OPEC Meeting Preview: Do production cuts mean higher crude prices?

- OPEC's current production cuts of 1.2 million barrels a day expire in March 2020.

- Iraq has proposed an additional 400,000 barrels in reductions.

- Many US shale drillers have debt pressure from low crude prices.

Crude oil prices rose more than 4% on Wednesday but the reason, a larger drop in US inventories than forecast, underlines the dilemma facing OPEC members when they meet in Vienna.

Production cuts by the oil cartel and several associated nations are no longer a reliable means of influencing global oil prices. OPEC’s problem is that its members and Russia only control about half of the world’s production and alone that is not enough to force prices higher by restricting supply.

The 1.2 million barrels a day in production cuts that OPEC and its allies, known as OPEC+, which includes Russia, instituted at the beginning of the year expire in March 2020 and the 14-member group must decide whether to extend or deepen the reductions. Iraq’s oil minister Thamer Ghadhban has advocated an additional 400,000 in reductions despite its poor record of implementing its share of the current cutbacks.

Saudi Arabia, OPEC’s biggest producer was reported to be considering deeper cuts as a means of supporting the stock offering prices of Aramco as it goes public. The new Energy Minister Prince Abdul-Aziz bin Salman declined to answer questions on the Iraqi proposal as he arrived in Vienna, just noting that the market outlook was “sunny,” as quoted by Bloomberg.

The alliance between the Organization of Petroleum Exporting Countries, Russia, Kazakhstan and others is expected to continue the restrictions through the end of next year.

The US is now the world’s largest producer of crude oil having outstripped Saudi Arabia and Russia formerly the numbers one and two. It is North American shale producers that responded to the OPEC cuts by ramping up drilling so that the US became a net exporter of oil for the first time in 70 years.

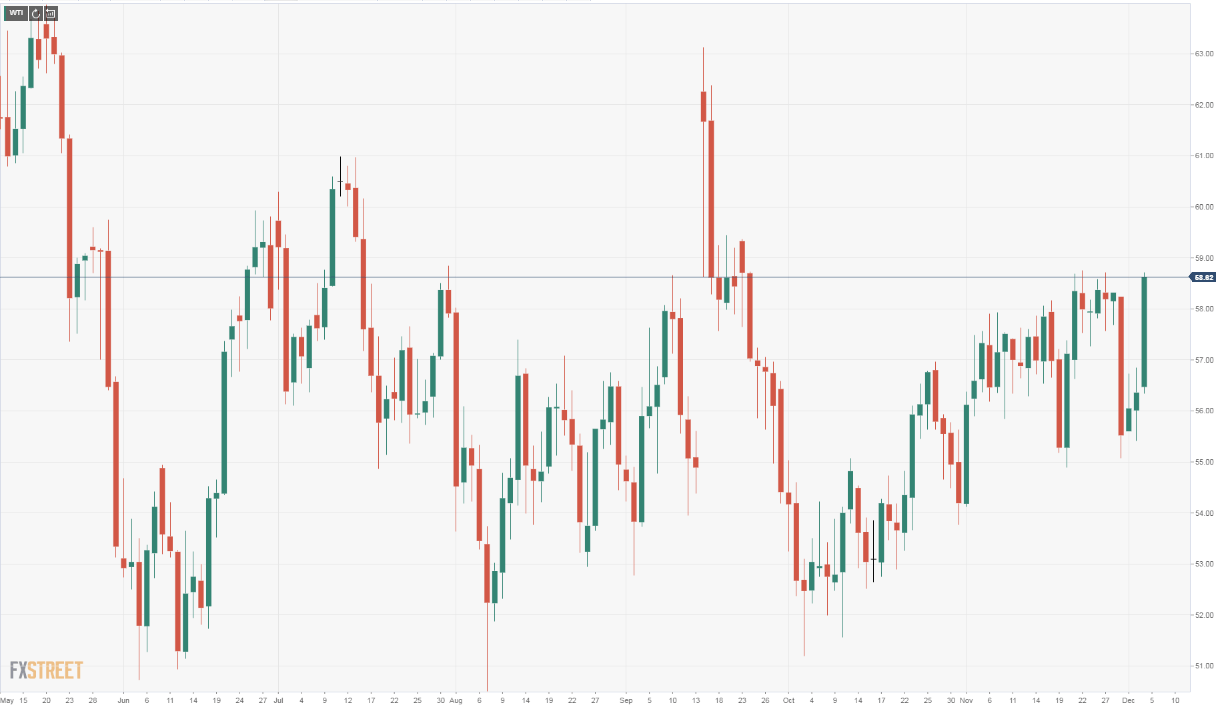

West Texas Intermediate (WTI) the US price standard has traded in a relatively limited $52 to $61 range since late May and for much of that six month period the price action was contained in a narrower $53-$59 band.

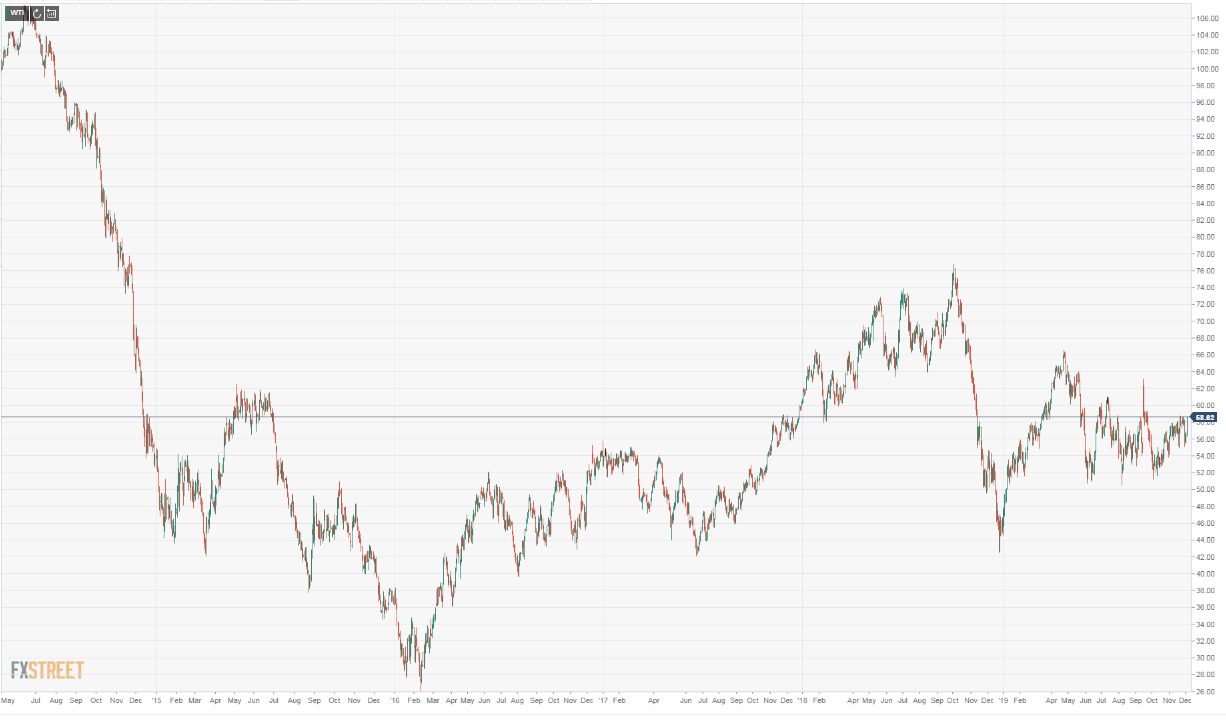

The rise in the WTI barrel price in the first half of this year from below $45 in late December 2018 to just over $66 by the end of April coincided with the implementation of the OPEC production cuts.

But the price increase was due far more to demand factors from the relatively optimistic global economic picture at the time and the prospective increase in demand from the seemingly positive US-China trade negotiations than to the OPEC reductions.

As the global economic outlook has darkened in the second half the WTI price has dropped sharply, unimpeded by the OPEC production cuts which remain in effect. Much of the crude output lost to the cartel was replaced by increased US and Canadian shale operations.

There is, however a complication to the surge in North American crude production. Shale drilling and the fracking process which makes it possible is expensive, at least compared to the low cost existing Middle Eastern fields.

Shares of energy companies particularly shale drillers, have dropped precipitously this year and the reason is the price of oil. Many US producers have extensive debt and the mid-$50 dollar WTI price range is not enough to provide the cash flow needed for service and the margin desired by equity investors.

If OPEC succeeds in raising the price of crude oil its members could be throwing a lifeline to its most successful competitors. Whatever choice OPEC makes the oil business is unlikely to escape the truth of the economic notion, ‘The solution to high prices is high prices.’

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.