October CPI preview: Disinflation is getting harder

Summary

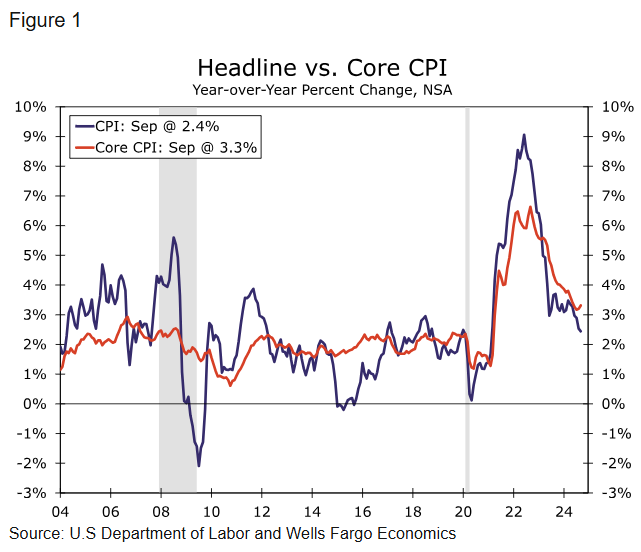

The October Consumer Price Index will likely show that progress in wringing out the last bit of inflation remains frustratingly slow. We look for headline CPI to have advanced 0.2% in October, which would bump up the 12-month change in consumer prices to 2.5%. Excluding food and energy, prices are likely to have increased 0.3% for a third consecutive month as another increase in goods prices coincides with glacial easing in services inflation.

Glacial slowing in services and firmer Goods prices bode poorly for overall inflation progress

The October CPI report will likely support the notion that the last mile of inflation's journey back to target will be the hardest. We look for the Consumer Price Index to have advanced 0.2% (0.21% unrounded) in October, causing the year-over-year rate to edge back up to 2.5% from 2.4% last month (Figure 1). Excluding food and energy, a third consecutive 0.3% monthly increase is expected to keep the core index up 3.3% year-over-year—still about one percentage point higher than its pre-pandemic pace.

A more temperate gain in food prices likely helped to keep October's headline gain in check. After grocery prices leapt 0.4% in September, we expect a slower rise in October (0.1%). About one-third of September's increase in food at home could be traced to eggs, but wholesale prices have eased in recent weeks, pointing to some giveback from September's hot reading. Amid a trend-like 0.3% rise in food away from home, we estimate the 12-month change in overall food inflation edged back down to 2.2%. Further offering consumers some reprieve was the continued easing of gas prices last month. We estimate energy goods prices fell roughly 1.4% in October and 13% from this time last year. However, the downdraft to overall inflation from energy is waning, and the risks to energy costs, at least for the time being, lie to the upside given geopolitical tensions in the Middle East.

Author

Wells Fargo Research Team

Wells Fargo