Powell put at play: Rotation, Yen and treasuries

Key points

-

US June inflation report and recent Fed comments have renewed market hopes for Fed rate cuts to begin in September.

-

Investors are rotating from large-cap to small-cap stocks, the Japanese yen has strengthened significantly, and there is strong demand for 2-year Treasuries, all in anticipation of potential Fed rate cuts and shifts in global monetary policies.

-

Despite renewed optimism, structural inflation and US election risks suggest that the Fed is likely to proceed cautiously with rate cuts.

Since the Federal Reserve indicated the end of its aggressive rate-hiking cycle, the focus has shifted to the timing and pace of potential rate cuts. At the start of the year, markets anticipated that disinflation would accelerate and that the Fed would reduce rates six to seven times. However, inflation data from the first quarter showed a resurgence in price pressures, altering market expectations to a single rate cut for the year.

Recent data has, however, revived expectations of the Fed beginning to ease rates soon. The June CPI report on July 11, which showed a whiff of deflation, has rekindled optimism about potential rate cuts starting as early as September. In addition, comments from Powell and other Fed officials have suggested increasing optimism regarding the inflation outlook and hinted that rate cuts might be imminent. This sentiment is further supported by recent labor market trends, such as reduced job openings and slower wage growth.

Given these significant shifts in inflation and labor market conditions, there is a strong argument for the Fed to proactively adjust its policy to ensure a soft-landing remains achievable.

Some parts of the market, as noted below, are already shifting in anticipation of the potential Fed rate cuts. Money is flowing into the beaten-down, capital intensive and rate sensitive parts of the market that can potentially get a boost from a lower interest rate environment.

Rotation from large caps to small caps

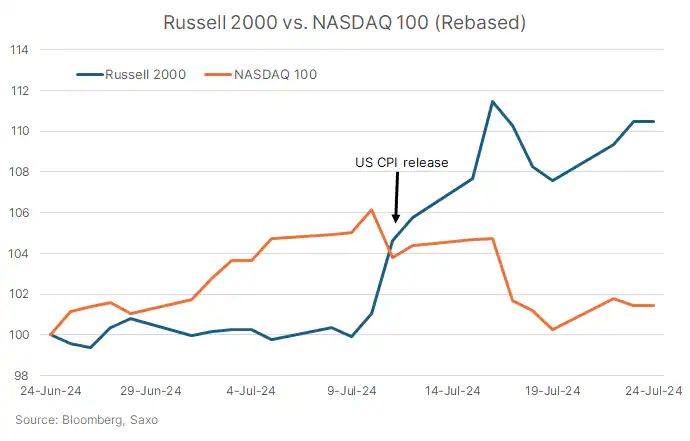

Small caps have underperformed the large cap indices such as S&P 500 and NASDAQ 100 since the start of the year. However, small caps have taken a lead over the large cap stocks since July 11, as shown in the chart below. The Russell 2000 index of smaller US stocks is up 10% since the day of inflation release while the S&P 500 is down 1.4% and NASDAQ 100 is down over 4%.

As we have discussed previously, investors are potentially rotating from large-cap to small-cap stocks in anticipation of a more favorable monetary policy environment. Smaller companies typically are sensitive to high borrowing costs because they carry heavier debt loads with floating interest rates compared to large caps. We discussed more about the recent Russell 2000 outperformance in this LinkedIn post.

Japanese Yen bears are retreating

The Japanese yen has seen sharp gains across the board since the July 11 US inflation report. The yen is up over 4% against the US dollar, with Fed easing bets coinciding with expectations that the Bank of Japan may hike rates further at the July meeting. This potential shift in yield differentials favors the yen.

Meanwhile, Japanese authorities also seemingly intervened in the FX markets after the US inflation report to help strengthen the yen. The move is also potentially squeezing the yen short positions, given yen-funded carry trading has been a popular strategy over the last few years.

Solid demand at 2-year treasury auction

The latest 2-year Treasury auction witnessed solid demand, indicating strong investor interest in shorter-term government debt. This surge in demand is likely driven by expectations of lower future interest rates, as investors rush in to lock in the current yields.

Investors secured a combined 91% of the auction, the highest since 2003, while primary dealers received a record low of 9%. The 2s10s curve inversion eased to about -24 basis points, nearing the least-inverted levels of the year. The high demand for Treasuries underscores the market’s anticipation of the Fed's supportive monetary policies continuing.

A word of caution

We have been here before.

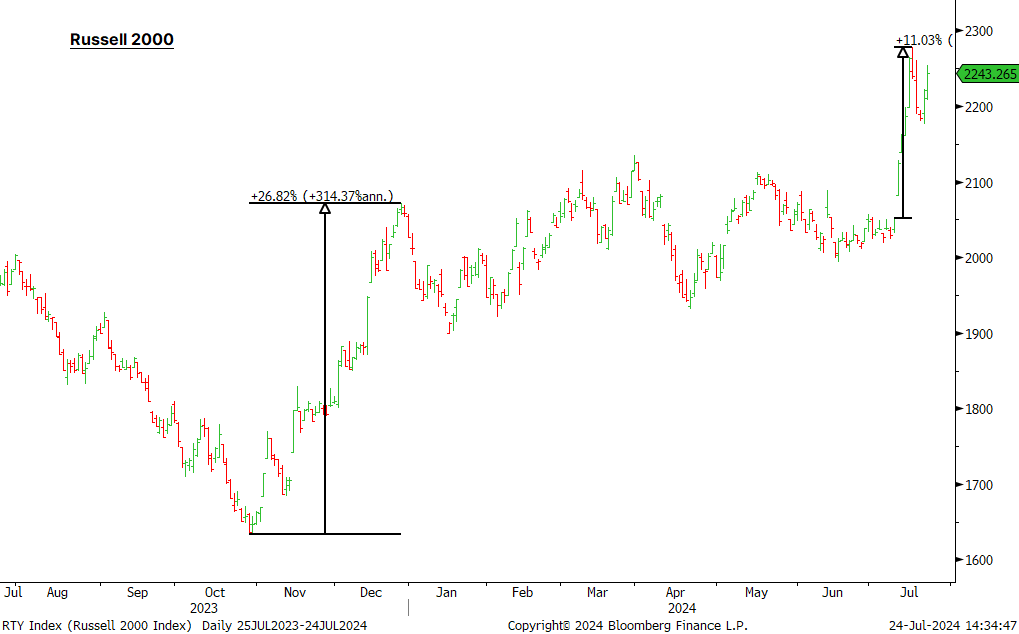

In late 2023 as well, small-cap index Russell 2000 rose 27% from its October lows, outpacing the 17% gains in S&P 500 and 20% in NASDAQ 100 as markets anticipated Fed rate cuts. However, as Fed rate cut expectations eased, Russell got locked in a range while the large-caps continued to gain on the back of a solid earnings momentum.

Source: Bloomberg. Disclaimer: Past performance does not indicate future performance.

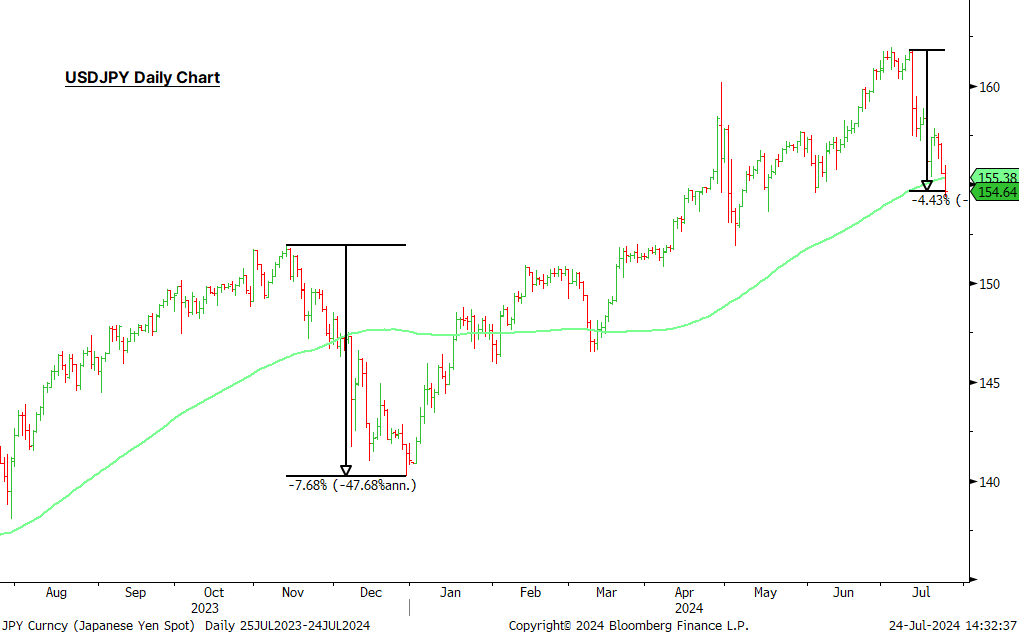

Likewise, the Japanese yen gained about 8% against the US dollar in late 2023 on the back of Fed easing expectations, before reversing back to record lows.

Source: Bloomberg. Disclaimer: Past performance does not indicate future performance.

This is clear evidence that early optimism on rate cuts is at play here. However, sustained trends are only likely if fundamentals support and the rate cut cycle continues.

However, structural inflation pressures suggest that inflation may not return to the Fed’s 2% target. Factors such as labor supply shortages, supply chain disruptions, the green transition, and sustained fiscal spending will continue to drive inflation. Additionally, US election risks imply that while the Fed may start its easing cycle, but it will likely proceed cautiously with rate cuts to allow time to assess the new administration’s policies and their impact on inflation.

As such, rate cuts from the Fed are unlikely to be enough to resolve profitability issues for the small-cap companies or make the yield differentials unattractive for yen-funded carry trading.

Read the original analysis: Powell put at play: Rotation, Yen and treasuries

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.