Rates spark: Sterling rates most likely to fall, Dollar rates more likely to rise

US labour market data could trigger another leg higher in dollar rates but we doubt their euro peers will follow, barring a much stronger inflation print today. Hawkish BoE pricing is vulnerable to a pushback.

US labour market indicators take centre stage

The start of the week is proving a constructive one for bonds. It seems the feel-good factor felt by markets, after the White House and House leader McCarthy reached a deal to raise the debt ceiling over the weekend, was short-lived. The deal is due to be voted on today by the lower chamber and later this week by the Senate. We think expectations are for the bill to pass, which also means the market-moving potential of a successful vote is limited. The same cannot be said of any delay on procedural grounds, although more would be needed to shake the market’s optimism.

Instead, the focus should now focus on more fundamental matters for interest rates valuations, namely this week’s two labour market releases. Today sees the publication of the ‘JOLTS’ job openings report, followed on Friday by the non-farm payroll report (which also includes wages). Rate cut expectations last month received a shot in the arm when job openings unexpectedly dropped but payroll data continues to go from strength to strength and we expect investors will be wary of chasing bond yields lower into the report as a result.

We expect investors will be wary of chasing bond yields lower into Friday's job report

10Y US Treasury yields are more than 60bp away from the peak they reached in early March, prior to the regional banking crisis. The Fed has been pushing a more hawkish line disappointed by the lack of progress on the inflation front, but end-2023 Sofr futures still price a rate that is 50bp below the early March peak. At least so far, this doesn’t feel like a wholesale reappraisal of the market’s macro view although a more forceful Fed communication at the 14 June meeting, with potentially a hike and a higher end-2023 median dot, could push us closer to this year’s peak in rates.

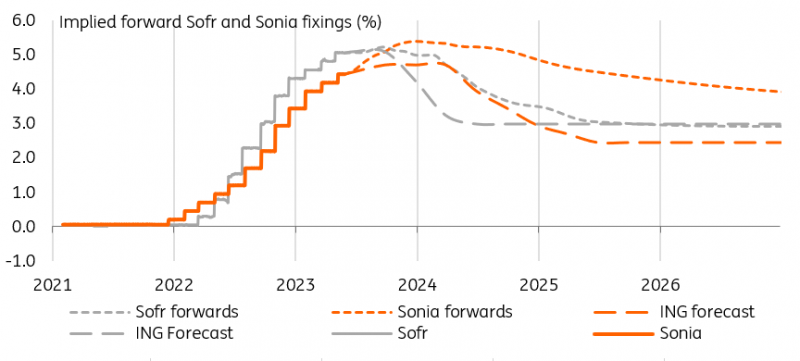

Both UK and US rates are above our forecast but it is the GBP curve that is most vulnerable

Source: Refinitiv, ING

ECB pricing is hard to move but markets look to the BoE for guidance

In Europe, today’s inflation prints from France, Germany, and Italy will, in addition to yesterday’s Spanish release, give us a pretty good idea of where the eurozone-wide number will fall tomorrow. If the drop in Spain’s core inflation is any guide, EUR markets will struggle to follow their US peers higher. Add to this that it is difficult for euro rates to price a path for policy rates that materially diverges from their US peers. Even if the Fed hikes in June or July, the EUR swap curve already prices ECB hikes at both meetings. Swaps assign a low probability to another hike in September for now. That probability may well rise but we think any labour-market induced sell-off in US Treasuries will reflect, in part, in wider rates differentials between the two currencies.

It is in the UK that the local swap curve is diverging most from the central bank’s message. Swap currently imply another 100bp of tightening will be implemented before year-end. We do not disagree that core inflation has been disappointingly slow to decline in the UK but betting on another four 25bp hikes this year requires a strong opinion on inflation dynamics which we think few in the market actually have. This means current pricing is unlikely to be maintained. Markets should also be on alert for a pushback by Bank of England (BoE) officials against market pricing. Only Catherine Mann is due to speak today. As the more hawkish member, she is the least likely to disagree with elevated rates but her pushback would be all the more potent.

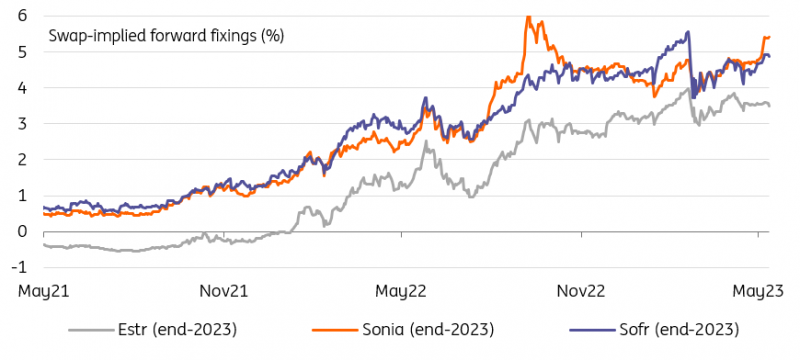

Forward EUR rates have been relatively immune to the recent re-pricing higher in USD and GBP rates

Source: Refinitiv, ING

Read the original analysis: Rates spark: Sterling rates most likely to fall, Dollar rates more likely to rise

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.