National Bank of Poland preview: MPC to hibernate until March

Poland’s rate-setters are expected to leave interest rates unchanged this week, with the key policy rate at 5.75%. The response from the National Bank of Poland’s governor to a dovish shift in local fundamentals and the external environment remains highly uncertain. We anticipate a rate cut in the second quarter of next year, or even as early as March.

The Monetary Policy Council’s (MPC's) decision on rates will follow two days of meeting and will be announced on Wednesday afternoon. On Thursday, National Bank of Poland (NBP) Governor Adam Glapiński will provide their rationale and the broader context during a press conference. We and the market consensus assume that rates will remain unchanged, with the key policy rate still at 5.75%.

Statements from the president and the majority of Council members in recent weeks have focused mainly on the fact that discussions about rate cuts will begin in March next year. For a while now, Glapiński has communicated that the MPC brought CPI to 2.0% in March and the recent headline CPI spike was caused by regulatory decisions by the government to unfreeze energy prices. He forgot to add that core inflation has persistently stayed above 4%YoY and is very sticky.

The government has decided to extend the energy prices freeze which means the 2025 average CPI will be 1.3pp lower than the November NBP projection. The March inflation projection should present this lower CPI path and will be very important in this context as it will incorporate regulatory decisions on continued electricity freezing and the loose fiscal policy stance in 2024-25.

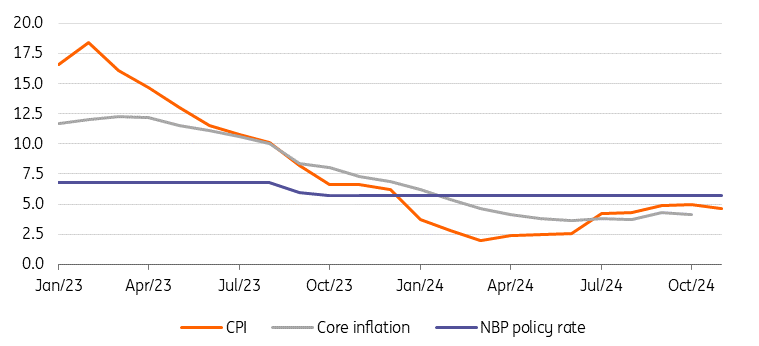

Therefore, decisions about cuts before March next year would be a big surprise for the market and a communication problem for the MPC. Although headline CPI inflation declined to 4.6%YoY in November from 5.0% in October, this was mainly due to statistical base effects on fuel prices. Inflation is well above the NBP target of 2.5% with a tolerance band of +/-1 percentage point, and is expected to trend upwards in the first quarter of 2025. As long as headline CPI is rising, the MPC should refrain from easing.

CPI and core inflation and NBP policy rate, YoY, %

Source: CSO and NBP

Governor's reaction to dovish shift in local fundamentals and external backdrop is very uncertain

Since central bank decisions are stated to be data-dependent, recent data suggests an increasing number of factors justifying rate cuts or even earlier easing.

Keeping rates unchanged means a gradual increase in the restrictiveness of NBP’s monetary policy in the coming months. Externally, expectations have grown for deeper ECB easing (to 1.75%) due to the negative impact of Trump's policies on the eurozone, in addition to rate cuts by major central banks (75bp cuts by both the Fed and ECB in the current easing cycles, and in the CEE region – including the most hawkish Czech National Bank).

Local fundamentals also call for easing i.e. a gradual decline in inflation expectations, falling corporate profitability, and a deepening in private investment activity data for the third quarter.

Also, the latest GDP structure data in the third quarter is very surprising as it showed that the dynamics of private consumption (just 0.3% YoY only) were significantly below market expectations and the NBP’s November projection (2.8% YoY). This may be only partly attributed to the catastrophic floods in South-West Poland in September.

The discussion on interest rate cuts is expected in March 2025

In this context, the most important thing for us is how the latest GDP structure data will be interpreted in the statement after the MPC meeting and during the NBP press conference. If taken as a lasting trend of lower household spending, it opens up space for a faster pace of monetary policy easing after March next year. We see the odds growing that the MPC decides to surprise markets with the first cut in March and by 50bp rather than 25bp.

On the other hand, with the consumption underperformance regarded as transitory, Governor Glapiński is likely to declare that the outlook for monetary policy is broadly unchanged, even after the extension of the electricity price freeze through the majority of 2025. In such a case, the Council is unlikely to start discussing rate cuts until it sees a sustainable reversal in the inflation trend in the March 2025 projections.

Read the original analysis: National Bank of Poland preview: MPC to hibernate until March

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.