Nine fundamentals for the week: Elections, Powell, and the build-up to Nonfarm Payrolls set the tone

- The aftermath of the French elections and Britain's probable political change are of high interest.

- Fed Chair Powell speaks in Portugal ahead of the bank's Meeting Minutes.

- A full build-up to all-important Nonfarm Payrolls is set to rock markets.

Will populists take over? In the UK, the answer is most likely no, but France poses risks to markets. Politics adds spice to an already busy kickoff of the second half of 2024. Here is the preview for this week’s major events.

1) French second-round positioning shakes the Euro

Business-friendly President Emmanuel Macron's agenda seems less at risk after the first round of voting for the French parliament. Analysts foresee greater chances of a hung parliament, which provides some calm. However, nothing is certain until the second round is held on July 7.

Before the vote, there are two factors to watch. First, how many candidates from Macron's centrist group and the wide left-leaning New Popular Front make way for each other when it comes to confronting the far-right National Rally? The deadline to withdraw is Tuesday at 16:00 GMT. More withdrawals would benefit the Euro, while stubbornness to run would risk a majority for the extreme right

Secondly, opinion polls released ahead of the vote will also rock markets.

I expect Monday's relief rally to fade away as the week progresses, making way for risk aversion that may weigh on the Euro and global stock markets. That would be a repeat of the price action seen ahead of the first round. Any headline matters.

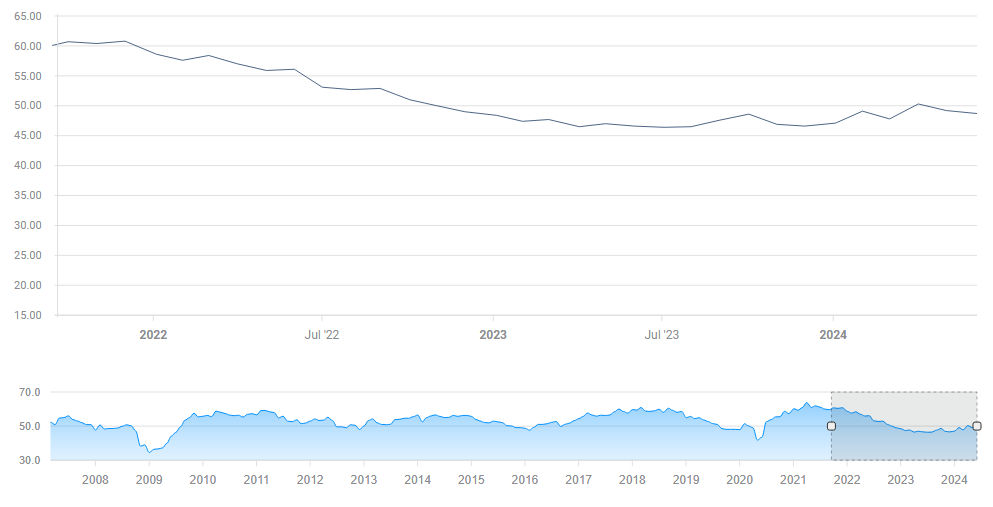

2) ISM Manufacturing PMI to provide first taste of market mood this week

Monday, 14:00 GMT. The first notable figure this week is set to show a slightly more moderate contraction in the US manufacturing sector – a score of 49.1 vs. 48.7 points the month before, still below the 50-point threshold. Any figure below 50 represents a squeeze.

ISM Manufacturing PMI. Source: FXStreet

The Prices Paid component is also of interest, as it reflects inflation expectations in the industrial sector. A small decline to 55.9 from 57 is projected, a development that would add to hopes of an early interest rate by the Federal Reserve (Fed).

In general, the softer the figures, the better for Gold and stocks, the worse for the US Dollar – all due to interest rate expectations.

3) Fed Chair Powell's inflation comments are key in Sintra

Tuesday, 14:00. Hot on Powell's heels, the US releases the JOLTs Job Openings report for May. While the data lags the Nonfarm Payrolls, the Fed watches this report closely. Job openings have been falling gradually in recent months, painting a picture of a "soft landing."

Surrounded by fellow central bankers – the event is hosted by the European Central Bank (ECB) – Powell may feel more free to express himself in all matters of monetary policy. Investors will be eager to hear about intentions to slash rates, as well as employment.

I expect him to sound somewhat more dovish, encouraging markets.

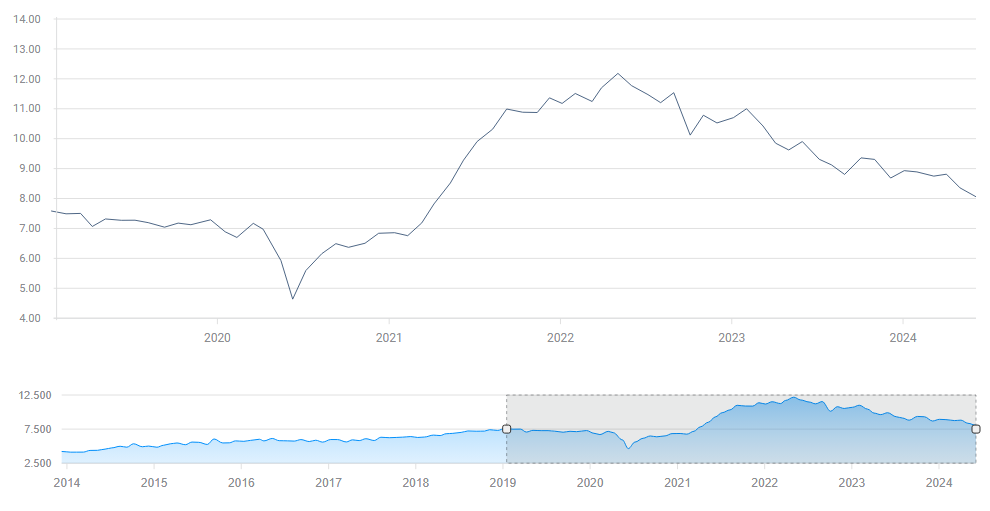

4) JOLTs to show more job cooling, eyed by the Fed

Tuesday, 14:00. Hot on Powell's heels, the US releases the JOLTs job openings report for May. While the data lags the Nonfarm Payrolls, the Fed watches this report closely. Job openings have been falling gradually in recent months, painting a picture of a "soft landing."

JOLTs still above pre-pandemic levels:

JOLTs job openings. Source: FXStreet

Should JOLTs rise, investors would fear rate cuts would have to further wait and the US Dollar would rise. A sharp drop in openings would also be beneficial for the Greenback, which would rise in response to safe-haven flows. Another moderate decline to 7.85 million, as the economic calendar shows, would weigh on the Greenback and buoy risk assets.

5) ADP jobs set to create a contrarian opportunity

Wednesday, 12:15 GMT. America's largest payroll provider rocks markets with its private-sector jobs report. While the data is not necessarily correlated with Friday's official Nonfarm Payrolls, it triggers knee-jerk reactions from markets.

However, unless the data differs wildly from expectations, these initial moves are swiftly reversed – creating a potential opportunity to go against the first reaction. It is essential to note that there are additional figures released that day, so ADP's report has tough competition.

Economists expect an increase of 156,000 in June from 152,000 reported in May. To have a sustained impact, a sub-100K rise or a figure above 220K would need to be seen.

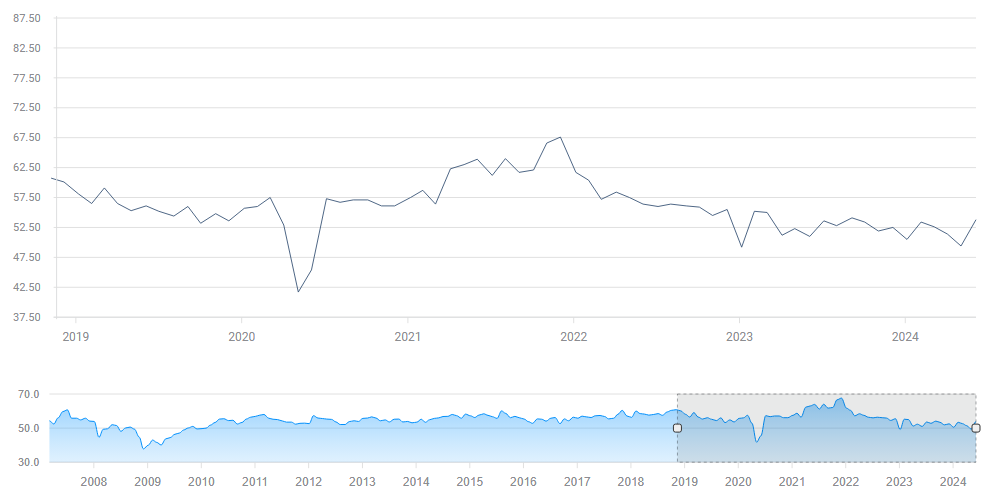

6) ISM Services PMI set to have an outside impact due to the holiday

Wednesday, 14:00 GMT. Most Americans work in the services sector, and this forward-looking snapshot is a good gauge of the broader economy. The ISM Services PMI hit 53.8 points in May, indicating moderate growth. A drop to 52.5 is on the cards for June.

ISM Services PMI. Source: FXStreet

Like with other releases, the sweet spot for markets is in the middle – ongoing moderate growth that would allow for rate cuts yet avoid a recession. A drop below 50 would trigger concerns of a downturn, while a renewed acceleration would push rate cuts off the table for longer.

I expect a slightly lower figure, which would satisfy the market.

The release might have an outsized impact due to the 4th of July holiday on the following day.

7) FOMC Minutes may cause another contrarian opportunity

Wednesday, 18:00 GMT. Will markets watch out for a document that is officially outdated just before the fireworks? I expect some US traders to be around and move markets – but cause a short-lived reaction.

These Meeting Minutes refer to the mid-June meeting in which the Fed left rates unchanged and projected only one rate cut for 2024. That "dot plot" reflecting fewer rate cuts than investors desired weighed on markets.

Officials at the Fed revise the minutes until the last minute, aiming to convey a message to markets. With stocks rising and bonds pricing two cuts, a more hawkish tone is likely from the minutes. Yet, as mentioned, I expect only a short-lived reaction.

8) UK elections set to confirm big majority for now-centrist Labour

Thursday, results are due early on Friday. The polls have been showing a clear verdict for long months – the public is angry with the ruling Conservatives – and do not trust them with the economy.

While there is no enthusiasm for Labour and its not-too-charismatic leader Keir Starmer, there is good chance the opposition sweeps into power.

For a change, markets are happy to see the leftist party in government. Under Starmer, it has taken a more business-friendly approach, emphasizing the need to generate growth.

A clear majority for Labour would please markets but might also cause a "buy the rumor, sell the fact" effect. Investors have been ready for this change. A lack of a big majority for Starmer would cause the Pound to tumble and also send global stocks down – but the prospects are extremely low.

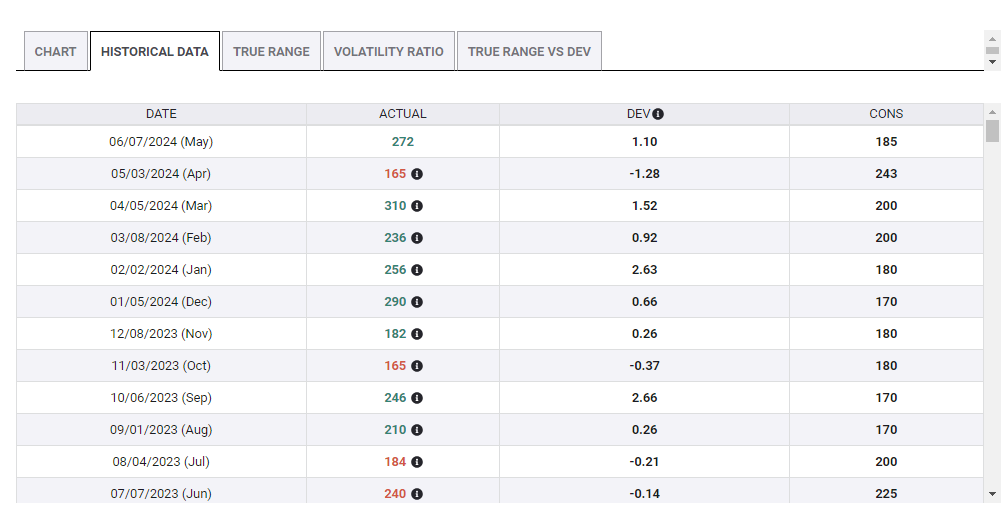

9) Nonfarm Payrolls set to show cooler job gains

Friday, 12:30 GMT. Is the job market cooling down? No, according to the headline, nonfarm payrolls jumped by 272,000 in May, which was substantially above estimates. A more moderate increase of 195,000 is expected for June.

Most NFP releases exceeded expectations:

Nonfarm Payrolls. Source: FXStreet

On the other hand, the unemployment rate – derived from a parallel survey – rose to 4% in May, and is expected to stay at these levels.

Another factor to watch is wages. Average Hourly Earnings are projected to have risen by 0.3% in June, a cooler pace than the 0.4% recorded in May.

There is no single figure that stands out, leaving room for confusion and whipsaws in response to Nonfarm Payrolls. In general, the initial reaction is driven by headline NFP. Wages come second, and the unemployment rate third.

A moderate cooling of the labor market is perfect for stocks, good for Gold, and downbeat for the US Dollar. Extremes benefit only the Greenback.

Final Thoughts

It is rare for me to highlight nine events in one week – but this is undoubtedly a busy one. That means some movements may be ephemeral, and others exaggerated. Trade with care.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.