Rates daily: How to spend it

It’s all good right? Well $Libor doesn’t think so, at least not yet. There was some intra-day easing yesterday, but we’ve yet to see a definitive fall in fixings. The ECB and the Fed keep plugging away, still all in. Without the ECB, there might by no non-resident buyers of Italy. We examine the latest numbers.

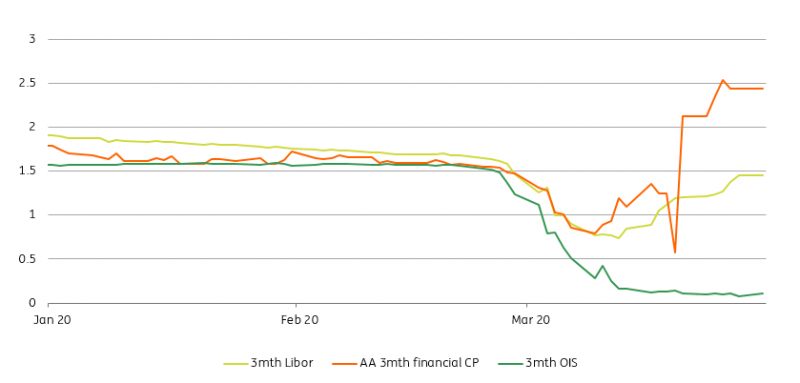

Oh Libor, still off-colour

Although the FRA/OIS spread did ease back below 135bp yesterday, that was more a reflection of a moderate rise in the risk free rate (reacting to a better tone for risk assets).

Either way, $Libor remains elevated, and that reflects stress. And in fact 3mth Libor at 1.45% currently likely underestimates where it could be given AA financial CP with a 2% handle. It is one of the few measures that has not seen a material turn for the better in the past week when practically everything risky turned up.

One of the issues here is default risk. If this turns bad, defaults could be as high as 20% according to Moody’s. But even on a more benign base case, defaults are set to reflect a deep recession. This would mean in the 5% to 10% area, and likely at the upper end (versus 1.5% currently). When defaults rise, that tends to hurt banks, and is part of the transmission process behind Libor elevation.

Diverging dollar rates (%)

A next step now is to get the Fed’s domestic commercial paper support programme off the ground, as that will act to reduce demand from bank credit revolvers. That is the cleanest means to taking perceived pressure off the banks and, by extension, $Libor.

We believe there is actually no pressure here. It’s just that simple extrapolation generates one in theory. Here too we need to flatten the curve.

Keeping track of central banks flow

With much of our enthusiasm for core government bonds hinging on central bank purchases, it is worth keeping a close eye on weekly purchase flow and targets. So far, the Fed and ECB have given signs of 'spending the envelope'. In the Eurozone, PSPP net buying settled last week totalled almost €20bn and Reuters reported €15bn was purchased under PEPP (the breakdown between sovereign and corporate bonds is not known), on Thursday and Friday we surmise. This would be indicative of a significant 'front-loading', leaving us hopeful that the announced purchases 'envelopes' will be spent in full and therefore bring downside to bond yields by crowding out potential buyers. In the US, the Fed's purchases this week will be carried out at a rate of $60bn per day, down from $75bn per day in the past two weeks. But still a very significant number.

Italian yields capped by the ECB...

So far this week, it is noticeable how optimism in equity markets did not permeate through to Italian government bonds. Here the effect of central bank purchases crowding out private investors is perhaps too hopeful. In our mind the impact of PSPP and PEPP on peripheral bonds works in two phases. First, the flexibility around the timing and breakdown of the purchases allows the central bank to cap borrowing costs by absorbing most, if not all of selling flow, presumably from foreign investors. The second phase is when foreign investors decide to return to peripheral bond markets.

...but non-residents await show of European unity

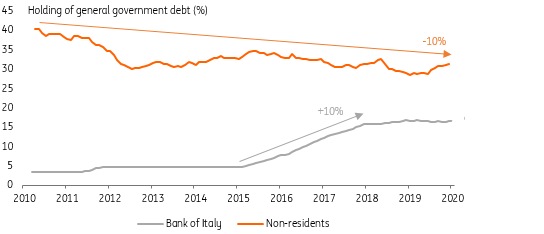

This second phase could prove elusive as long as the debate around fiscal risk-sharing continues out in the open. Kicking the issue into the long grass lowers headline risks in the near term but a display of European unity is needed for cross border flows to reverse in our view. In the meantime, the ECB should function as a backstop as long as selling pressure remains within the limits of what it can buy. For comparison, between the onset of the Eurozone crisis and now, the share of non-resident holding of Italian debt has dropped by10% of the total, whilst that of the central bank has risen by the same figure. This may be an extreme case but it gives an idea of what central banks are replacing.

The central bank has replaced non-resident debt holders

Source: Banca d'Italia, ING

What's up today: More CPIs, ECB talk, Italian and Belgian bond sales

More Eurozone member states' CPIs are released today: from France, Italy, and the Eurozone. Fair to say the attention will more likely be on 'current' indicators. The Austrian central bank's Holzman will be on the wires and a more supportive tone towards recent ECB decisions would help ease fear of divisions within the governing council.

Italy will reopen three bonds in 5Y to 10Y maturities as well as a floater or a total of up to €8.5bn. Belgium will be in the market with a syndicated sale of a new 7Y bond. The announcement came immediately after the Belgian debt agency updated its auction calendar by adding auctions in May, August and October. Money market issuance is also increased.

Read the original analysis: Rates Daily: How to spend it

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.