Navigating credit in 2025: Insights from five emerging trends

The start of the year has certainly been eventful, which has led to supply being underwhelming and spreads looking compressed. But this will be a year of yield and carry, as spreads are not looking attractive. Thus positioning will be key for alpha generation amid the challenges posed by fluctuating tariffs.

Spread compression leaves little to be excited about

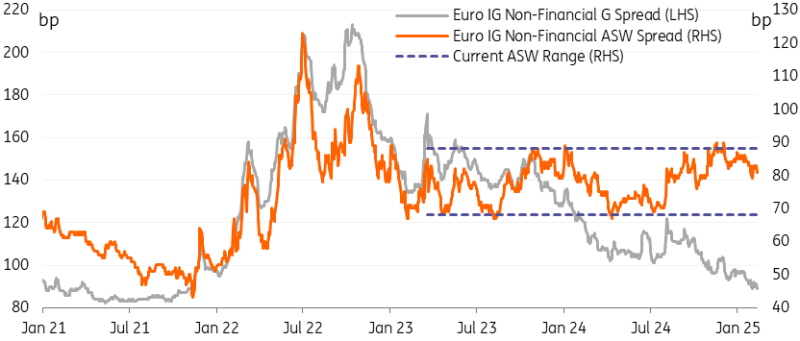

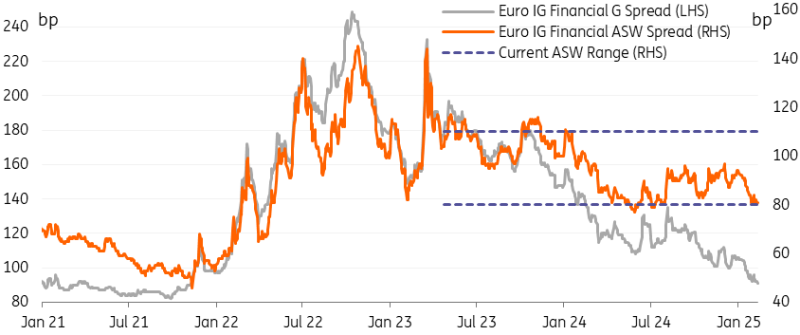

Currently, credit spread valuations can be described as challenged from various angles. Credit spreads over government bonds are particularly unfavourable, trading almost at the tight levels seen in 2021. The widening of Govie spreads and Bund/swap effects, in particular, are driving this move, which makes credit look particularly rich and unattractive against Supranational, Sovereign, and Agency bonds (SSAs).

More value appears on an asset swap spread basis for corporates, as we trade in the wider half of the range, while financials are relatively tighter at the bottom end of the range. Regardless, we don’t see much tightening potential in asset swap spreads as we expect spreads will stay elevated within the range.

Overall, spreads do not offer much value, as we expect spreads to stay elevated for 2025 due to:

-

Slightly weaker technicals,

-

A small deterioration of fundamentals,

-

Asset re-allocation,

-

Synthetic barrier formed given current SSA spreads,

-

Tariff threats.

EUR non-financial spreads

Source: ING, ICE

EUR financial spreads

Source: ING, ICE

Carry and yield will be the name of the game, not spreads

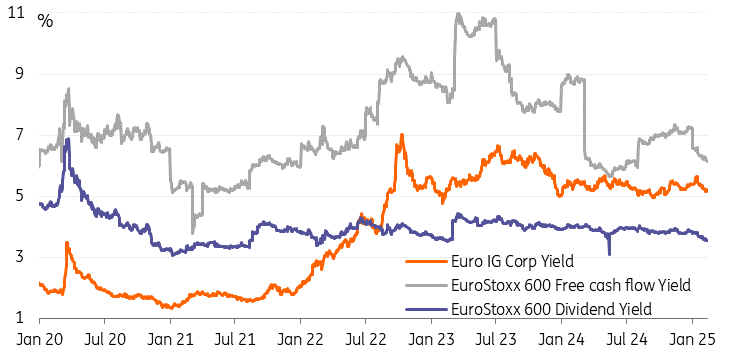

Despite the current spread levels looking relatively rich, we remain positive on the credit markets. Yield is still the name of the game, and the mantra of last year persists; ‘Carry me Home’. The carry and attractive yield will compensate for any range-bound spread widening and volatility. In addition, there are still many ‘stars in the sky’ in the form of pockets of value and opportunities for alpha generation, as it is a year of selective positioning, and issuer, sector and duration picks will be key.

Yield is still very attractive for credit

Source: ING, ICE, Refinitiv

Turbulent times amid tariff uncertainty

President Trump's tariffs have created turbulence in various sectors, with the auto industry being notably affected. The ongoing uncertainty surrounding tariffs presents potential downsides and risks in the following areas:

-

Autos: The sector remains under pressure from tariffs, with risks not yet priced in. US auto companies face initial exposure to tariffs on Mexico and Canada, while European issuers also face risks from potential European tariffs.

-

Exposure to autos: In addition, areas exposed to the auto sector, such as financing and value chains may experience challenges depending on the intensity of the tariffs.

-

Logistics and chemicals: These sectors, intertwined with global supply chains, are expected to feel the impact of tariffs and weakened demand in key markets like autos and construction.

-

Retail: Tariffs affecting US and European consumers will negatively impact retail companies.

-

Mexico exposure: Companies with substantial ties to the Mexican economy may suffer.

-

Utilities: This sector has minimal exposure to the US and is unlikely to see significant downside. However, CAPEX may be slightly affected.

Supply underwhelms initially, but picks up in February

Whilst the year started with rather underwhelming supply versus what was expected, the past couple of weeks have maintained a steadier pace compared to the usual February slowdown.

Corporate supply so far this year is now sitting at €53bn, a marginal uptick on previous years. This is despite the slower-than-expected January, impacted by fewer opportunities due to Trump's actions and central bank meetings, as well as a 40-50bp rise in rates.

A similar trend has been seen in Reverse Yankee supply, which was also underwhelming initially but picked up in February, with supply now at €10bn for corporates and €9bn for financials. And more is expected in the coming months. The low-cost element, with the very low cross-currency basis swap, makes Reverse Yankee deals attractive to issuers.

Yankee supply was underwhelming at US$8bn for corporates and US$32bn for financials, in line with previous years. Despite tight USD vs EUR spreads, European issuers did not take advantage of the tight spread differential.

Senior unsecured bond supply in banking reached nearly €57bn in 2025 year-to-date, a €9bn increase from 2024 YTD, driven by €36bn in the senior bail-in segment, offsetting a €2bn decline in senior preferred. Total senior unsecured issuance for 2025 is expected to reach €200bn, split between €90bn in senior preferred and €110bn in senior bail-in instruments.

EUR covered bond issuance was €32.5bn in 2025 YTD, behind the €48bn record in 2024 YTD but in line with full-year expectations at 21% of the total €155bn supply. This decrease is due to the end of TLTRO III refinancing and anticipated sluggish economic growth.

Dauntless demand

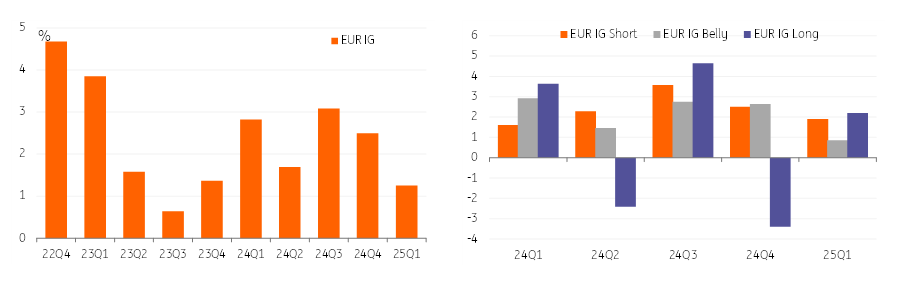

Demand continues to be very strong for credit, as attractive yields and carry help compensate for any widening pressures. Generally, the market remains skewed towards buyers. Inflows into EUR and USD credit remain steady, with approximately 1% of assets under management flowing into each on a positive, albeit gradual, trajectory. The start of the year saw a continuation of the recent trend of flows being concentrated in the shorter maturity bucket. However, in the past couple of weeks, the long end has also seen strong inflows in order to lock in yield after rates ticked up. The strong demand is also reflected in the primary market. Book oversubscriptions are still above average and very well covered, despite the very low new issue premiums on offer and often even pricing through the curve.

EUR IG fund flows per quarter

and per maturity bucket

Source: ING, EPFR

Read the original analysis: Navigating credit in 2025: Insights from five emerging trends

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.