Positive sentiment gaining ground but can it last through Non-Farm Payrolls? [Video]

![Positive sentiment gaining ground but can it last through Non-Farm Payrolls? [Video]](https://editorial.fxstreet.com/images/TechnicalAnalysis/Sentiment/risk-under-magnifying-glass-60181126_XtraLarge.jpg)

Market Overview

The past few sessions has begun to see a more constructive environment for risk emerging once more. The question is that after weeks of see-sawing sentiment, can this move be sustained? There is still a drip feed of positive economic data for June which has helped to counter the concerns of rising COVID-19 infection rates for the US and rolling back of economy re-openings. However, it will be interesting to see whether there is a tipping point back lower once more, and it will be in the July data that this may start to become an issue once more. This edge towards risk improvement has been backed by the FOMC minutes last night, which talked favourably of yield curve control. An outcome based forward guidance (monitoring the level of inflation) was also on balance favoured. This lends a ongoing dovish bias to monetary policy from the Fed. Treasury yields and the dollar are being weighed down in the wake of this, whilst equities are ticking positively. Looking forward today, attention quickly turns to the Nonfarm Payrolls report, this month brought forward to Thursday, due to the Independence Day public holiday tomorrow. Payrolls are expected to show a record gain of +3 million jobs in June, which would beat the existing record of +2.5 million jobs added in May. This remains a fraction of the 20.6 million jobs lost in April and it will be interesting to see what sort of reaction the market gives, considering the developments in more than 12 states of slowing or even reversing re-openings of their lockdowns.

Wall Street closed positively for a third straight session, with the S&P 500 higher by +0.5% at 3115. Futures are showing a continuation of this positive move today with E-mini S&Ps +0.4%. Asian markets have been broadly positive, with the Nikkei +0.1% and Shanghai Composite +2.2%. European markets look set fair too, with FTSE futures +1.0% and DAX futures +1.3%. In forex, the risk positive bias is also present with the underperformance of JPY, whilst EUR, GBP and NZD all gain ground. Commodities show the move higher on oil continues to creep through, whilst the precious metals have had their breakouts dragged back with gold and silver a shade lower.

With it being a public holiday in lieu of Independence Day in the US tomorrow, the payrolls report is on a Thursday this month. The US Employment Situation is at 1330BST. Headline Nonfarm Payrolls are expected to show another +3.000m jobs added back into the US economy in June. This comes after the gargantuan surprise of +2.509m jobs were added in May. The potential for a sizeable revision will be high and w3%ll be a key factor in how the market assesses the overall composition of the report. Unemployment is expected to be reduced to 12.3% (from 13.3% in May). Average Hourly Earnings remain a curious statistical issue, with a decline of -0.7% expected on the month, to 5.3% year on year (down from 6.7% in May). WE are also keeping an eye out for the Weekly Jobless Claims at 1330BST which are expected to show another 1.355m claims in the past week (1.480m prior). US Factory Orders for May are expected to show a rebound of +8.9% on the month (although still not recovering the -13.0% of April).

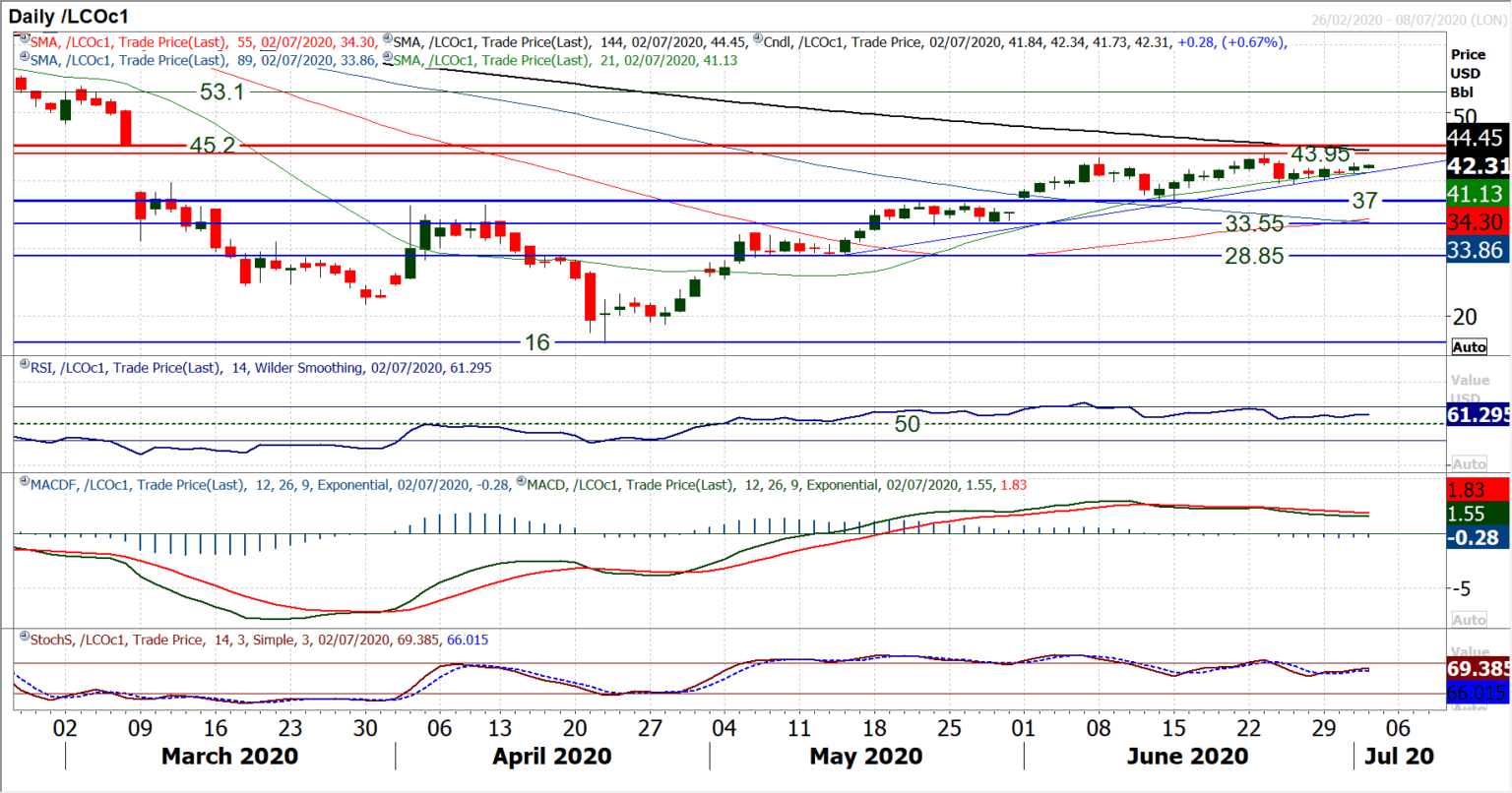

Chart of the Day – AUD/JPY

Is risk appetite beginning to improve again? Aussie/Yen is often seen as a key gauge of risk and is just beginning to pick up after a period of correction from early June. Having stabilised a move back from 76.75 around 72.50/72.75, the major cross has been taking its time in finding buyers once more. After a couple of weeks of consolidation, something looks to be brewing for the bulls. With the underpinning of support from a three month uptrend, the magnitude of positive candles in the past week or so are beginning to pull the market higher once more. Candles this week have been encouraging and show an appetite to buy into intraday weakness now, on a succession of higher daily lows. Pressure is mounting on the 74.50 pivot area. A close above this resistance would really suggest positive traction is building. The improvement is already coming through, as the Stochastics rise in the wake of a bull cross, and RSI is also looking to move into the 60s. Given the consolidation in recent weeks, it would be wise to see confirmation of an upside break before looking to buy. However, there is now decent support building around 73.20/73.30, around where the three month uptrend comes in today. A move above 75.05 would re-engage upside traction for a retest of 76.75.

Brent Crude Oil

Although the market looks to be struggling for traction, there is still a mild positive bias that comes with the market tracking higher over the past few sessions. Brent Crude is a market that may have lost some of its drive, but it is still gaining ground nonetheless. This does however leave us slightly more cautious than we have been previously been over the continuation of the trend higher. This is a recovery which has seen uptrends shallowed out on several occasions in recent weeks. Faltering positive momentum configuration also requires attention. Negative divergences on RSI and Stochastics, whilst MACD lines bear crossing all lend caution as to how far the bulls can take this move without a correction. What is likely is that the market is in the process now of building a medium term range. Support at $36.40/$37.00 remains strong but the resistance of the highs at $43.40/$43.95 and the importance of the gap at $45.20 suggests this is a growing problem for the bulls to continue higher. Initial support of the past couple of sessions at $40.90/$41.05 is needed to hold to maintain the mild positive bias. The importance of support at $39.50/$40.00 is growing.

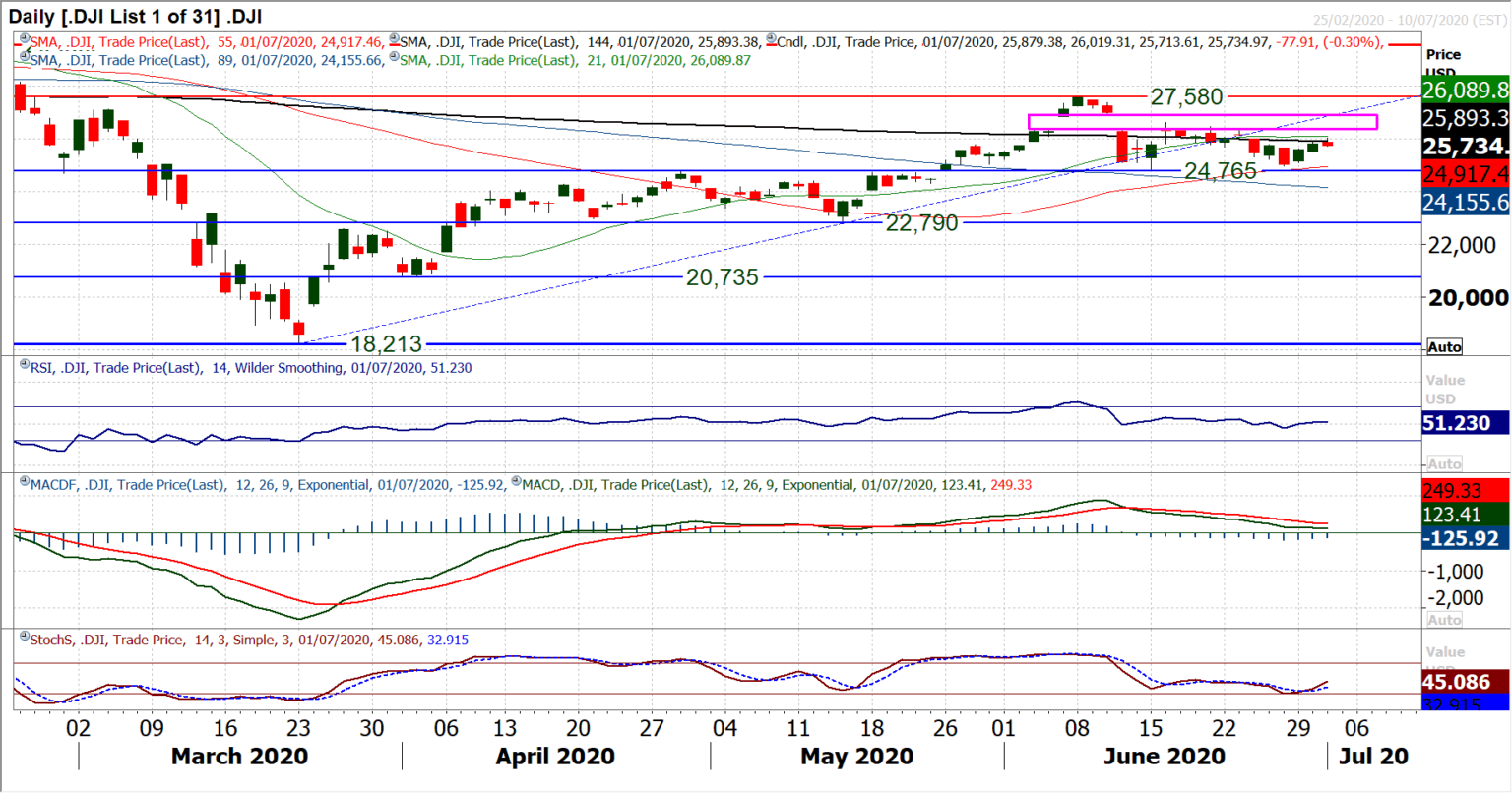

Dow Jones Industrial Average

The selling pressure may have eased in recent sessions, but this looks increasingly to be a ranging market now for the Dow. Support has been bolstered between 24,765/24,970 and forms the bottom of the range. However, the island reversal back in early June has left a key gap open but is a growing band of resistance too. Failures between 26,315/26,610 have built up a barrier to gains, and with the market again faltering last night, recovery impetus is leaking away. Momentum indicators have picked up in recent sessions, but this essentially the daily RSI is reflecting a tight range between 45/55 for three weeks now. Below 24,765 support or above 26,610 resistance would give more of an indication of direction going forward. Until then, this is a consolidation.

Author

Richard Perry

Independent Analyst