PCE inflation is forecast higher

Outlook

The US data plate is full today, with personal income and spending for May, the PCE deflators, and the U of Michigan consumer confidence index. PCE inflation is forecast higher with the PCE as high as 3.9% (Bloomberg). It’s the PCE itself and not the core PCE the Fed watches, but never mind.

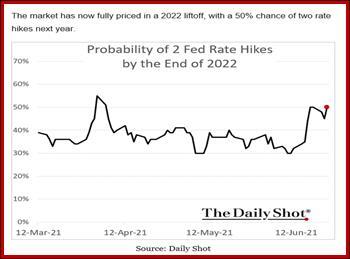

Bloomberg also writes that the Fed is split on upcoming tapering/hikes, with one camp saying “steady as she goes” and the other camp egging the policy committee on to faster action. We are not sure this qualifies as a “conflict” unless and the until the Fed sees it that way, and remember, Feds have the same freedom of speech as everyone else. The only time a conflict arose between the Fed chief and the rest of the members was when the members outvoted Paul Volcker and he resigned (1987). In other words, difference of opinion are normal and we should avoid buying into Bloomberg’s sell-newspapers hype.

Bloomberg chooses Kaplan to follow with the headline “Fed’s Kaplan sees hikes in 2022, Taper starting sooner.” Earlier this week, Atlanta Fed Pres “Bostic said the taper decision may come in the next few months and he expects the Fed to first hike rates in late 2022.” So there’s two.

While we like to be snide about news content so heavily embedded with opinion, Bloomberg is probably right. And the reason is that the transitory inflation story has some big holes. Supply chain delays and rising shipping costs are not going away quickly. The chip shortage that impeded auto output may drive used and new car prices even higher. Commodity prices are sometimes scary even if lumber came down. It’s not trivial that China is imposing regs on commodities. Demand for all kinds of raw materials from the infrastructure spending can’t be inflation-neutral.

And most tellingly, rentals and house prices are a problem, even if the US reports data in such a way as to obscure. Only a handful of central banks admit they have a housing bubble–New Zealand and Canada are the only two who say it’s an issue and poses moral hazard. WolfStreet illustrates why economics is not always such a pain to slog through with this: “It is just so much fun to watch central banks denying that there are housing bubbles, and even if there were housing bubbles, denying that they could be seen, and even if they could be seen, denying that monetary policies are responsible for them, and even if monetary policies are responsible for them, denying that monetary policies could be used to deflate them or prevent them in the first place.

“Central banks say this after spending years repressing short-term interest rates via their policy rates – often now into the negative – and repressing long-term interest rates via asset purchases, including housing bond purchases, such as MBS, and thereby driving down mortgage rates, which then trigger enormous price increases and soon housing bubbles.

“This is a huge accomplishment by central banks to pull off – denying that bubbles exist and then denying, after their existence can no longer be denied, that central bank monetary policies caused them, and then denying that central bank monetary policies could fix those bubbles (by raising rates and unwinding their holdings of securities).”

Wolf then replicates the Bloomberg Housing Bubble table, in which Norway comes 4th and the US comes 7th–but the US is bigger than the first six combined.

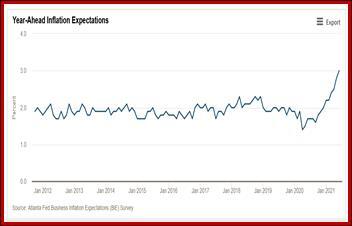

And in the end, ultra-high growth stresses supply in general. The latest Atlanta Fed GDPNow isa wild 9.7% for Q2, and that’s down from 10.3% on June 16 and over 13% in May. We get a new estimate today. The Atlanta Fed generally overshoots but is quite reliable. Its separate business survey of year-ahead inflation expectations is up to 3% in June, from just over 2% since 2012.

This means we do buy into the early taper/hike narrative, and if and when the market comes to buy it, too, yields should respond. While the correlation of yields and currencies is weak, it’s not dead. We see the dollar recovering, pushed along by an overbought condition in some of the majors, including sterling and the euro. Commodities currencies may be an exception, and the Swiss franc can regain its safe-haven star rating.

Tidbits: Yesterday a court suspended Trump lawyer Giuliani’s license to practice law because he lied about the election being fraudulent, and keeps lying, a threat to the public.

Today we hear the number of years the cop who killed Floyd George will serve in prison. The max is 40 years. We’re betting on 12. This is also the due date for the report on UFO’s that the tinfoil hat gang has been awaiting for decades. We can forecast with confidence the outcome will be “not disproved but no hard evidence.” We may also find out what caused the Miami apartment building to collapse. We expect it’s a sinkhole and/or low quality construction materials.

A week from Monday, July 5, the US celebrates Independence Day, and all markets are closed. We will not publish reports. Many will take the Friday before as a vacation day, too, and market activity will be thin by noon on Thursday.

The US Infrastructure Plan (so far): The deal is rickety and not actually a deal yet, and does not include new taxes on corporations and the rich. The deal comes in two parts, the spending approved yesterday with 5 Senators (10 or 12 are actually needed) plus an additional bill to be passed by the House alone and sent through on “reconciliation,” aka “sausages.” Here are some of the items, from the WSJ:

-

$201 billion in water, sewer, power and environmental projects.

-

$109 billion in road and bridge projects.

-

$66 billion in rail projects and $49 billion for public transit.

-

$65 billion for broadband infrastructure.

-

$47 billion for “resilience” projects to cope with climate change.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat