Positive PMIs don't mean inflation is coming

Outlook:

Before getting into the issues surrounding the data, note that trading in all sectors can easily be disrupted today because of a massive snowstorm hitting the East Coast. We have al-ready suffered temperatures below freezing, sometimes well below, for over a week, with an-other week to come and this time with a blizzard's worth of snow accumulation and high winds. Schools and airports are closed. Not everyone will be able to make it to the office. Washington has already post-poned release of the usual Thursday jobless claims. Trading may be thin and that can make for volatility.

We get the ADP private sector jobs forecast today, probably 190,000 (the same as November) and the Markit services PMI. The flash had disappointed on the downside so expectations of a better final may be a dollar positive.

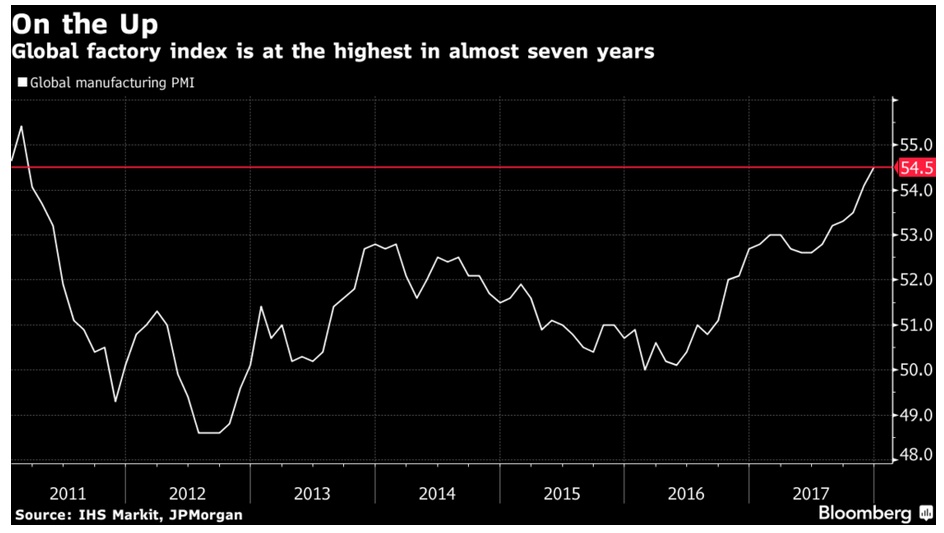

The big story so far this week is the slew of very good manufacturing and service PMIs being released by everybody—China, Canada, Europe, the US and even the UK. JP Morgan reports its collection of world indices is the highest since 2011 and this is the buttress for a global growth forecast of 4%.

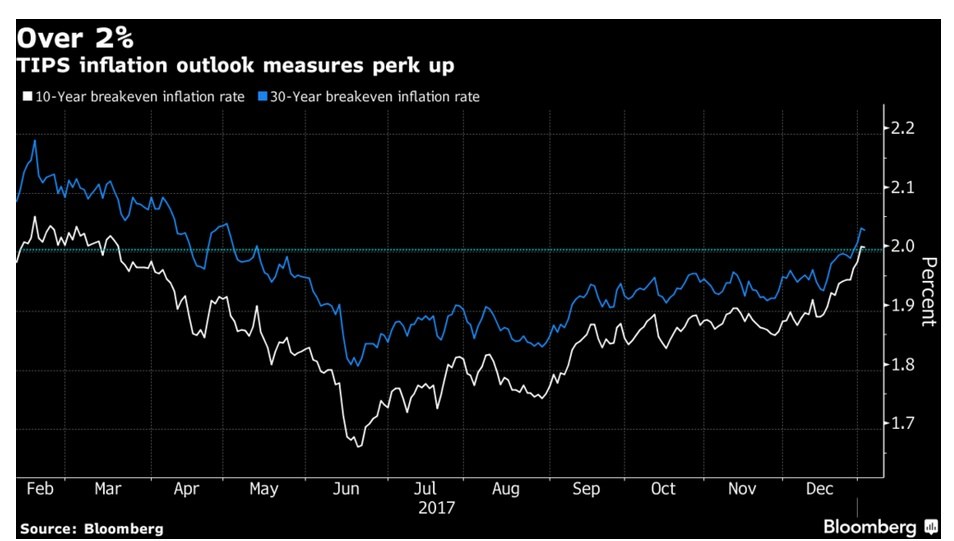

Bloomberg takes the opportunity to sell newspapers by linking high PMIs to supply constraints that will lead to price inflation. "Government bonds fell around the world as traders moved to price in the prospect of quickening inflation. The yield on 10-year Treasury notes increased four basis points to 2.45 percent while the 10-year break-even rate, a gauge of the outlook for consumer prices over the coming decade, approached 2 percentage points for the first time since March. In Europe, the five-year, five-year inflation swap rate increased to the highest level since February."

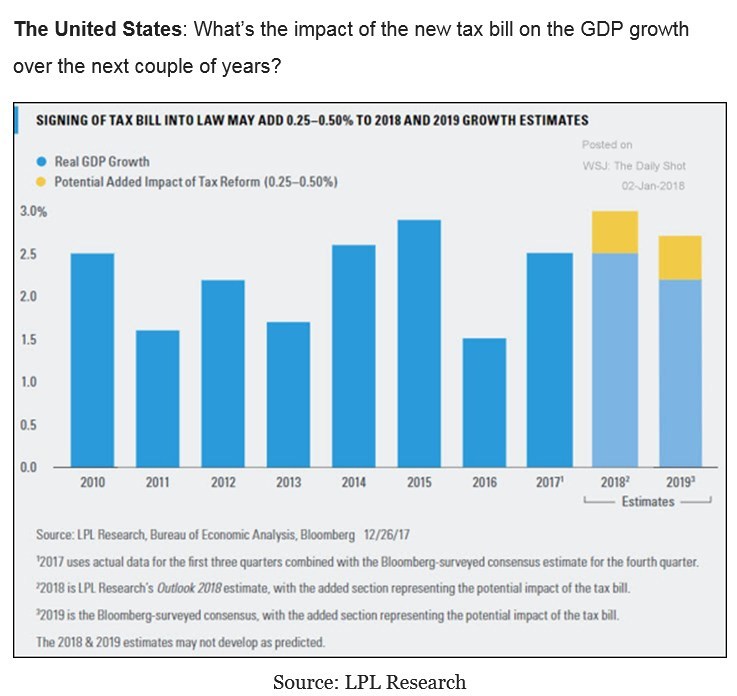

The Daily Shot is an email report from the WSJ that contains nuggets of research from outfits you probably don't subscribe to. We like the charts. Below is a picture of US GDP showing the effect of the tax cuts. The amount is small, only 0.25-0.50%, but appears more important in graph form. Depending on how many decision-makers see charts like this, confidence could be about to zoom upward.

Markit chief economist Williamson notes that the market does not expect sustained inflation. "But the near-record incidences of supply-chain delays seen toward the end of 2017 indicate that pricing power is shifting from the buyer to the seller, suggesting upward price pressures are gradually returning." Bloomberg chief economist Mike McDonough writes "Rising supply constraints across many of the world's largest economies represent a return to normalcy for now, but if momentum continues it will ultimately become inflationary. Accelerating growth has been eating up excess capacity and once that is gone inflation will perform in a more typical fashion and accelerate."

Granted, robust PMIs do suggest supply constraints may be coming. But while PMIs are the key eco-nomic indicator these days, they are not the only indicator. Two others of equal importance for project-ing inflation are capacity utilization and wage growth. When an economy has plenty of excess capacity, inflation is far behind. Tradingeconomics.com gives us the chart below.

The tradingeconomics.com site summarizes that "Capacity utilization in the US increased to 77.10 per-cent in November from 77 percent in October of 2017. Capacity utilization in the US averaged 80.31 percent from 1967 until 2017, reaching an all-time high of 89.40 percent in January 1967 and a record low of 66.70 percent in June of 2009." In other words, the US is still pretty far from the long-term aver-age. It's a stretch to say the US is reaching "supply constraints." And with a few exceptions, that im-plies wage growth is not about to explode upwards any time soon. The capital investment that could come from tax reform is not going to materialize. Nearly every analyst on the planet opines that the extra money will go to dividends, stock buy-backs and executive bonuses, not capital investment or higher wages.

Here's the scenario likely to take hold: the US is getting better growth than we thought but not as good as the eurozone and surprise! Even Japan is perking up. Inflation is assumed from capacity stress but in the US, capacity utilization is still on the low side, while in Europe, reports of supply constraints and labor shortages are credible. On the demand side, US households are already overspending their brains out, while that optimistic mode is just beginning in both Europe and Japan. If anyone is going to get inflation, it's the eurozone.

In FX, everything is relative. Maybe the US will be getting terrific growth and even a little inflation, but it's old news that the Fed is normalizing. It will be fresh news if the ECB accelerates its process and thus leads to the idea that zombie bonds yielding less than zero are a thing of the past. Investors have already demonstrated an appetite for non-dollar assets. In what area does the US offer investment op-portunities more attractive than elsewhere and enough to overcome the long-standing bias against the dollar? California pot-growing, maybe. Granted, the new tax regime will appeal to some, but a Trumpi-an trade war, a likely event this year, might be a counter-weight.

Longer-term, this suggests the dollar will resume its downtrend and the Trump Dollar will put in anoth-er lousy year. But short-term, meaning a few days to a week, the euro peaked at a high ten points under the last highest high (1.2092 on Sept 8) and unless it surpasses the Jan 2 high at 1.2082, will correct downward, probably at least to red support around 1.1960-70. It's hard to forecast the euro/dollar fall-ing after concocting a forecast scenario that has it rising, but at the same time, traders tend to behave in predictable ways. The failure to match and surpass the old highs—two of them—implies a pullback. Stay tuned. We can always get a Shock.

Finally, confidence in the US and its political leadership is falling to new all-time lows. At least some of the stories are funny.

Tidbit: We all had a bit of fun yesterday when former White House advisor Bannon was quoted in a new book about Trump (Fire and Fury, Inside the Trump White House by Michael Wolff) saying Trump Junior committed treason for failing to notify the FBI about Russian promises of opposition dirt and will go down for it. Bannon also thinks what special prosecutor Mueller is really after is money laundering. Those are the law-related things. Politically, Trump and the campaign people never ex-pected to win (Melania cried) and running for the office was intended solely to boost the brand. Flynn said the Russian speaking event money was a problem "only if we win."

On the gossip side, Wolff writes the White House is a seething chaos of staff back-biting and incompe-tence. Trump doesn't read, even a one-pager, and didn't make it to the 4th Amendment in the briefing on the Constitution, He has the attention span of a gnat and interrupts briefings with irrelevant and off-the-wall remarks. The White House is a stepping stone for the younger Trumps to run for office, de-spite Ivanka being as "dumb as a brick." Trump likes fast food because he can be sure it's not poisoned. Trump obsesses about losing his hair and wears the ridiculous style to cover up a bald spot that scalp reduction didn't entirely fix.

Even the FT and Guardian have the story on the front page. Trump repudiated Bannon in a series of tweets, saying Bannon lost his mind when Trump fired him. Trump is also trying for a court order to halt Bannon speaking disparagingly about him, as contracted during the campaign. Picking such a big fight is the usual ploy of distracting attention from ... what?

Here's the problem: maybe neither one of these two repulsive guys has lost his mind and it's all a giant game of some sort that narcissists play. Bannon might be trying a page from the distraction book by throwing money laundering out there. And Bannon, through Breitbart, has the loyalty of the diehard Trump supporters. Is it even remotely possible Trump can keep them if Bannon really has turned on him?

Trump was coherent enough in the latest tweets. But in an Esquire article titled "Trump's New York Times Interview Is a Portrait of a Man in Cognitive Decline," Charles Pierce notes Trump is "only in-termittently coherent. He talks in semi-sentences and is always groping for something that sounds fa-miliar, even if it makes no sense whatsoever and even if it blatantly contradicts something he said two minutes earlier.... this is more than the president's well-known allergy to the truth. This is a classic coping mechanism employed when language skills are coming apart....

"In addition, the president exhibits the kind of stubbornness you see in patients when you try to relieve them of their car keys—or, as one social worker in rural North Carolina told me, their shotguns. For example, a discussion on healthcare goes completely off the rails when the president suddenly recalls that there is a widely held opinion that he knows very little about the issues confronting the nation. So we get this: "But Michael, I know the details of taxes better than anybody. Better than the greatest C.P.A. I know the details of health care better than most, better than most. And if I didn't, I couldn't have talked all these people into doing ultimately only to be rejected."

"This is more than simple grandiosity. This is someone fighting something happening to him that he is losing the capacity to understand." In a nutshell, Alzheimers or some other form of cognitive impair-ment. Vanity Fair, Forbes and The Atlantic magazines have run articles on the subject. Last summer the American Psychiatric Association repeated the Goldwater Rule, which says psychiatrists should never give opinions on people they have not actually examined, but the American Psychoanalytic Asso-ciation is willing to do it, and comes up with a diagnosis of impairment.

A Yale conference on the subject in November sputtered when the university departments backed out in the usual academic cowardice, but stressed the concept of "duty to warn." As we wrote last year, however, it would be almost impossible to get rid of Trump unless the VP and cabinet all agreed the president had lost his marbles. Trump will get a physical sometime this month. It's unlikely the docs will test Trump for mental impairment, let alone disclose the results. We like to celebrate the robust-ness and resilience of our institutions to authoritarian assaults like the ones Trump has launched ("ban all Muslims"), but this is one place the institutions may be falling short.

Or not. The chairman of the House judiciary committee, a Trump sycophant, demanded a ton of secret information from the Mueller investigation, presumably to hand it over to the White House. The Justice Dept didn't turn it over and instead reached out the Speaker of the House, who is supposed to be able to rein in the committee guy. This is more information than most people want—Trump's hair is so much more fun—but the point is that the law and the institutions upholding it, wobbly though they may be sometimes, is coming out on top. So far.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat