Non-Farm Payrolls Preview: Labor market defiance

- ADP posts 183,000 February jobs, January revised to 300,000 from 213,000

- Jobless claims 4-week moving average of 229,000 signals strong labor market

- February payrolls to moderate from January’s 304,000 surge

The US Labor Department will release its Employment Situation Report for February on Friday March 8th at 8:30 am EST, 13:30 GMT.

Often referred to simply as non-farm payrolls for its headline statistic, the widely followed monthly report tracks the condition of US labor markets through figures on job creation, unemployment, average hourly earnings, labor force participation, average work week and others. The non-farm payroll number is the most closely followed and traded US economic statistic. The report is one of most timely of the hard data series as its information is just one month old.

The report consists of the establishment survey and the household survey. The establishment survey polls non-farm businesses for the number of employees, their compensation, hours and other attributes of employment. This survey produces the payroll, wage, participation and other numbers. The household survey contacts a representative sample of the US working-age civilian population and classifies each person as employed, unemployed or not in the labor force. The most commonly cited U-3 unemployment rate stipulates that an individual must have looked for work in the prior month to be counted as unemployed otherwise they are considered to be not in the labor force. The U-6 rate counts as unemployed anyone who has looked for work in the prior year.

Forecast

Non-farm payrolls are expected to gain 180,000 workers in February after January’s strong count of 304,000 with factory payrolls to add 11,000. The U-3 unemployment rate is predicted to fall 0.1% to 3.9% and average hourly earnings to rise 0.3% following January’s 0.1% gain. Annual earnings are predicted to increase to 3.3% from 3.2%.

US Economic Growth

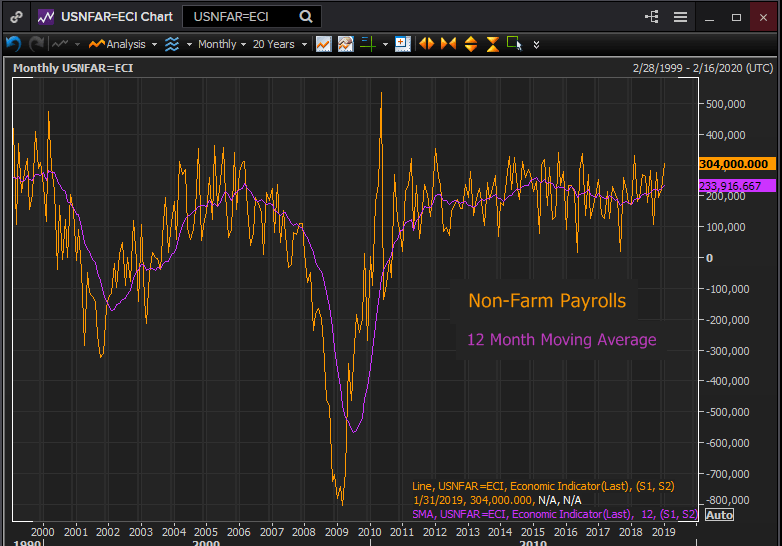

The US economy finished 2018 at 2.6% in the second estimate from the Bureau of Economic Analysis for a 3.1% quarterly average and the first year at 3% since 2004. The labor economy remains healthy. Non-farm payrolls have averaged 233,900 over the past twelve months the best since August 2015. Particularly impressive has been the sustained increase in factory payrolls as many analysts and politicians had written off the huge losses in employment as an inevitable consequence of globalization.

Reuters

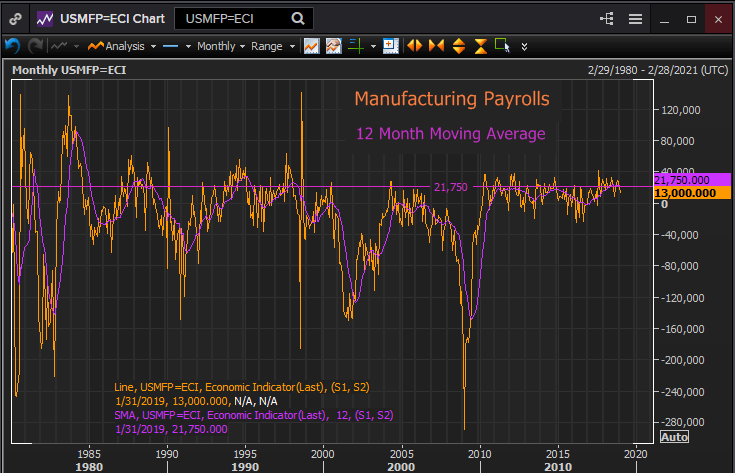

Manufacturing employment has expanded at the best rate in two decades over the past 24 months. The 12-month moving average of 21,750 in January was the highest since April 1998.

Reuters

Jobless claims are one of the most accurate early warnings of trouble in the labor market and the economy. The 4-week moving average at 229,000 has turned down from the government shutdown induced rise in mid-February and remains at the extreme lower end of its historical range.

Are US Economic concerns real?

Nonetheless a slow tide of economic worries is creeping in. The shutdown sank consumer sentiment in January. The Conference Board reading has recovered to the buoyant level of early 2018. The University of Michigan number has not. It remains below almost all the reading of the last two years at the level of November 2016, before the post-election surge.

Business sentiment was falling before the shutdown, having been at levels in the first half of 2018 not seen in 20 years.

Final retail sales statistics for the December holiday season have been delayed by the government closure and the revised numbers will be reported Monday March 11th.

The initial retail report at -1.2% for overall sales, -1.8% for sales ex-autos and -1.7% for the GDP contributory control group was widely discounted. The Census Bureau itself noted problems with the data. Private sector accounting from Amazon, the Redbook Index and MasterCard reported good or excellent spending. The January numbers are forecast to be 0.1% for sales, 0.3% for ex-autos and 0.6% for the control group. There are no forecasts for the December revisions.

The Atlanta Fed may have added to the uncertainty with its widely followed GDPNow estimate. Its first quarter annualized GDP estimate on March 4th was just 0.3% which increased to 0.5% on March 6th.

Europe, Brexit and China

Behind the domestic qualms loom quite real global issues. Europe seems headed for a recession. German quarter on quarter growth was -0.2% in the third quarter and she avoided a recession by the slimmest of margins with flat growth in fourth quarter. Italy is already in recession for the third time in a decade with -0.1% growth in the fourth quarter after a 0.2% contraction in the third. France’s average quarter on quarter growth in the first nine months of 2018 was 0.23%. Fourth quarter activity will be reported on March 28th.

Brexit continues its torturous path to conclusion, whether in the UK Parliament sometime before the March 29th exit or at some future date by delay of that deadline. Either way the prolonged wrangle and confusion has damaged growth and sentiment on both sides of the Channel.

In the US the China trade dispute while appearing to be headed for resolution keeps finding obstacles for delay. A completed deal would do much to bolster sentiment and growth in the United States and China, but until Xi Jinping and Donald Trump sit down to dinner in Mar-a-Lago, all assumptions are premature.

Finally the Organization for Economic Cooperation and Development (OECD) has reduced its global economic forecast again. Growth is 2019 has been cut to 3.3% from 3.7% in November. Europe is down to 1.0% from 1.8%.

Very little in the economic condition of the United States has changed from January to February. Predictions have deteriorated at home and abroad but they were not sanguine in January when payrolls flattened all expectations. Can the US labor market continue to deny the economic naysayers?

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.