PCE report: FX market reacts as expected, but surprises linger in the details

Outlook: We got the expected FX market jumps from the PCE report, but prices changed only a little from before the release for much of the day. Bloomberg calls inflation sticky and the report a relief, containing no surprises. We are not so sure. Maybe it will take a while for those core services prices to hit home. See the numbers.

The WSJ tried to be cute with an essay asking which is true, CPI or PCE? It flops (Bloomberg keeps the cuteness trophy) but does point out that 31% of the CPI is housing whereas housing is only 15% of the PCE.

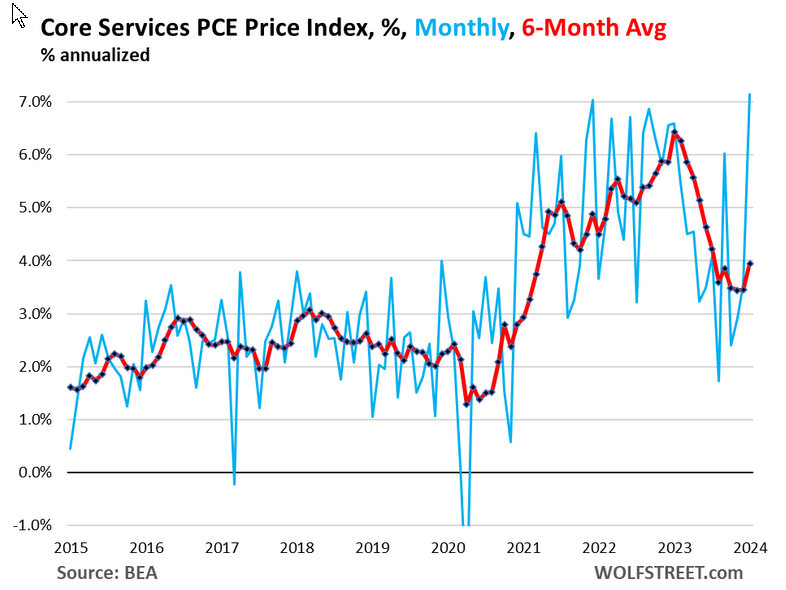

WolfStreet wrote “Powell is going to have a cow” over core services and while we don’t want to exaggerate a single piece of data, the numbers do point to a jolly good excuse for additional delay—July, instead of June. At of 4 pm yesterday, the CME FedWatch tool shows exactly that—only a 18.9% probability of a June cut from 51.4% a month ago, with July getting a 52.8% chance of the cut from 11.6% a month ago.

A little strangely, the 10-year yield failed to respond as might have been expected—from 4.315% at 8 am to 4.24% by 4:15 pm.

Besides, the economy is still pretty hot. The Atlanta Fed GDPNow has 2.9% for Q1, down from 3.2% two days ago. This is still far higher than the Fed and most big bank forecasters have been assuming. We get another stab at it today.

On a separate line of thought, yesterday the FX market decided to believe the hints and whispers about the BoJ dropping the zero rate policy and/or curve control. The earliest this has been expected is April, after the fiscal year ends on March 31. Then overnight BoJ chief Ueda said yes, he is looking for confirmation of the sustainable inflation rate but "I don't think we are there yet."

This was taken as a denial of any policy action right away, although honestly, it adds nothing. We wonder if trader instincts need to be heeded and today’s pushback will get followed by a series of alternating pushme/pullyou dollar/yen moves. In a way, this could well be exactly what the Finance Ministry and BoJ want—lots of advance notice (=”transparency”).

Forecast: The dollar “should” be the beneficiary of additional delay in the rate cut race as well as obviously higher resilience and growth prospects. Today, however, could be a stalled Friday and new positioning not on the deck until next week, when we get the usual labor market plateful, including JOLTS, ADP, and nonfarm payrolls.

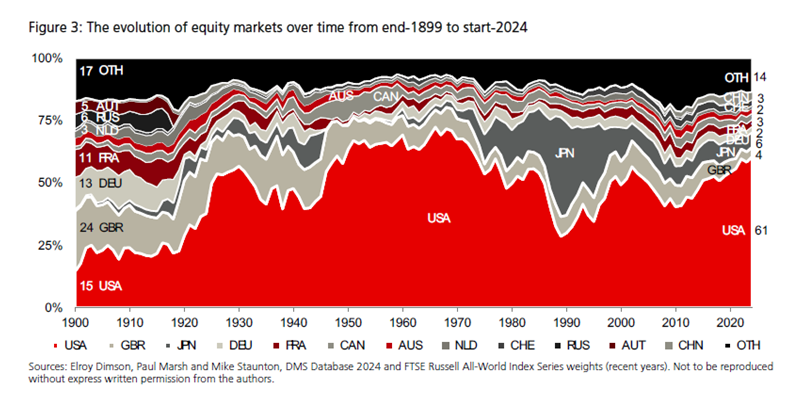

Tidbit: Bloomberg’s Authers writes that Dimson et al. have released the latest 25th edition of Global Investment Returns Yearbook 2024, the follow-though of their astounding book showing returns on everything starting in the 1700’s (https://www.ubs.com/global/en/investment-bank/in-focus/2024/global-investment-returns-yearbook.html). That original books cost over $200 and still sits on my bookshelf if anyone wants it.

There is a lot of interesting stuff in their work, including the observation that the top ten stocks in an index are often, if not usually, the majority of the trading volume, so our current Top Seven in the US is not, historically, unusual or a cause for worry. Other countries’ indices are more top-heavy. But we like the chart copied here showing the US stock market as seriously dominant among all equity markets worldwide, with Japan a challenger around 1990 but losing momentum. This is one hell of a chart.

Another chart, not shown here, has railroads the biggest slice of the pie in 1900 while in 2024, it’s technology. Industrials never made it to more than 25% in 1900 and is, of course, even smaller today. We should remember that when contemplating the de-industrialization of the heartland.

Fun Tidbit: Fromer Australian PM Turnbull is all over US TV for the second day, having described Trump’s adoration of Putin at global leader meetings as like a 12-year old boy meeting the high school football captain—and it’s “creepy.” He points out that all the free nations are worried about the prospect of Trump II.

Separately, the FT reports that Trump is trying to grab more shares of the soon-to-be-IPO’d “communications” company he had set up for him. The other shareholders, who actually did the work, are suing on the grounds there is no basis for Trump suddenly to get ten times the stock. The motivation is obvious—a huge gain in the stock price that will give Trump the money he needs to post as bonds in two court cases that he has lost. Well, does an IPO stock still go up when the world knows the biggest shareholder intends to sell and PDQ?

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat