OPEC oil cut extension unlikely to add much NOK support

-

We look for Organisation of Petroleum Exporting Countries (OPEC) and non- OPEC supply cuts to be extended, with limited upside impact on oil prices.

-

We expect Brent crude to trade around USD50-54/bl near term and rise to around USD60/bl in 2018.

-

The NOK should benefit only marginally from an extension. Meanwhile, weaker global demand/the OPEC meeting pose downside risks to our NOK-forecasts.

-

Strategy: Leverage funds should look to buy NOK strategically but tactically we prefer a side-lined stance. NOK volatility looks cheap. Corporates with long NOK (short FX) exposure should protect themselves against tail risk in the next 3M.

FX economics

Extension of supply cuts about priced

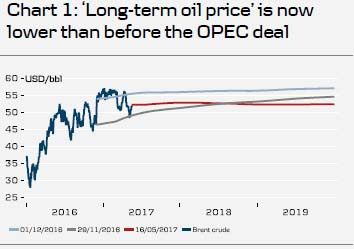

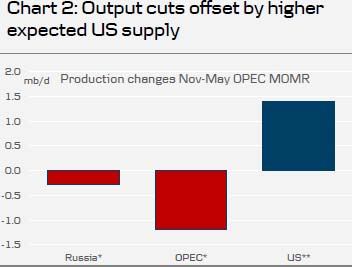

We expect the deal between OPEC and the 11 oil-producing countries outside OPEC to be extended when OPEC meets on 25 May. This has been more or less confirmed by recent comments, e.g. from Russia and Saudi Arabia, which have further hinted that the deal may be extended until March 2018. In our view, the market is about priced for an extension of supply cuts next week, although there is likely still to be some uncertainty about whether it will be for six or nine months. Positioning remains net long oil, which further backs our view and implied volatility at significant lower levels compared with 2016. Hence, if we are right that supply cuts will be extended, we see limited near-term price reaction and expect Brent crude to trade close to current levels (i.e. remain in the USD50-54/bl range). In the unlikely event the deal is not extended, we expect the price of Brent crude to fall to USD45/bl, which is close to the recent intraday low in May when markets priced out extension expectations. Medium term, we are still looking for the price of Brent crude to rise to around USD60/bl in 2018 on a lower USD and steadily rising demand. This is around 10-15% above current pricing in the oil forward market. In the big picture, supply cuts have had, and should continue to have, a limited impact on prices, while they have led to a shift of market share from OPEC and Russia to the US (see Charts 1 and 2).

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.