Policy Response Monitor: What has been done and what still have left

Monetary Response

March 3: FOMC cut FFR 50 bps to 1.00-1.25%; unanimous decision

March 9: NY Fed increased overnight repo offering from $100B to $150B and increased two-week term repo operation from $20B to $45B

March 11: NY Fed increased overnight repo offering from $150B to

$175B and added three one-month term repo operations at $50B

March 12: NY Fed switched reserve management purchases from T-bills to all Treasury securities, introduced weekly one-month and three-month term repo operations at $500B each

March 15: FOMC meeting

Cut FFR 100 bps to zero lower bound (0.00-0.25%); Mester dissented

Restarted Quantitative Easing (QE); increased Treasury and mortgage-

backed securities (MBS) holdings by at least $500B and $200B

Cut primary credit rate (discount window) 150 bps to 0.25%

Depository institutions may borrow from discount window for 90 days, repayable & renewable by the borrower on a daily basis

Reduced reserve requirement ratios to 0.00%

Reduced rate on standing U.S. dollar liquidity swaps from OIS+50 bps to OIS+25 bps (BoC, BoE, BoJ, ECB, SNB)

March 17: Regulatory agencies encouraged banking organizations to use capital & liquidity buffers

March 17: FRB established Commercial Paper Funding Facility (CPFF)

March 17: FRB established Primary Dealer Credit Facility (PDCF)

March 18: FRB established Money Market Mutual Fund Liquidity Facility (MMLF)

March 19: Fed expanded U.S. dollar liquidity swap arrangements to nine additional central banks

March 20: Fed, BoC, BoE, BoJ & ECB further enhance swap lines by increasing frequency of 7-day maturity operations from weekly to daily

Potential Monetary Response

Forward guidance to signal FFR will remain at 0%

Additional QE purchases of Treasury and MBS

Request authority from Congress to purchase corporate bonds

Purchase short-term municipal bonds (six months or less to maturity)

Reinstate the the Money Market Investor Funding Facility (MMIFF), the Term Securities Lending Facility (TSLF), and/or Term Asset- Backed Securities Loan Facility (TALF)

Adopt a negative fed funds rate, though we view this as unlikely

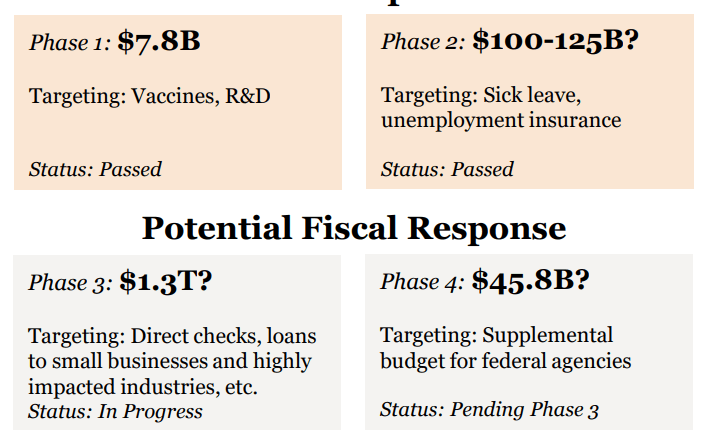

Fiscal Response

Author

Wells Fargo Research Team

Wells Fargo