Norges Bank running out of hawkish ammunition to support the Krone

Norway’s central bank is getting closer to monetary easing, and at this week’s meeting the rate projections may well be revised lower. At the same time, we think policymakers will try to use all the remaining hawkish ammunition to support the currency, which has recently underperformed despite short- and medium-term drivers.

Norges Bank announces monetary policy on 19 September, and rates will almost certainly be kept on hold at 4.50%. That means that by the end of September, Norges Bank, the Reserve Bank of Australia (and obviously the Bank of Japan) will be the only G10 central banks not to have started easing policy. In Australia, the issue is that rates were not raised enough in the first place – and inflation remains a concern while in Norway, the central bank is dealing with a currency problem.

NOK remains cheap

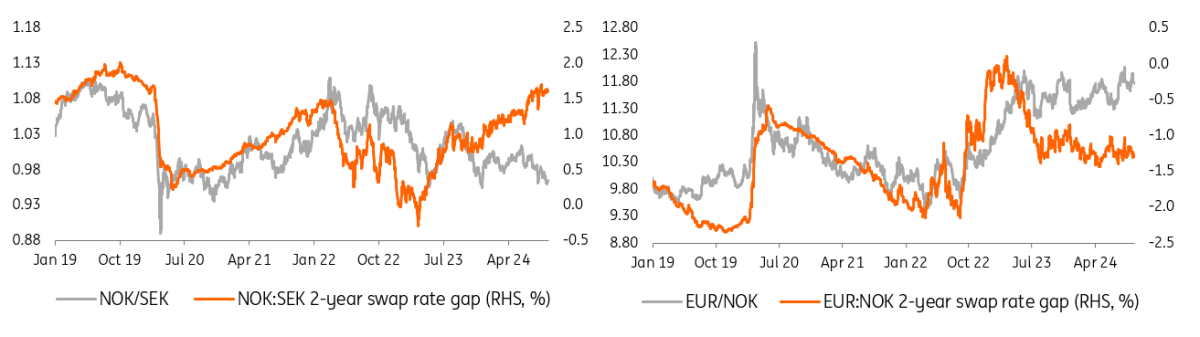

We admit the size and pace of the past three NOK selloffs (July, August and September) surprised us, especially in relative terms against its closest peer, Sweden's krona. NOK/SEK traded below 0.960 earlier this month and remains around the lowest since December when the Riksbank was artificially boosting SEK via FX hedging purchases. That’s despite short- and medium-term drivers which have instead argued for a stronger NOK against both SEK and EUR.

As shown below, NOK short-term swap rates are at pre-pandemic highs versus SEK’s. During the last two instances where the NOK-SEK 2Y swap rate gap was at 150bp or higher, NOK/SEK was trading at around 1.05, which is 9% above the current levels. Also, the difference between EUR/NOK and underlying short-term rate differentials is around the widest since the 2020 pandemic shock.

NOK should trade stronger against SEK and EUR

Source: ING, Refinitiv

In the medium run, terms of trade (price of exports/price of imports) differentials between countries are generally the most statistically relevant factor for exchange rates. Norway’s terms of trade has shrunk since the 2022 gas-led spike, but it is well above the five-year pre-Covid average. In contrast, terms of trade in the eurozone and Sweden have deteriorated compared to pre-pandemic levels. When we exclude the 2022 spike, Norway’s current account is at historical highs (17% of GDP).

The oil selloff is undoubtedly relevant for NOK, but our models show that even when accounting for the recent swings in crude prices, EUR/NOK is around 1.5% above its short-term fair value, and 6-7% above its medium-term fair value. We continue to believe that the lower liquidity of NOK compared to other G10 currencies is the key factor behind NOK’s volatility, as that allows speculative selling to be more effective.

The role of Norges Bank in FX

Turning to the role of the central bank, Norges Bank currently sells NOK 400m (c.USD 38m) a day as part of its FX purchases on behalf of the sovereign fund. That is much lower than NOK 1bn+ last year and the 4bn peak in 2022. The weaker oil prices mean that Norges Bank may trim FX purchases to zero in the coming months. All in all, we doubt that is materially contributing to NOK weakness.

At the same time, markets still have to receive a clear warning from the central bank on excessive downward speculation in NOK. The difference with the Riksbank is noticeable in this sense. One year ago, the Riksbank deployed a form of FX intervention through its reserve hedging programme, which proved effective in stabilising and then boosting the severely underperforming SEK. We think the threat of Riksbank tapping FX reserve hedging if EUR/SEK were to touch 12.00 again helped cap the pair’s rally around 11.80 in July.

A similar threat is not present in NOK markets. Back when rates were being raised across developed markets, Norges Bank used larger rate hikes to discourage NOK selling. That helped halt the EUR/NOK run at 12.0 last year. Now, rate hikes aren’t just out of the question, but markets are understandably doubting Norges Bank will be able to keep rates on hold for much longer, despite its FX-driven hawkish tone.

Norges Bank may have to give in to easing pressure

Looking at this week’s Norges Bank meeting, the question is whether Norges Bank will acknowledge a seemingly inevitable first rate cut by the end of the year. The latest indication is that rates will be held at the current levels for some time, but this time, Norges Bank releases an update of the rates projections as part of their Monetary Policy Report. It may include one rate cut (or a fraction of a cut) by year-end, effectively endorsing market pricing for 30bp of easing. Our call is for one 25bp rate cut by Norges Bank this year, most likely at the December meeting.

If the rate path is revised lower to include one 2024 cut, then we think Norges Bank will point to the risks that a weak krone will prevent monetary easing. That would effectively make the whole message more hawkish and could prevent another NOK selloff. However, as discussed above, it should also be insufficient to turn the tide for NOK by itself.

Read the original analysis: Norges Bank running out of hawkish ammunition to support the krone

Author

Francesco Pesole

ING Economic and Financial Analysis

Francesco is an FX Strategist and has been with the firm since May 2019. His main focus is on the G10 space and, in particular, commodity currencies. He began his career at Credit Agricole CIB and holds an MSc in Financial Markets and Investments