Rates spark: ECB, part of the solution or part of the problem

The more seriously the European Central Bank takes financial stability worries, the better the chance of a stabilisation in yields. Much depends on sentiment towards banks. We discuss a number of steps the ECB can take.

Today, the ECB balances inflation and financial stability risks

Based on economic data alone, the ECB should be hiking 50bp today. And indeed, this is what it signalled to markets at its last meeting. Today, however, the ECB is not making decisions just based on economic data. The rapid contagion from a US regional bank failure to European banks cannot completely be ignored. It is extremely difficult to say how far this contagion will go, and so how far it will end up tightening financial conditions in Europe, and so how much this could ‘substitute’ for ECB hikes.

And yet the ECB has to make a call. In theory, a response where it delivers the 50bp hike to fight still-rising core inflation, whilst providing a comfort blanket (see below) to market participants is the best course of action. In practice, the two are interconnected. There is a level of market stress where the ECB no longer needs to hike because of its impact on the economy. Neither can the ECB completely ignore the impact higher rates would have on confidence. The prudent course of action would be to pause and resume hikes later, but the ECB might judge that its already battered inflation-fighting credibility cannot afford it.

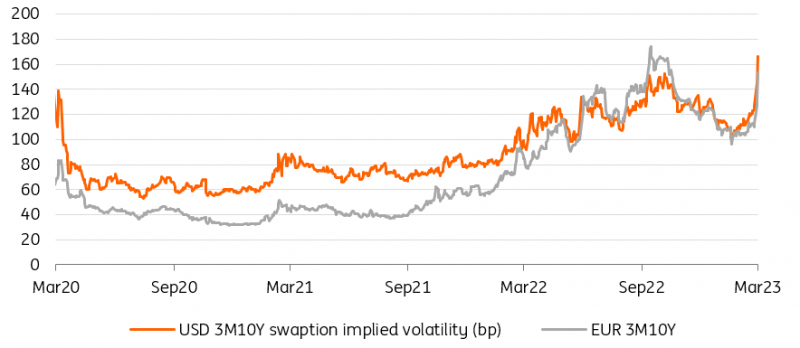

Swaption volatility exploded upwards, reflecting lower liquidity and the drastic change of market direction

Source: Refinitiv, ING

Comfort blanket needed, urgently

As with any crisis of confidence, the main task of authorities is to provide reassurance to market participants in order to stop self-fulfilling market panics. From the ECB, the first port of call would be to provide, or promise to provide, liquidity to banks under generous conditions if needed. Quantitative tightening, a process started just two weeks ago could also be seen as fanning the flames of the market crisis. None of these tools is perfect, and the ECB might be reluctant to interrupt a tightening process it has painstakingly started, but these are potential signals the ECB can send to markets. This is especially true if it still decides to hike.

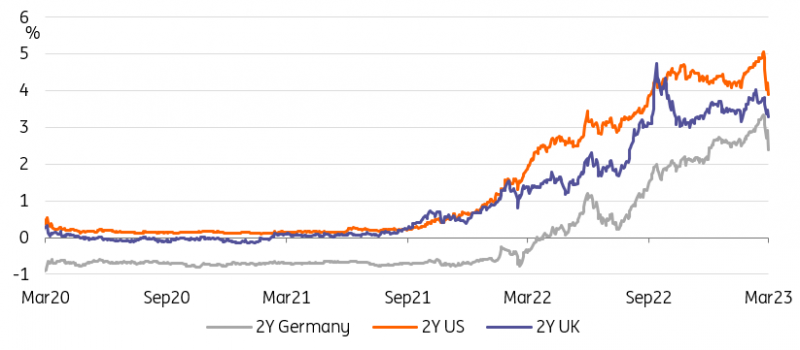

The psychological barrier to rate cuts is probably too high for today. After all, the ECB is facing an acceleration of core inflation and its forecast should show it taking longer to converge to target than anticipated. For the subsequent meetings, however, market conviction is growing that central banks will no longer be able, or need, to hike as much as previously thought. The nearly 50bp rally in 2Y US and German govies yesterday shows the magnitude of the reversal in market sentiment.

The fate of bonds today is pretty binary, and we wouldn’t overstate the importance of the ECB’s response compared to confidence towards banks. A hike (our base case), could well precipitate a fall in interest rates if market sentiment continues to deteriorate. Inversely, some measures could go some way towards reassuring the market, and so prevent a further fall in yields. The more seriously the ECB takes the situation in our view, the more likely we are to see a stabilisation in yields.

Flight to quality and rate cut expectations sent short-end bonds on a record-breaking rally

Source: Refinitiv, ING

Read the original analysis: Rates spark: ECB, part of the solution or part of the problem

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.