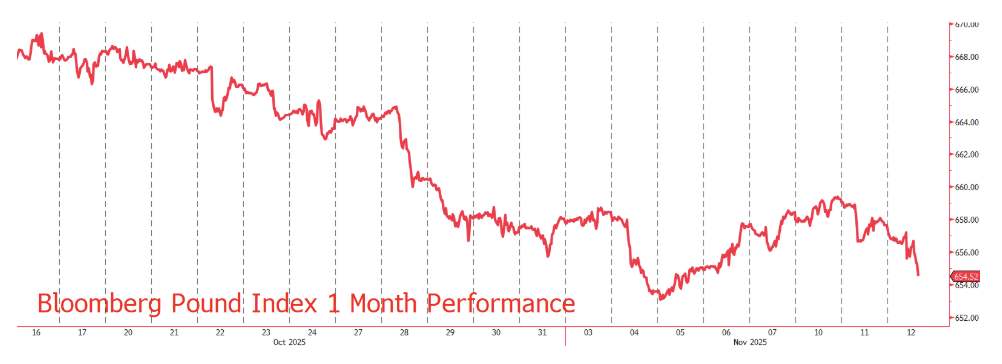

Pound bound to soften regardless of budget

It’s another bad day at the end of a bad month for the Pound, possibly at the start of a bad quarter. News that unemployment had reached 5%, months ahead of the Bank of England’s estimate of it only reaching that rate in early 2026, hurt GBP, but not quite as much as the news this morning.

Firstly, GDP data showed the economy coughing out a 0.3% growth rate in Q3 of this year, slightly better than Q2, but not setting the world alight by any means. Secondly, the specter of political risk took form early morning as the current Health Secretary, Wes Streeting, was forced to explicitly back PM Kier Starmer after rumours of a plot to place himself in the big seat took hold. No smoke without fire when it comes to these things and it’s a space we’ll have to watch carefully.

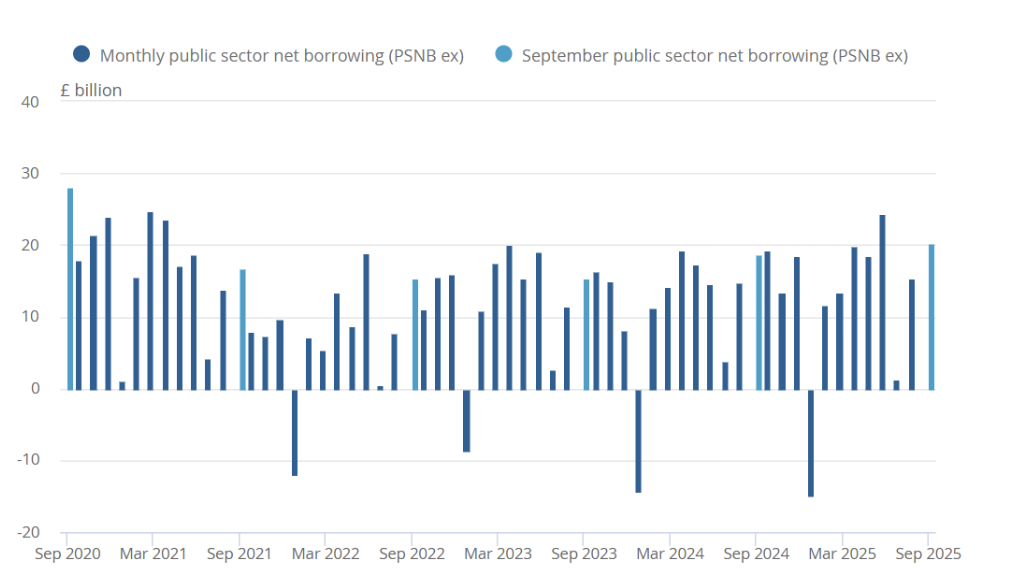

But the most interesting area relative to FX was the suggestion that Chancellor Rachel Reeves wanted to bolster the UK’s “fiscal buffer” to lower borrowing costs. Practically, this means that Reeves would tax more than necessary in the next budget, so as to increase her “fiscal headroom”- that being the difference between what the Government actually spends and its self-imposed limit of spending.

Reeves gave herself £10bln worth of headroom at the last budget, but this has all but been chewed up by higher-than-expected borrowing costs this year.

By increasing this space buffer, the Chancellor should increase the UK’s resilience to fiscal shocks, on paper at least. If Reeves doubles the buffer, she lowers the chance of needing to raise taxes for the third consecutive budget next year. Naturally, doubling the buffer would take £10bln, an add-on to a budget already likely to take £35-50bln out of the economy in taxation.

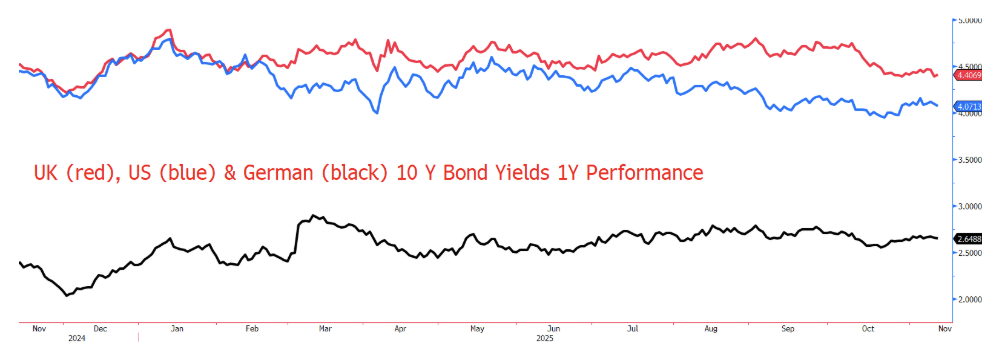

Even worse for GBP bulls, by increasing this buffer and protecting public finances, the risk premium associated with UK Gilts is likely to decline. Bloomberg Economics estimates this move could precipitate as much as a 30bps decline in 10-year UK yields, representing a considerable drop in the attraction of Gilts to yield hunters.

We can then suggest, that GBP could suffer the double blow of higher taxes, lowering future inflation estimates and an increased fiscal buffer taking the risk out of yields, that would further hammer the value of the Pound.

Indeed, the last time we saw UK 10 Y yields 30bps lower than their current 4.4% was back in October of 2024, when GBPUSD was just below $1.29, a bad sign for Sterling.

Most estimate that the plan could bear fruit, potentially saving £6bln worth of debt payments by 2029-30. But it will come at a cost in the short run, that being a higher taxation burden into next year, which is bound to drain the already anemic Pound of more life.

But with the UK government spending £124bln just on interest payments in FY 2024-25, out of £1.28 trillion in overall public spending, it may be one of the painful fixes we need.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.