Payrolls on Friday is pretty much the only thing that counts

Outlook

Today’s upcoming US news is the August manufacturing PMI from both S&P and ISM.

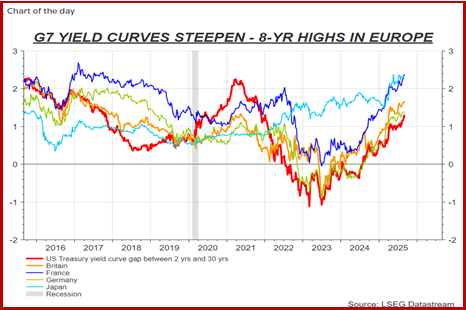

We are seeing a burst of uncertainty and not just in the US. In the US, yields are taking off all along the curve, with the 30-year near 5% again and the highest since July. The 2-30 yield curve is the steepest in nearly four years, according to Reuters. One report says the jump is due to the US perhaps having to repay the tariff proceeds because of the latest court ruling, but that seems fanciful. The classic reasons will do just fine—inflationary pressure, over-indebtedness due to a reckless budget, threats to the Fed, and all the other Trump mismanagement.

Elsewhere, the French 30-year hit the highest in 16 years as the government struggles to get a budget compromise behind the scenes and faces and faces a vote of no confidence on Sept 8. In the UK, Reuters reports “Britain's 30-year borrowing costs rose to their highest levels since 1998 and sterling slid more than 1% on Tuesday, with this week's reshuffle of PM Keir Starmer's economic team ahead of the Autumn budget raising questions about the position of Chancellor Rachel Reeves.”

See Dolan’s chart of the day displaying the yield gains.

Payrolls on Friday is pretty much the only thing that counts, apart from some new grotesque thing from Trump. We know the data is wonky but have to respond to it anyway. SocGen’s Juckes says the US economy needs payrolls growth of about 130,000 to keep GDP on track at about 2.1%--but the current numbers point to under 1%. One story had 35,000-40,000 as an estimate for Friday. The consensus seems to be about 75,000. Firms are not firing all that much but not hiring, either, out of knees shaking from Trump-driven uncertainty. And will we be able to trust the numbers now he has fired the head of the BLS?

Finally, a US government shutdown looms again at Sept month-end unless Congress can pass a stop-gap “continuing resolution.” The Republicans need some Dem votes to get it done but the Dems are digging in their heels deeper by the day as Trump delivers yet another stupid initiative, this time ending foreign aid (which is less than 1% of the total budget). As we have seen many times before, a US government shutdown has very little effect on financial markets. It might be different this time if anyone had confidence the Dems could deliver a robust opposition.

Forecast

We can think of a dozen reasons why traders should shun the dollar this week, starting with the loss of confidence in the US government, the rising expectation of a rate cut on Sept 17, the takeover of the BLS and maybe the Fed by unqualified Trump lackeys, firing the scientists at the health agencies to favor the crackpots, and exhaustion from the endless parade of crass attention-seeking by the four-year-old in chief.

The probability of the Sept rate hike rose again to 89.6 as of Monday evening from 87.1 Friday morning. The probability of a total of three cuts or more by June of next year is 73.2% when everything is added together. Apparently the bettors think inflation will not be anything special or the Fed will see we are at risk of recession. Or maybe they see zero risk of recession now that the Atlanta Fed sees Q3 GDP at a whopping 3.5%, strong enough for a rate cut.

Offsetting the bad karma is the Treasury market, with the 10-year climbing back up again after bottoming in early August and again last week. This is due partly to the Treasury’s logistics, partly to the state of the stock market, partly to inflation fear, and partly to the absence of good alternatives.

Which has more muscle—revulsion at Trump, especially his getting the rate cut he seeks in two weeks, or rising yields? History tells us to put our ten cents on the yields. That means the dollar gain can get bigger. We don’t like it. We tend to take losses when the dollar gains and then reverses fast, as it has done several times since Trump came along.

A story now hitting the mainstream has it that foreign central banks have more gold than US Treasuries for the first time since 1996. We don’t know what this means or even if it’s measured correctly. After all, the price of gold in 1996 was a lot lower than now ($385 or so), so if it’s marked to current prices, of course that could be true—and meaningless. The bigger point is they are still showing up in droves for the auctions.

Tidbit: TreasSec Bessent said the government doesn’t want to interfere in local and state affairs (really?), but is thinking about declaring a housing emergency in the fall that would “standardize local building and zoning codes and decrease closing costs,” according to Bloomberg. Together with rate cuts, housing affordability could get better and end the housing crisis. Yeah, and allow flood, hurricane, wildfire and tornado areas to do without protections—while Trump has taken away the ability of the weather service to issue alerts and FEMA from going in to rescues.

Tidbit: We can’t find a poll showing approval ratings for Trump from Europe and elsewhere in the world but inside the borders, the Economist reports “225 days into Donald Trump's term, the president's net approval rating is -14%, up 0.9 points since last week. 41% approve, 56% disapprove, 4% not sure. In July, the Guardian noted that the Nazis took over in the late 1930’s with an approval rating of 38%.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat