New tax rate or not, who would want to throw foreign direct investment into the US?

Outlook:

The data this morning is retail sales, forecast up 0.4% after three months of negatives, expected to be led by autos. Note that sagging retail sales contradict fluffy consumer confidence readings. Maybe the household tax cuts will start kicking in this time.

We get a lot of interesting data this week, including the ZEW tomorrow, but we wonder what the IMF and World Bank will come up with at the spring meetings that start tomorrow. We almost always get some juicy comments from the sidelines and we also get official statements containing forecasts. No-body pays a lot of attention to them at the time unless they contain dire predictions... which they may well contain this time.

The Big Bank commentariat is divided about the outlook, according to an article in Bloomberg. Gold-man and Morgan Stanley see moderation in critical variables, but no crash, while JP Morgan, HSBC, and Unicredit all see the global expansion on track to continue. Bank of America ML says "It's still a synchronized improvement, though we may have hit the maximum pace. The U.S. will move into the lead because of the big fiscal stimulus. Growth will be a little softer in Europe and Japan." Nomura says the downside risks to growth are overstated. Barclays writes that uncertainty about the US-China trade war leads to the advice to start shedding risk assets. "But sentiment is still at historically healthy levels, U.S. earnings are strong, and China growth has accelerated, keeping the global expan-sion intact in the second quarter."

Deutsche Bank is not optimistic. "Growth is slowing from a relatively high level. We're worrying much more about overheating than a slowdown. The big tailwind for global growth will continue to be the fiscal expansion in the U.S." PIMCO says "It's been clear that growth has peaked and is no longer accelerating. The question is how sustainable the expansion now is. In the US, we still see fiscal stimu-lus coming in and I would expect there to be a re-acceleration. We are beginning to see the end of this economic expansion, but it's the beginning of the end not the end."

Citibank is the most worried. "Recent growth and inflation data seem to have undershot expectations. Recent developments have sharpened our risk outlook. We continue to see small upside risks to our 2018 growth, inflation, and monetary policy forecasts; but downside risks have risen. This is largely the result of growing geopolitical risk, and the increasing importance of the weak dollar to global (and especially emerging market) growth."

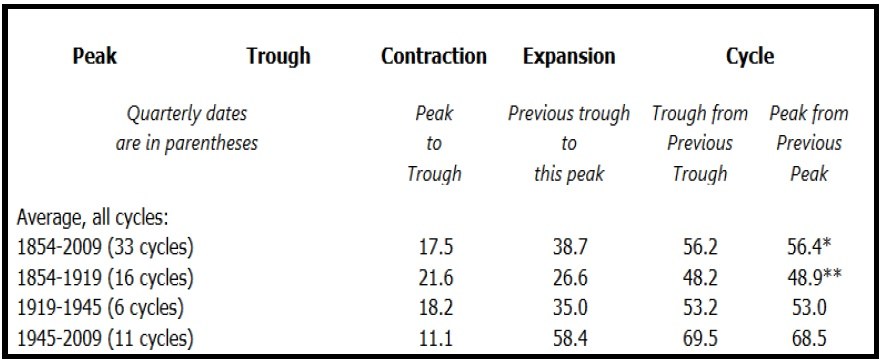

Putting the various views together and shaking vigorously, what comes out is the suspicion (based on data) that the growth peak has passed and deceleration lies ahead. More importantly, downside risks are multiplying. The self-appointed expert on the business cycle is the NBER, which offers more data than any sane person could possible want on peak-to-trough (and peak-to-peak, etc.) than any sane person could want (http://www.nber.org/cycles.html). A summary table shows trough to peak at 58.4 months. The NBER also dates the current expansion starting in June 2009. So, if averages can be applied, we should have expected the expansion starting then to have persisted by 4.8 years, or about 2014. In a nutshell, we are overdue for a trough. Many others have pointed out this anomaly—the "longest expansion in postwar history," etc. but while we may like to poke fun at the self-important NBER, data must be respected. A slowdown to recessionary conditions is, historically, inevitable.

It's a little different this time because we have the first meaningful US tax reform in three generations. But tigers do not change their stripes. Companies will continue to abuse loopholes to pay zero tax and to reward management and shareholders with the largesse from repatriated cash at the new low rate, exactly as they did in 2004 under Bush's "job creation" repatriation tax cut. What, precisely, is going to jump up and drive a new expansion? We already invented the railroad and the lightbulb. New technolo-gy can sometimes postpone recessions, to be sure, but somehow we find Alexa and self-driving cars less than compelling.

Besides, we have all too many reasons to fear the worst. Top of the list is the US-China trade war. Trump seems to have backed down for the moment, but don't buy into it. He is not giving up. Some folks do not like the debt-to-GDP ratio rising over 100%. Everyone who counts has read Reinhart and Rogoff. Such high debt ratios are a surefire indicator of doom. We also have the prospect of some kind of Middle East war, again despite Trump's promise to get out of and stay out of "stupid" wars. Trump's anti-immigration stance can easily bleed over into capital controls, something he already suggested in the form of prohibiting some Chinese investments. The US tends not to freeze or expropriate foreign assets except in time of war, but we were one of the cubicle worker bees in the Iran asset freeze, the point being it has happened in our lifetime and is a lot easier to do today. New tax rate or not, who would want to throw foreign direct investment into the US? We have zero indication that this is hap-pening.... Yet.

Some astute observers think it's time to sell in May and go away. Wall Street in Advance Lynne writes ".... if you're still long, be looking for levels to get out. The Trump honeymoon is dead, and even a great earnings season won't be sufficient to drive stocks up." The older we get, the less we know about stock market behavior, but one thing we do know—it's full of a bunch of hysteria-prone herd follow-ers. Recall the narrative in February about higher hourly wages about to push inflation to the moon. It was a dumb story, easily refuted (weekly wages fell), but equity market volatility jumped to the moon. It can do it again.

What does this have to do with the dollar? First and foremost, if the idea of recession becomes a more dominant theme, the 10-year yield is not going to break that famous 3% benchmark. If Europe is also flailing so that yields stagnate, normally we would say the differential staying the same would be dollar -neutral. But the driving force these days is not relative risk-reward, it's risk-on/risk-off. With Trump generating so much risk, risk has to rise again. Maybe Trump is inventing a whole new cycle of risk-on/risk-off, imagining it's his negotiating stance. So, again we arrive at the deduction that the dollar hangs on to gains and makes some more. Of course, a stronger dollar trajectory is bad for the trade balance.

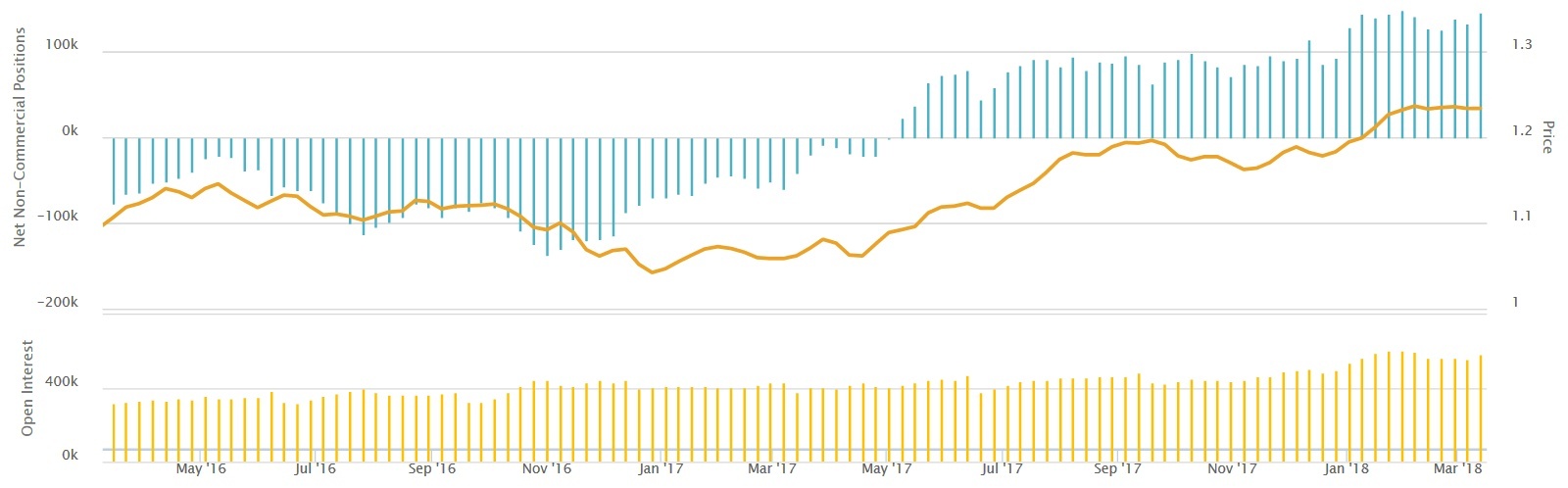

It's not necessarily bad for capital flow, not yet. We get the TIC report this afternoon, which will give everyone something to chew on. In the meanwhile, consider that the FX market doesn't see the world entirely in risk-on/risk-off terms. See the Commitments of Traders report from Oanda. Euro longs are at a historic 5-year high as of the last report (Friday for the Tuesday before). The chart is a 2-year for-mat to show the shift in sentiment better. We must be ahead of the curve with our forecast of a stronger dollar. It's not something we like, either, and many days is hard to swallow.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat