Middle East tensions drive markets into US CPI week

- Middle East conflict remains the key market driver; headline risk to intensify as a truce nears.

- A potential ceasefire would trigger a risk-on reaction and dollar losses.

- Key US CPI data next week; upside surprises likely to support hawkish Fedspeak.

- Yen intervention on the cards; low chances of a surprise RBNZ rate hike.

Middle East conflict remains in the driver’s seat

With the US-Israel-Iran conflict completing its fifth week, investors are trying to predict the next steps. The main question is whether markets will remain driven by Middle East developments, or whether a gradual relaxation of the prevailing risk-off sentiment could allow a refocus on the real economy and AI.

Given the latest newsflow, it looks like the former will continue to prevail for now, as, unsurprisingly, US President Trump continues his back-and-forth, having failed to present a roadmap to end the conflict at his recent address. He mentioned the 2-3 week timeline again, but investors are not really taking his comments at face value.

That said, Trump almost exclusively cares about stock markets and the US economy remaining strong heading into the November midterm elections. Hence, he tends to sound more accommodative when stocks drop and US data releases fail to positively surprise, and he is obviously reading the latest opinion polls showing that the majority of responders are very concerned about gas prices.

At the same time, there are a handful of voices within the Israeli government advocating for a pause in the hostilities. Certain senior military officials have been highlighting that Israeli forces are stretched in numerous confrontations, and support for the current war against Iran is waning as Israeli cities are more vulnerable than anticipated.

Headline risk to heighten as we get closer to the finish line

Therefore, the scenario that we are nearing the end of the current conflict might have merit, with bombardments, though, from both sides getting worse ahead of the expected truce. Interestingly, there has been mixed commentary from the US side about the reopening of the Strait of Hormuz. Trump has urged his NATO allies to get their own oil through the Strait of Hormuz, or buy US oil, while VP Vance appeared ready to support a ceasefire if US demands are met including the reopening of Hormuz.

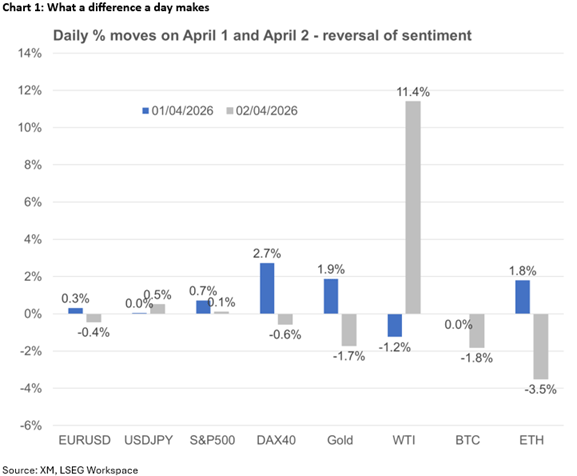

Market movements on April 1 gave us a taste of the post-Middle East conflict period. A risk-on rally would weaken the dollar, with the euro and the aussie primed for the biggest gains. Similarly, positive developments should help US equity indices climb back above their 200-day simple moving averages (SMAs), easing fears for a protracted sell-off.

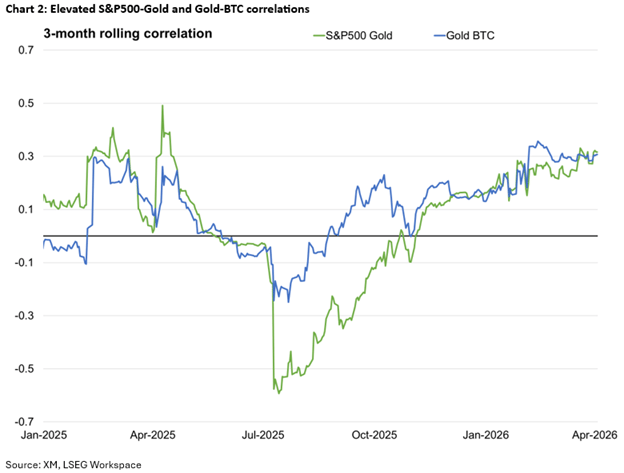

Interestingly, gold also jumped on April 1, before quickly surrendering its gains. Short-term correlations between the S&P 500 index, bitcoin and gold remain at the highest point since April 2025, with the precious metal failing to act as a safe haven asset for a plethora of reasons.

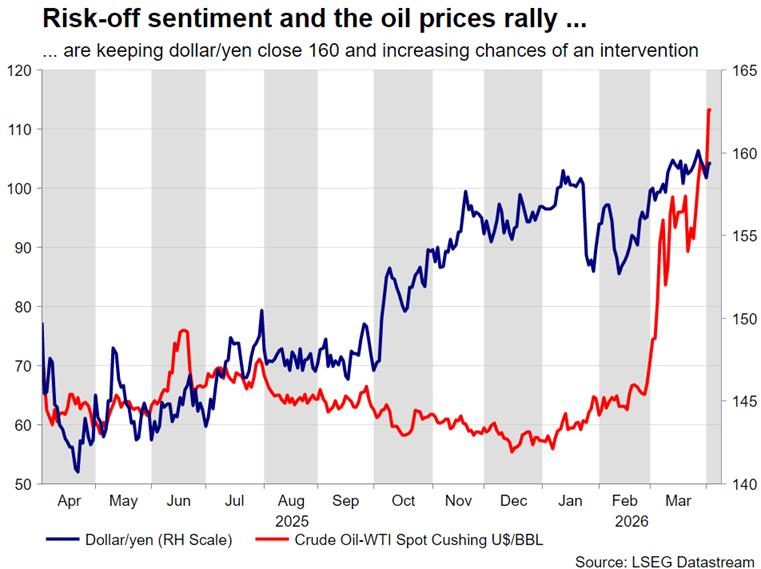

While a truce might put an abrupt end to hostilities, the return to oil supply normality could take more than a few weeks. Understandably, the risk premium embedded in oil prices will persist, with oil finding a new balance, above the previous $60-$65 range but below current elevated levels.

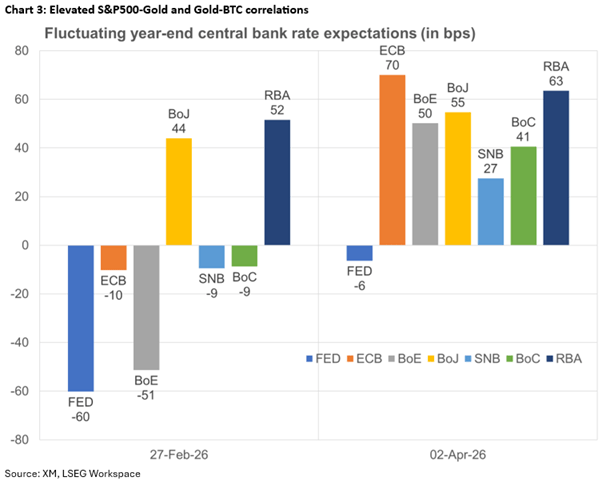

Meanwhile, a plethora of governments have announced fiscal measures to tackle the ballooning energy costs, keeping central banks on edge regarding the short-term inflation surge. The RBA has already hiked, with markets pricing in rate hikes from other major central banks. The combination of these two factors has pushed sovereign bond yields higher, increasing concerns about consumer spending. Another set of US Treasury auctions will be held next week, with the key one being Thursday’s 30-year offering as long-term yields hover near 5%.

CPI data in focus next week

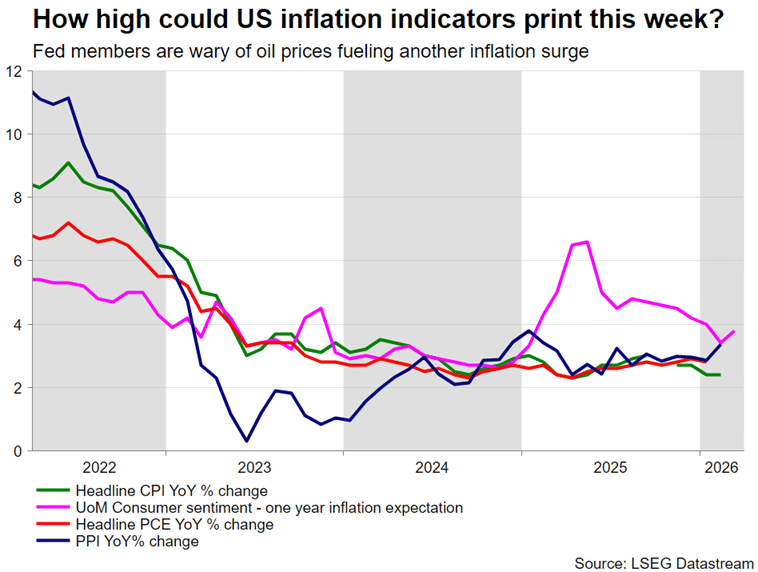

With markets digesting the US jobs data, the focus shifts mostly to the consumer sector and, more specifically, to Friday’s CPI report and the University of Michigan Consumer Sentiment survey. These data prints, along with Monday’s ISM Services PMI, February’s PCE report and Tuesday’s New York Fed one-year consumer inflation expectations, will show the initial impact of the elevated energy prices, potentially prompting an adjustment in Fed rate expectations and most likely maintaining the current hawkish Fedspeak. Notably, it will also be interesting to see if China has managed to make any progress with deflation, as the March CPI and PPI report will also be published on Friday.

Despite being mostly out-of-date, Wednesday’s minutes of the last FOMC meeting could confirm the hawkish shift seen in the dot plot. Meanwhile, US tariffs have been overshadowed by the geopolitics, but they are definitely not forgotten. Recent articles point to changes in both steel and aluminium tariffs, and pharmaceutical imports. At the same time, tariff refunds could commence during April, potentially further angering President Trump, prompting him to order the swift completion of the plentiful Section 301 investigations that could give him the right to reimpose tariffs on most key trade partners.

Additionally, private credit firms are facing heightened investor withdrawal requests, as concerns about loan quality and the actual returns are testing this lightly regulated industry. Further pressure on this industry could have implications for traditional banks, bringing back memories of the 2007-08 banking crisis.

Further Japanese data on the menu but Yen remains the main issue

Among the geopolitics mayhem and the ballooning energy prices, the Japanese government continues to focus on the ailing yen. The dollar/yen pair ebbs and flows based on Middle East newsflow, but it is evidently dangerously close to the 160 level.

Despite recent mixed data – the March Tokyo CPI eased further but both the Manufacturing PMI survey and the quarterly Tankan surprised on the upside – expectations for an April BoJ hike remain supported. Notably, Governor Ueda signaled that the BoJ is more sensitive to yen weakness than before, meaning that the chances of a BoJ rate hike in four weeks’ time are probably higher than currently perceived.

Rate expectations appear insufficient to help the yen at this stage though, and unless Ueda preannounces the April rate hike soon, Japanese authorities might be forced to act with actual intervention. Historically, BoJ prefers to intervene in low liquidity sessions such as bank holidays and weekends.

Could RBNZ surprise with a rate hike?

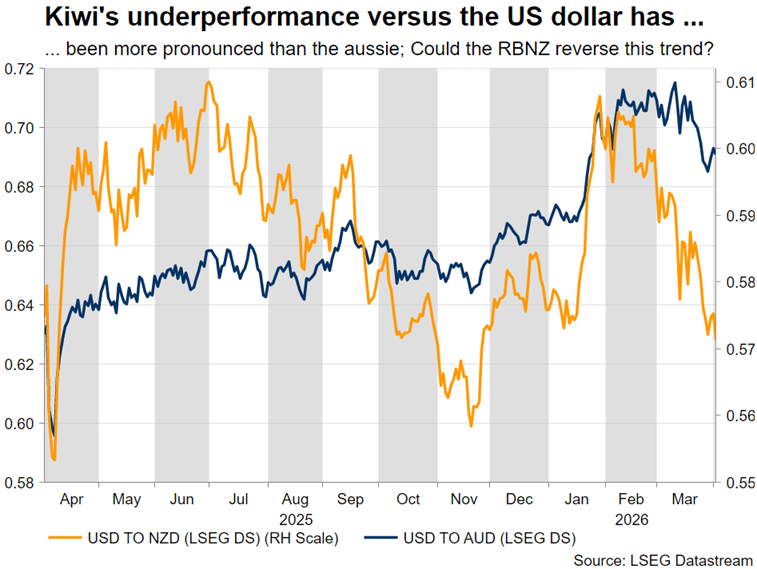

Like the aussie, the kiwi has been suffering since the start of the Middle East conflict, losing 4.2% against the US dollar in March and starting April on the back foot.

The RBNZ will meet on April 8, remaining partly out-of-sync with the other central banks. It is expected to emphasize its readiness to hike to contain any second-round inflation effects, although Governor Breman made it clear in recent comments that she is not on board with acting prematurely. Therefore, should the current Middle East newsflow persist and the RBNZ does not surprise with a rate hike, kiwi/dollar could finally overcome the support set by the 0.5690 area.

Author

Achilleas joined Trading Point in November 2022. He holds a BSc in Business Economics from Middlesex University and a MSc in Mathematical Trading and Finance from Bayes Business School, City University.