Rates Spark: It’s the ECB that’s behind the pace, not the Fed

The market now has more than a 50% probability attached to a 100bp hike from the Fed in July. We think this is overdone, and we think the bond market agrees with us. The outcome can be flipped in either direction by the Fed in the period ahead of the meeting on 27 July. It's the ECB that needs to pick up the pace before market rates and forwards flip too much.

Calls for a 100bp rate hike in July look overdone post-US CPI

The US CPI miss to the upside is 20bp on core and 30bp on headline (versus expectation). The reaction on the bond market has been more subdued than that, with the 10yr, having flirted with a move higher, is back below 3%.

The 10yr is up some 10bp from the lows seen yesterday before the “high inflation print talk”. The rise in nominal rates has come from a combination of higher inflation expectations and higher real rates, approximately 50:50, but not dramatic. The important 5yr expectations part of the curve has shown very little movement when measured versus the 2yr and 10yr on the 2/5/10yr fly. The 5yr is a tad cheaper, but only just.

More important, the 2/5yr inversion has deepened. This has helped the 5yr to maintain a richening preference, and suggests that longer dated yields don’t need to over react, even if the Fed feels they might need to. The probability for a 1% hike in July has risen, but a 75bp hike remains the central market bet.

We doubt very much the Fed will act to massage the market discount higher this time around, as inflation expectations in fact have fallen quite impressively in the past number of weeks

Importantly, the 2yr inflation expectation is below 3% versus 4.5% only a few weeks back. And the 10yr inflation breakeven is at 2.35%, well down from the 3% hit in May. These inflation expectations are quite deviant from the headline 9% – handle printed yesterday, but paint an important picture of calmness that such inflation prints (and we will see a few more) are likely overshoots when viewed in the forward looking longer term time.

The US Treasury curve isn't alarmed by higher inflation

Source: Refinitiv, ING

There is upside risk for yields from these data, but not enough to change our view that the peak is in at 3.5% for the 10yr yield. The money market, however, seems intent on pricing in an elevated probabilty for a 100bp hike. We think this is overdone. But if its gets close to 100%, the Fed will deliver just that. The big question is whether they will want or indeed whether they will need to deliver such an outsized outcome (25bp to 50bp to 75bp to 100bp, and then what? 125bp?). A 75bp hike is already big and can help inject some stabilty into the process.

We still think the Fed will prefer to go with a 75bp hike (the upper end of the predicted 50-75bp range mentioned at the June meeting), and premise that on the material easing seen in inflation expectations, alongside the slowdown clearly identified in yesterday's Beige book.

The EUR curve bear flattens, but is reluctant to price a larger July hike

EUR rates could not elude the flattening dynamic spilling over from the US in the wake of the CPI print. 2Y ESTR OIS posted a close to 10bp rise on the day while the back end even dropped slightly.

The EUR exchange rate flirting with parity to the dollar had prompted remarks from the European Central Bank’s Villeroy and later a statement from an ECB spokesperson that the central bank was “attentive the impact of the exchange rate on inflation”. The ECB’s hawks have been surprisingly quiet, though, foregoing this opportunity to push for a larger hike already July. The market’s pricing for the respective ECB meeting was thus relatively stable, rising by 2bp to price in roughly a one-in-four chance of a 50bp. The ECB has invested much in restoring its credibility and that also applies to its commitment of hiking by 25bp this month. But markets have shown less restraint to pricing in larger moves at later meetings post July and expect slightly more than 152bp worth of hikes to be delivered by the end of this year. Taking 25bp in July as a given that is 125bp across the remaining three meetings of the year.

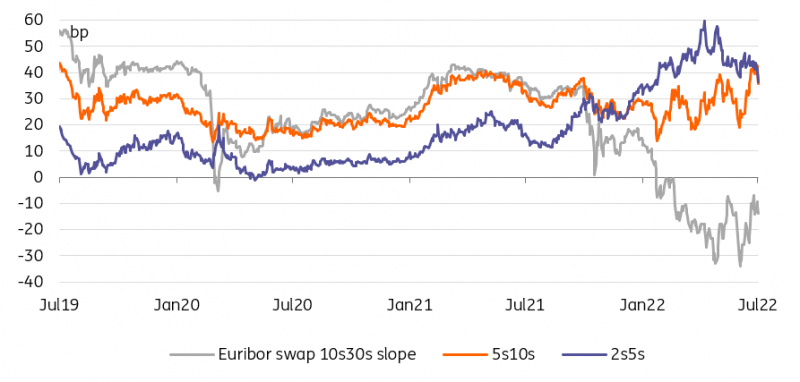

The EUR swap curve has found some flattening impetus after the US CPI release

Source: Refinitiv, ING

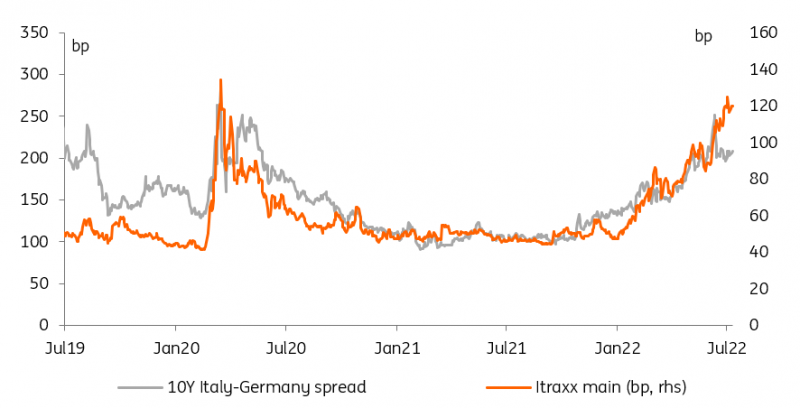

Faster tightening is not without cost, also in sovereign spreads. The initial risk-off move in markets also saw the 10Y Italy/Bund spread briefly topping the 200bp mark. A larger hike in July if not accompanied by a credible spread backstop still renders this spread vulnerable to further widening. For now the ECB’s promise to provide more detail on a new anti-fragmentation tool next week, paired with the flexible Pandemic Emergency Purchase Programme reinvestments having started this month has been enough to keep the spread in check, also relative to other market measures of risk and volatility. This has been even more impressive achievement given that the Italian collation government led by Draghi is looking increasingly fragile after the split of the 5 Star Movement with an important vote of confidence to take place in the Senate today.

Italian spreads are already too tight relative to credit indices

Source: Refinitiv, ING

Read the original analysis: Rates Spark: It’s the ECB that’s behind the pace, not the Fed

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.