Oil stock investors batten down the hatches

This week’s energy world drama is another reminder that all things oil-related can be slippery.

Earlier in the year, OPEC lynchpin Saudi Arabia let it be known that it wanted to see crude oil around $60 a barrel (bbl). Instead, oil has seen its biggest drop in the first half of any year since 1997, with Brent this week bottoming at a seven month low of $45.35. We all know what went wrong, but not even OPEC itself seems to know why. Twenty two straight weeks of higher and higher oil rig counts is a clear enough message that the cartel’s supply agreement isn’t working.

The main price tipping points:

- Year-high inventories in Europe’s main hub

- Supply-cut exempt Nigeria nearing the highest oil exports for 17 months

- U.S. crude oil production (52% from shale in 2016) rising to 9.35 million barrels a day, close to Russia and Saudi levels, despite two consecutive weeks of falling inventories

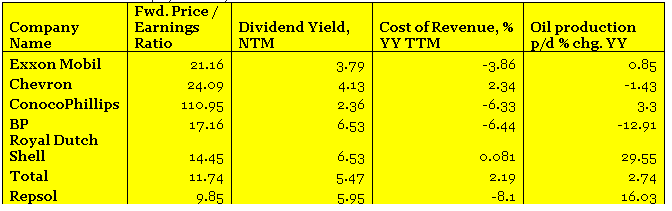

Big Oil falls hard

For investors in Big Oil, worries that were all but put to sleep earlier in the year have now been dusted off. There’s a bigger chance that stocks of most oil producers will fail to rise this year, after gaining in 2016. Of 18 U.S. and European oil majors, only two, Marathon Petroleum and Spain’s Repsol are trading higher so far this year. They’re up a meagre 4% and 2% respectively and have been sliding since late May. (Marathon’s parent co., Marathon Oil is down 33% year-to-date).

More than ever, cost efficiency and oil production growth will be in the spotlight. Investors will tend to stick with companies that slash the most costs and pump the most oil to maximise cash flow as prices relapse. The table below shows production growth and revenue costs for western European and U.S. oil ‘supermajors’, together with forward price/earnings ratios and forecast dividend yield.

OIL ‘SUPERMAJORS’ P/E, YIELD, REVENUE COST AND PRODUCTION GROWTH

Source: Thomson Reuters and City Index

Key takeaways

- One possible explanation emerges for why Repsol stock has outperformed its peer group: it has managed to reduce costs marginally whilst ramping up production at the second highest rate

- World No.1 Exxon barely increased production in its last fiscal year, and an already hefty (for Exxon) circa 4% cost reduction looks hard to repeat

- Shell’s BG buy added an exponential amount of barrels of oil equivalent production in one fell swoop, whilst costs were flat. A ‘fear discount’ is still weighing on its rating (P/E) after the giant acquisition. But investors may find it is a cheaper play for similar yield than its arch rival (Exxon) as oil price uncertainty continues

Author

Ken Odeluga

CityIndex

Ken Odeluga has over 15 years' experience of reporting and analysing global financial markets.