Oil prices plunge due to tariff-related demand worries and increased OPEC+ supply

Oil prices have sold off heavily as the market deals with a potential demand hit from tariffs and a surprise supply increase from OPEC+. Stronger supply and demand uncertainty has led us to lower our oil forecasts for the remainder of the year. Further downside risks remain.

OPEC+ surprise decision

Oil prices are under significant pressure, with Brent witnessing its largest sell-off since August 2022. Front-month prices are trading below US$70/bbl. Worse-than-expected reciprocal tariffs from the US have raised demand fears. However, OPEC+ has only added to these concerns by announcing a larger-than-expected supply increase for May.

Under the current production plan, OPEC+ was set to gradually bring 2.2m b/d of additional supply back onto the market from April 2025 until September 2026. The supply increase for April is 138k b/d, while the group was meant to increase supply by a further 135k b/d for May.

However, the group surprised the market after a video conference between members on Thursday, where it was thought the main discussion point would be to ensure that members stick to their production targets. How wrong the market was. Instead, the group announced it would increase the oil supply by 411k b/d in May. The group attributed the increase to healthy market fundamentals and a “positive market outlook”. This is strange given that, if anything, there is more uncertainty for the market, particularly when it comes to demand after the US tariff announcement.

OPEC+ is set to next meet on 5 May, where it will decide on June production levels.

Why has OPEC+ decided on a larger-than-expected increase?

While OPEC+ said the supply increase is due to a more positive outlook, it seems there is more behind this move.

Firstly, US President Trump is taking a more hawkish view towards Iran and Venezuela with stricter sanctions. OPEC+ might feel that this provides it with the opportunity to increase supply. OPEC+ might see this as an opportunity to boost supply, especially after Trump announced secondary tariffs for buyers of Venezuelan oil and threatened similar measures for buyers of Iranian and, potentially, Russian oil.

Secondly, it is no secret that Trump wants lower oil prices and has pressured the Saudis to boost supply. This recent move might indicate that Trump has been more successful than many anticipated in persuading the Saudis to increase supply.

Finally, there are also suggestions that the group decided to increase supply to punish members who have been consistently producing above their production targets. Iraq has been guilty of doing this in the past, while more recently, Kazakhstan has been producing well above its production targets. Members who have produced above their production targets have agreed to compensation cuts, however, yesterday’s move could suggest that there is little belief that members will actually follow through with these compensation plans.

What this supply increase means for prices

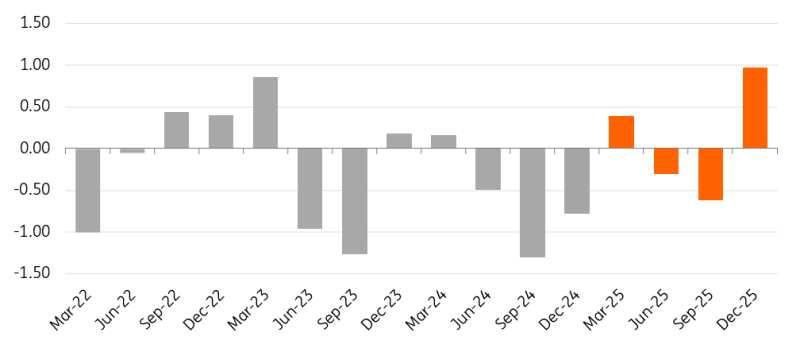

The move leaves the oil balance better supplied over the second quarter, with 134k b/d of additional supply compared to previous expectations. However, there is still uncertainty around this. It is unclear what the group decides to do with production from June onwards. We will have to wait until early May for a decision on this.

In our forecast, we assume the group will look to keep output steady over June and July and then continue with its gradual unwinding from August onwards. The clear downside risk is that rather than pausing supply increases after May, the group brings forward the gradual increases by two months. This would only further increase the expected surplus over 2025, particularly in the fourth quarter.

Adding to the uncertainty is the demand picture, which has deteriorated this year. Demand estimates have been trimmed as we have moved through the first quarter, and the announcement of reciprocal tariffs means that further potential revisions lower in demand are likely, given the impact that tariff escalation will have on global growth. For now, we assume that oil demand grows by 1m b/d with risks skewed to the downside.

As a result, we have cut our 2025 average Brent forecast from US$74/bbl to $72/bbl, while our 4Q25 forecast has been lowered from $71/bbl to $68/bbl. For now, our balance continues to show a modest deficit over 2Q25 and 3Q25, supporting our view that prices over this period should move modestly higher from current levels. However, this can change quickly, depending on OPEC+ policy and demand developments.

Global Oil balance looking increasingly comfortable towards the end of the year (m b/d)

Source: ING Research, IEA, EIA, OPEC

Sanctions remain an upside risk

The threat of supply disruptions due to sanctions is likely to linger, particularly when it comes to the Venezuelan and Iranian oil supplies. While Trump has threatened secondary tariffs on buyers of Russian oil, we feel this is unlikely. It would significantly tighten the market, with Russia exporting more than 7m b/d of crude oil and refined products. Losing a large share of this supply would propel prices higher.

Markets would be able to deal with the loss of the Venezuelan oil supply, with OPEC having more than ample spare capacity to make up for this loss. It is a similar story if we are to lose a large share of the Iranian oil supply. However, the uncertainty is whether OPEC would be keen to further tap into spare capacity or wait to see prices rise before bringing further supply online. Recent developments suggest the group may go for the former, which would keep the US administration happy.

In the absence of OPEC spare capacity filling the gap, the loss of Venezuelan export supply and Iranian exports returning to 2022 levels would be more than enough to push the market into deficit and change the outlook for prices.

Lower prices stand in the way of stronger US supply growth

Current WTI price levels provide little incentive to US producers to increase drilling activity. If anything, we could see a further slowdown, particularly when you consider the backwardation in the market. Calendar 2025 prices are trading at a little under $65/bbl, while calendar 2026 is trading closer to $62/bbl. This leaves little incentive to US producers to drill. The latest Dallas Fed Energy survey shows that producers need on average $65/bbl to profitably drill a new well. Meanwhile, the average price needed to cover the operating costs of an existing well is $41/bbl. However, given the large decline rates in US shale, it is more important to focus on new well costs.

Current price levels mean it is unlikely that Trump is going to be successful in boosting domestic oil production. US oil producers are price sensitive. If Trump wants higher US oil production, we will need higher oil prices.

ING Oil price forecast

Source: ING Research

Read the original analysis: Oil prices plunge due to tariff-related demand worries and increased OPEC+ supply

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.