus vs cases & permanent economic damage from falling confidence and increased saving.

Recovery is happening, but is it fast enough: German industrial production rose 7.8% in May, but the figure was short of the 11% that was expected. Meanwhile, BMW Q2 sales in China rose from the same period a year ago, which might be down to the pent-up demand from the shutdown in the country in Q1, but nevertheless indicates a decent pace of recovery in the world’s second largest economy.

The UK’s Halifax mortgage survey showed prices fell for a fourth month in a row in June, but activity levels are rebounding, with enquiries up 100% from May. It’s too early to tell if this rebound can be sustained - a truism across the economic data prints we see right now.

Meanwhile we got another dose of salt from Raphael Bostic, the Atlanta Fed president, who warned of signs the US recovery is levelling off. Indeed, the headline nonfarm payrolls number last Thursday masks a lot of ills. Not least of which, permanent job losses are on the rise: while the number of unemployed classed as being on temporary layoff decreased by 4.8m in June to 10.6m, following a decline of 2.7m in May, the number of permanent job losers continued to rise, increasing by 588,000 to 2.9m in June. Additionally, the data for the June report was collected largely before the spike in cases in several of the big economically important states like Texas and California. Dr Fauci said the US is still ‘knee-deep’ in the first wave.

The Reserve Bank of Australia left interest rates on hold at the record low 0.25%, but noted households and businesses are worried about the state of the economy after the jump in cases in Victoria raised doubts about the country’s handling of the outbreak, which had been assumed to be as good as New Zealand. “The downturn has been less severe than earlier expected,” RBA governor Philip Lowe said in a statement, but added that “uncertainty about the health situation and the future strength of the economy is making many households and businesses cautious, and this is affecting consumption and investment plans”. Scott Morrison’s government will deliver a statement on July 23rd outlining further support on the fiscal side.

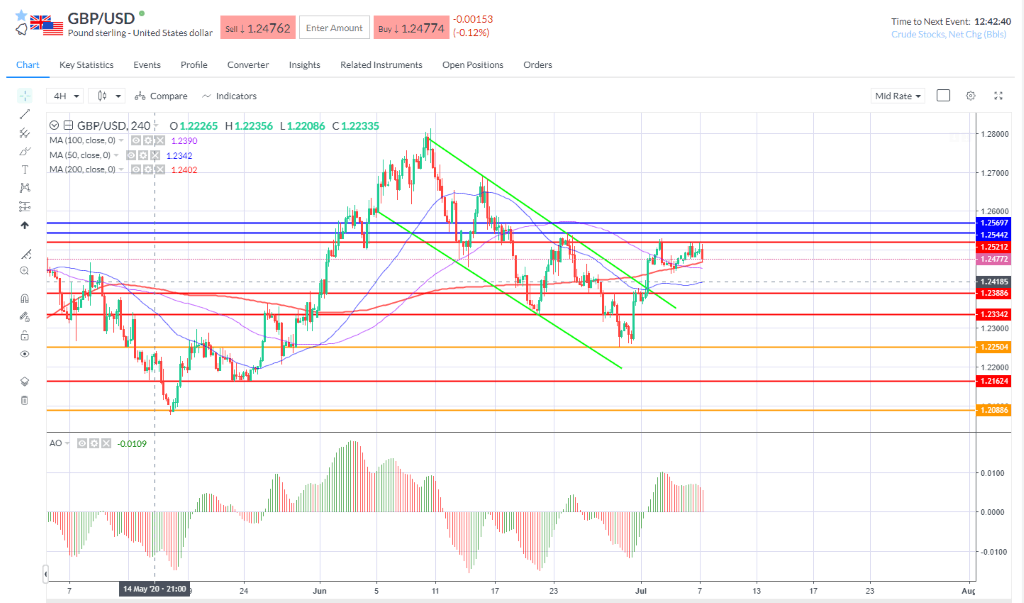

Elsewhere, gold’s bullish bias remains intact as it consolidates around $1780 and may be preparing for a fresh run towards $1800 – first up it needs to clear the seven-year highs at $1789. WTI (Aug) is steady at $40 for now and in FX we see the majors still trading within recent ranges as the dollar recovers a little from Monday’s risk-on sell-off. EURUSD failed to break the June swing high at 1.1345 yesterday and has pulled back towards the middle of the bullish pennant. GBPUSD has also drifted lower after several failed attempts in the last session to clear the 1.2520 resistance, finding some immediate support on the 200-period SMA on the 4-hr chart. Sterling has that RoRo feel.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.