Politicians will always choose inflation over austerity

The US yield advantage over the Bund narrowed. We may have the first step in a Hamas/Israel peace deal, although both parties are slippery as eels, and Trump lies. These are two reasons to wonder if a dollar pullback might not be in order, along with the Scaff indicating the move is getting overdone.

We will not be getting the usual Thursday jobless claims today because of the government shutdown. The earlier worries about the softening labor market remain if getting faded. What about inflation? Again, no hard data. The WSJ has a story today about how it’s not so that gold is up because of expected inflation—it’s up because of anxiety, falling rates in the US, and a bet on central banks diversifying away from Trump. Inflation expectations in surveys and swap pricing do not show a rise.

A lot of folks speak of debasement of the dollar. The WSJ tries to refute it. “But if investors expect debasement, it is very odd that the bond market’s best guess at long-run inflation—the so-called break-even inflation rate for the five years starting in five years’ time—is basically unchanged, and close to the Fed’s 2% target.

“… Aside from gold, the two obvious debasement trades are to bet on big, inappropriate rate cuts while selling the longest-dated Treasurys, and to bet on higher inflation breakevens, the gap between ordinary and inflation-linked Treasurys. Both should do well if the president seized control of the Federal Reserve and forced it to finance the government cheaply.

“There’s little sign of that happening yet. Sure, the 30-year Treasury yield has stuck mostly in a 4.5% to 5% range this year, higher than it’s been in a long time. But it is lower than at the start of the year and, like inflation-linked Treasury yields, lower than before the latest gold run-up began six weeks or so ago. Investors don’t expect persistent inflation to erode the value of Treasurys.”

The WSJ reporter says we have to distinguish between current conditions and the long-term problem of fiscal recklessness. Long-run, there could well be a bond market showdown. Politicians will always choose inflation over austerity.

“But that could be many years away. Right now, if the economy keeps on growing as fast as it has been and the jobs slowdown proves merely a blip, the Fed will have to abandon predicted rate cuts. It could even start raising them again. Stocks, bonds and gold would all suffer from the Fed hitting the brakes when they’re positioned for acceleration. Only if the Fed chose, or was forced, to let the economy keep moving too fast would the debasement trade come into its own.”

We have been fretting over this very issue for months, which can be summed up concisely as “where are the bond vigilantes?” We don’t know whether the 5-year breakeven rate has a good track forecasting track record, but given the current special circumstances, we doubt it does this time. Besides, betting markets are not hard data. Pitted against the bettors in the 5-year breakeven market are thousands of economists, nearly all of whom forecast that tariffs will drive inflation higher. Fiscal irresponsibility is another matter. When nearly everyone is doing it, the US dollar might not get singled out for debasement punishment.

Well, it already is. Dollar reserves held in custody at the NY Fed fell to the lowest in over a decade, despite TICS and the COFER report on reserve currencies holding up well and the superficial drop attributable to currency changes. But TICS was for July and COFER for Q2 while the NY Fed report is more current.

Reuters: “The latest figures show that the value of U.S. Treasuries held at the New York Fed on behalf of foreign central banks is $2.78 trillion. That's the lowest since August 2012, and down $130 billion in just two months.” There’s more, but you get the picture. Note when the drop began…

Forecast: Sometime soon the chickens will come home to roost, meaning the dollar will resume its downmove. The chart indicates it’s on its way, by which we mean days, not weeks. But this is pure speculation. We wouldn’t advise a long dollar position that can’t be exited fast.

Food for Thought: The distress cries are getting louder that equity prices are way, way too high. We now have JP Morgan Chase Jamie Dimon and IMF chief Georgieva warning that the risk to the global economy could be catastrophic if we get a big stock market correction.

Let’s admit it—Big Tech is a bubble, a classic bubble like Tulipmania. But you can’t leave just yet and if you don’t have some, you are a loser. So, what will be the trigger for the bubble to burst?

Sometimes bubbles burst because the business models are overly optimistic (1990’s internet craze). Sometimes they burst because those buying on margin get overextended and need to liquidate on a small and sometimes factually irrelevant downmove, setting off an avalanche. This is the sense in which low interest rates and abundant liquidity are actually bad for stock markets. Surely the Fed knows this.

When you ask Google AI for price vs. book, you get this: “As of October 8, 2025, Nvidia's (NVDA) stock price of $189.11 is significantly higher than its book value per share of $4.11, resulting in an exceptionally high price-to-book (P/B) ratio of approximately 45.77.

“This massive difference highlights the market's high expectations for Nvidia's future earnings and growth, which are primarily based on its leadership in the artificial intelligence (AI) and data center markets, rather than the liquidation value of its assets.”

Well, of course no one is speaking of liquidation. But check out the S&P 500 price to book—it’s about 5.3 to 5.61, depending on the source. So we have 5 vs over 45.

The current thinking is that Trump’s primary fuel is the US stock market rally. He doesn’t seem to care about anything else, like the Constitution or even his polling numbers. So the question becomes what action does he take and what loony proposals does he make when the bubble bursts?

Why should it burst? Two reasons: it always does, and the rally has become downright ridiculous. Here’s some info from Heisenberg that will curl your hair: “Tesla is ‘bigger’ than Indonesia; Meta than Australia and Spain; Amazon than Canada, Brazil and the entire French and German equity markets (considered separately); Apple than the UK; Microsoft than India; Nvidia than Japan, and the top five US stocks than all of that as well as Germany and the entire European equity market as proxied by the EuroStoxx 50.”

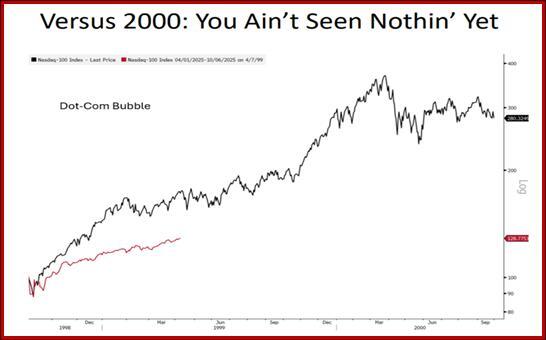

Be scared. But maybe not yet. See the chart from RenMac. The heading says it all.

Snack: Sanae Takaichi is likely the next PM in Japan and she is not holding back on asserting control over BoJ monetary policy. She said "The government must be responsible for fiscal and monetary policy. The BOJ will then consider the most appropriate means."

She said this over the last weekend after winning the LDP leadership and nobody can let it go. Reuters writes “Her leadership could present the biggest political challenge to Bank of Japan Governor Kazuo Ueda, a soft-spoken academic who took the helm two years ago charged with dismantling the radical monetary stimulus of his Abe-appointed predecessor.”

But she faces a rock and hard place. “Takaichi's presence will force the BOJ to delay rate hikes has already pushed the yen to an eight-month low per dollar, drawing verbal intervention by Japanese authorities. Takaichi may nod to a near-term rate hike if yen falls persist and threaten to push up already high living costs, said former BOJ executive Kazuo Momma, who oversaw negotiations with Abe's administration.

"’The biggest loser from a weak yen is the government,’ Momma said. ‘If Takaichi's approval ratings were to fall from the outset, it would be because of a weak yen. I'm sure people around her like Aso are well aware of that.’”

Hidden above is that critical word “intervention.” Betting can now begin on where the Japanese MoF will place the intervention line in the sand. Recently it was 150 or so but historically, the dollar/yen has been above that line a lot of times, just not since 1990. We had to draw the chart as quarterly just to see it (red horizontal line at 150).

For those not around 35 years ago, the US was having a kind of trade war with Japan starting in the late 1980’s over Japan’s huge surplus. This was more about chips and electronics than cars, but one of the outcomes was Japanese car companies building factories in the US and giving us the splendid movie about culture clash, Gung Ho (Michael Keaton). At one point in 1989, the Imperial Palace was theoretically worth more than the state of California.

The expected next LDP government under the leadership of a hawk wants to create a new asset bubble with wild fiscal spending/stimulus, rates not higher, and higher inflation. Inflationary economies get devalued currencies, or so the old rubric goes. It’s not obvious this will be the actual outcome, but it’s the fear. In practice, Japan probably needs institutional reform more than a different monetary policy.

As the news leaks out on the exact policies, assuming the fear is realized, there is no reason the dollar/yen cannot go to 160/170. But a warning: the Japanese establishment does not think like American economists. They have different perceptions and values and are miles better at compromise.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat