Rates spark: Bunds relatively detached from Oil price moves

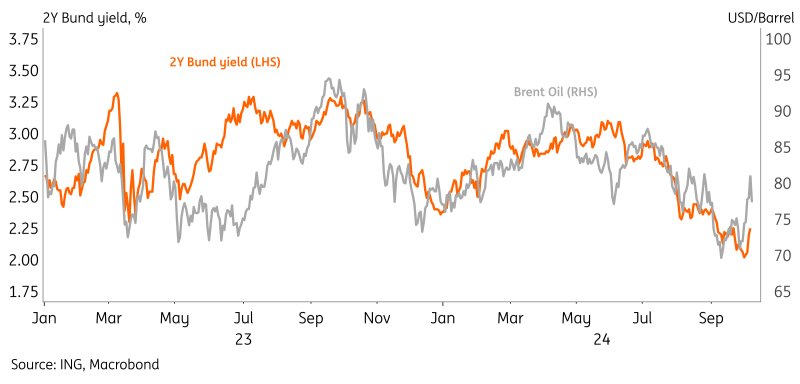

Bund yields have only reacted moderately to the recent uptick in oil prices, emphasising diverging growth outlooks. Markets are convinced of an October ECB cut and oil prices would need to move considerably higher to change conviction. Among the European supra names, the EU is the only issuer that still has a notable amount to fund this year.

Pessimistic eurozone outlook keeps Bund yields from ticking higher with Oil prices

EUR rates have settled higher after that big US payrolls number last week and are likely to trade more range-bound in anticipation of the upcoming European Central Bank decision. The conviction of a 25bp cut next week is high and there will be little economic data until then that could persuade markets otherwise. Having said that, we do have oil prices to watch, which have shown quite some volatility of late. If we see more upside surprises from global growth, and at the same time headlines from the Middle East emerge, the risk of higher prices could be considerable.

Still, Bund yields reacted only moderately to the recent uptick in oil prices (see figure below), which emphasises markets’ diverging expectations between global and eurozone growth. The US labour market is showing signs of resilience (again), whilst Chinese growth expectations are improving on the back of broad stimulus measures, helping oil prices to go higher. The potential bright spots for the eurozone are more difficult to see and given growth concerns are getting more attention of late than inflation, the front end of the Bund curve is likely to remain anchored for now.

Whilst the ECB did mention the decline in oil prices as a supporting factor in its decision-making earlier, we would need to see a lot more to convince markets that an October cut may not be as obvious as priced in. Also on Tuesday various ECB speakers, including the known hawk Nagel, hinted at a willingness to cut in October. Nevertheless, the current pricing of 24bp for a cut may be stretched and a sudden push higher by oil could challenge that positioning.

EU to remain prominent in primary markets even after Tuesday's larger deal

The EU issued €11bn via the syndicated reopening of two bond lines, €5bn in a 3y and €6bn in a 15y. Investor appetite looked healthy with a combined book of €166bn and in the end the size of the transaction exceeded market expectations, and was also larger than the September deal.

Among the European supra names EU, ESM, EFSF and EIB, the EU is the only issuer that still has a notable amount to fund this year. With close to €118bn issued, slightly more than €22bn remains to reach the indicated target of €140bn for 2024. ESM and EFSF have completed their funding for the year, and EIB said its 5Y EUR bond issued last week was the last EUR benchmark for the year with close to €62bn of its €65bn funding target reached.

In terms of spreads, the valuations of the sector versus swaps in the 10y area are still around 5-6bp cheaper versus the end of August, but there has been some stabilisation since the beginning of this month.

Recent uptick in Oil prices did not find its way to Bund yields

Read the original analysis: Rates spark: Bunds relatively detached from Oil price moves

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.