NZD to follow US yields, RBNZ to stay out of the way

The NZD is one of the most over-valued currencies compared to its long-run average real effective exchange rate and its historically low yield advantage. In a rising global yield environment, where global investors lose interest in squeezing every last bit of juice from somewhat higher yielding assets, the NZD should under-perform. Indeed, in recent months, the NZD has become more highly (negatively) correlated with US yields. But of course, US yields have fallen in the last two weeks as the Fed emphasized a gradual policy tightening cycle and Trump’s progress towards key policy goals stalls, contributing to a fall in the USD and recovery in NZD. Global growth indicators continue to improve, including export performance in Asia. The benign US Fed outlook, combined with improved growth indicators, has seen a further sharp rise in Asian equities and currencies. Buoyant global risk appetite is spilling over to stronger commodity currencies, including the NZD. New Zealand’s Q4 GDP reported last week was much below expected, suggesting that the RBNZ may sound more dovish at its policy statement this week. However, GDP is likely to bounce back this year. Underlying demand in the NZ economy remains strong, global conditions have improved, and the NZD is somewhat weaker since February. On the other hand, dairy prices have weakened and detract from an otherwise improved outlook for growth and inflation in New Zealand. The RBNZ will be wary of changing its language too much in its policy statement this week for fear of pushing the exchange rate higher.

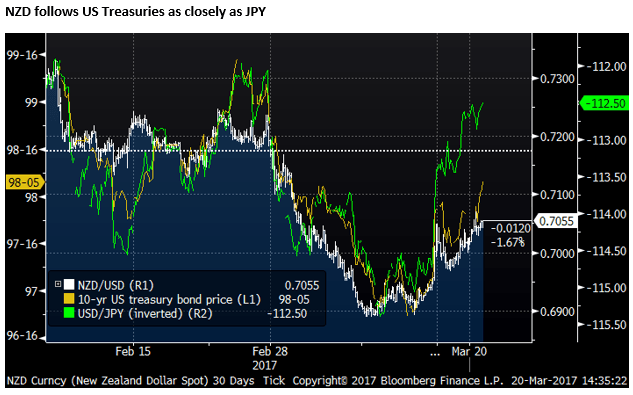

NZD correlation with US yields

I view NZD as one of the most over-valued currencies with respect to its long-run average and now small yield advantage (The US dollar is not overvalued). In a rising yield environment globally, and less investor focus on squeezing every last bit of juice from somewhat higher yielding assets, the NZD should under-perform.

Indeed in recent months, it appears that the NZD has become more (negatively) correlated to US Treasury yields, matching that of the USD/JPY. The NZD has firmed in recent days as US yields have fallen back from recent highs.

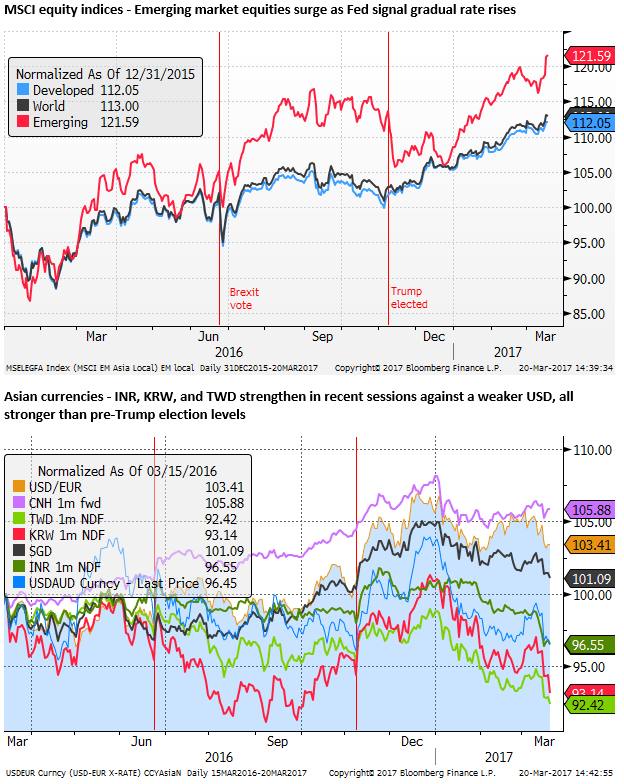

Strong Asia EM markets

The NZD can also draw strength from capital flows that move towards emerging market economies and commodity assets. A sense that a global recovery is gaining traction and the pace of US rate hikes will remain gradual and non-threatening does appear to have further boosted EM and commodity currencies since the Dovish Fed presentation of its 15 March rate hike.

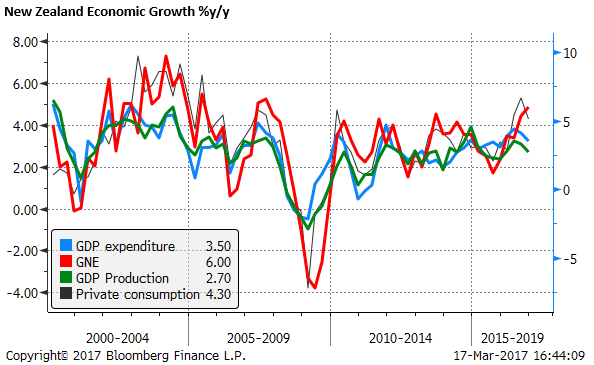

New Zealand – still strong domestic demand

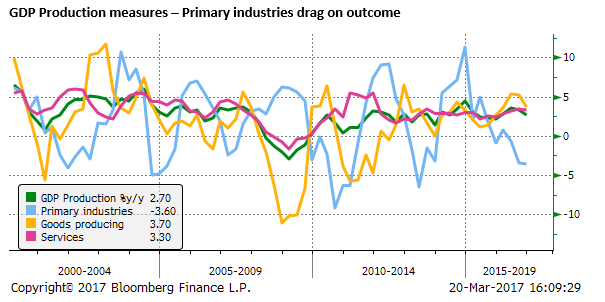

New Zealand Domestic economic conditions remain generally buoyant and supportive for the NZD. The most recent GDP outcome (+2.7%y/y in Q4) GDP was much below 3.2% expected. However, this reflected falls in production that are likely to reverse. The weak primary production, including dairy, says little about underlying demand in the economy.

In fact, stripping out net exports, a measure of domestic demand, GNE rose 6.0%y/y Q4-2016; a high since 2007. Private consumption was modest in Q4 (+0.4%q/q), but only after recent strong quarters; it rose 4.3% from a year-earlier.

Recent activity and survey indicators suggest the pace of growth in New Zealand remains on a solid path. GDP is likely to recover from the modest outcome in Q4.

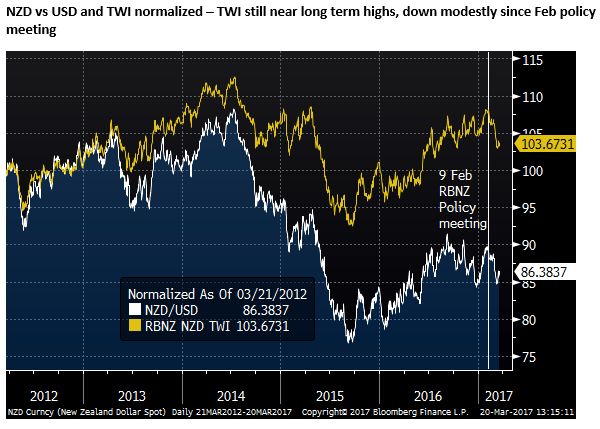

The RBNZ policy assessment on Thursday falls between quarterly statements on monetary policy. It is unlikely to deliver any surprises. The key message of a stable rates outlook, and a desire for a weaker exchange rate should remain. The statement hardly needs to be changed.

In its previous 9 Feb policy statement, the RBNZ was less hawkish than expected. It acknowledged that that inflation pressures were building and the global economy had improved. But it did not forecast any rise in rates until Q3-2019, toward the end of its three-year horizon.

Since February, global economic conditions appear to have firmed further, global inflation pressure may have lifted somewhat, and the NZD is modestly weaker. As such, the RBNZ may feel that the inflation outlook in New Zealand is somewhat higher. On the other hand, dairy prices have fallen significantly, weakening the domestic income outlook. On balance, the RBNZ would be cautious not to change its language too much in this statement. It would fear generating upward pressure on its exchange rate should it remove the cautious language in its policy assessment.

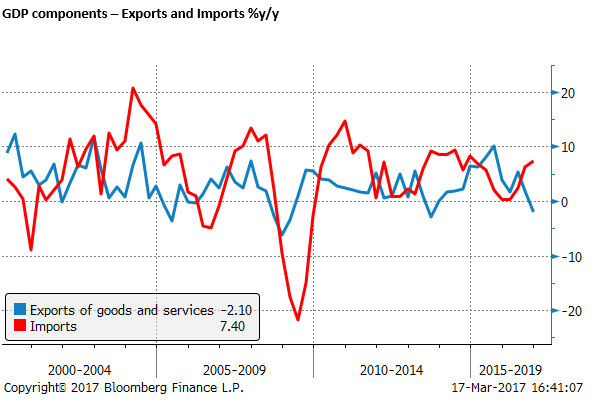

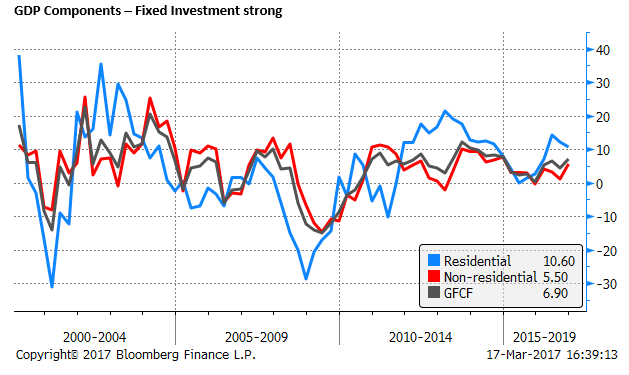

New Zealand GDP components

Export goods volumes had the biggest fall (-6.0q/q) since 1992, offset partially by a 2.1% rise in service exports. The biggest decline was dairy goods, although there was also a significant fall in manufactured goods exports. The weak export performance, particularly the manufactured goods component, may be indicative of a relatively expensive NZD exchange rate; likewise strong import growth. The trade performance is likely to keep the government and central bank in a mind to express a desire for a weaker exchange rate.

The key components of domestic demand were strong, private consumption rose 0.4%q/q and 4.3%y/y, Investment (GFCF) rose 0.7%q/q and 6.9%y/y. Government spending rose 1.1%q/q and 3.6%y/y.

Within Investment (GFCF), Residential investment took a pause in the quarter (+0.1%q/q), but was up 10.6%y/y. Non-residential (business) investment rose 1.8%q/q and 5.5%y/y.

Within business investment, Machinery and equipment investment rose 3.7%q/q and 1.8%y/y, non-residential building rose 5.0%q/q and 13.8%y/y.

Author

Greg Gibbs

Amplifying Global FX Capital

Greg has had a long career in foreign exchange. He began his career at the Reserve Bank of Australia in 1989 and in the early 1990s he was the first economics graduate at the Bank to be assigned to the foreign exchange dealing desk.