Rates spark: Hawkish white noise

Today’s BoE hike is likely to be the last, but we’re not sure markets will listen to its message as the Bank keeps its options open. Markets appear to have been ignoring repeated hawkish ECB warnings to focus instead on US disinflation.

The recent Gilt underperformance will eventually reverse but the BoE won’t be the catalyst for it

Our expectation for today’s Bank of England (BoE) meeting, a 25bp hike, is shared by 47 out of the 48 survey respondents who participated in Bloomberg’s survey. It is harder to judge if we’re also in the majority in expecting no major change in policy guidance, effectively keeping the door open to more hikes if necessary. In the event, we think this will be the last in this cycle. The Bank sounds satisfied that enough tightening has been implemented and that its delayed effect will ensure (with an assist from base effects and a drop in energy prices in particular) inflation returning to its 2% target.

The focus will be on the BoE's forecasts and on its qualitative assessment

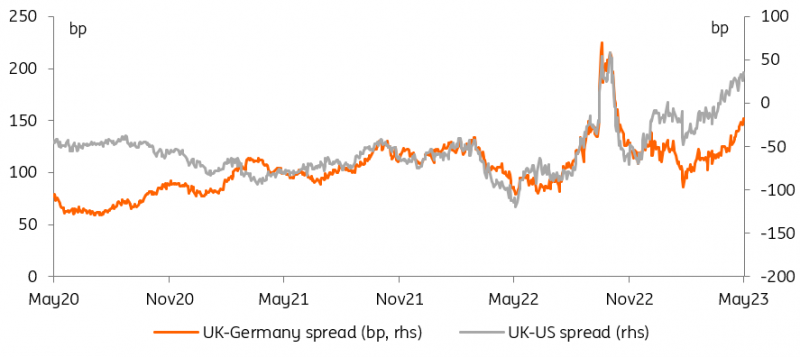

As usual when meetings come with an update of the monetary policy report and with a press conference, the focus will be on forecasts and on the Bank’s qualitative assessment. Here we think its predictions will be consistent with no more hikes, a slowing economy, and inflation returning to target within the forecast horizon, although a hawkish risk clearly stems from a more resilient economy. Markets have made their own mind up, pricing up to two more 25bp hikes in this cycle after today’s and driving a marked underperformance of Gilts against Bund and Treasuries. This will reverse in time, but the move occurred without the BoE’s encouragement, and it likely won’t be the BoE who helps it reverse.

Gilts underperformed Bund and Treasuries into today's BoE meeting

Source: Refinitiv, ING

Markets shrug off ECB hawks and focus on US disinflation

Away from the UK, the barrage of hawkish European Central Bank (ECB) comments continues with Bloomberg quoting internal sources as saying a September hike cannot be excluded. Unsurprisingly, this anonymous briefing failed to move market expectations, and rightly so. There are four months’ worth of data until then, and two updates of the ECB’s forecast, so what the hawkish wing of the Governing Council thinks in May of policy decisions in September is heavily discounted by the market. This is to say nothing of the already heavy hawkish briefing that took place since the May meeting, which markets are increasingly dismissing as white noise. In the same vein, the bar for Isabel Schnabel to push front-end EUR rates today is high.

A further slowdown in today’s annual PPI measures should reinforce that disinflation narrative

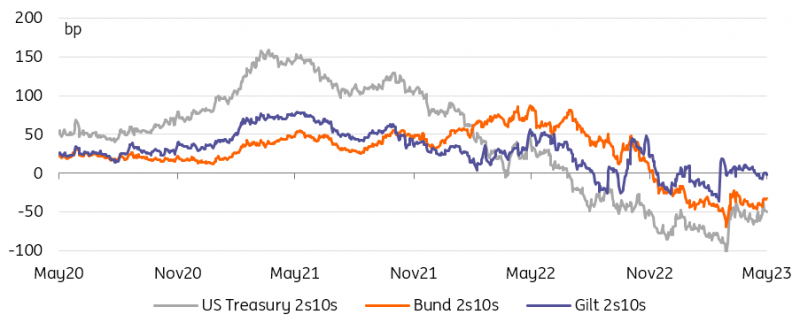

Instead the focus remains very much on US inflation data, and markets assume a strong read-across to European policy rates. Yesterday’s CPI report showed a slowdown in key core inflation components watched by the Fed. This caught many off guard after months of too slow progress on that front. Predictably, the curve’s knee-jerk reaction is to bull-steepen with almost three cuts priced by the December 2023 meeting, and a fourth one by end-January. A further slowdown in today’s annual PPI measures should reinforce that narrative.

Curve steepening impetus is modest so far, and mostly found in the US

Source: Refinitiv, ING

Read the original analysis: Rates spark: Hawkish white noise

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.