Middle East conflict puts energy efficiency back at the heart of Eurozone housing

A fragile recovery meets another shock

Despite the recent tentative US-Iran agreement, tensions in the Middle East continue to weigh on the eurozone economy. What initially appeared to be a continuation of last year’s gradual recovery at the start of 2026 has quickly become more fragile. Higher energy prices have revived inflation fears, pushing up rate hike expectations and market interest rates, and weighing on confidence. The housing market will feel the impact too.

This comes at a time when the housing market was already losing steam. In the first quarter of 2026, new mortgage lending to households in the eurozone fell by 6% quarter-on-quarter and was down 1% year-on-year. March brought a temporary rebound, with new business volumes rising by more than 10% year-on-year, but this may have reflected front-loading rather than a genuine and sustained pick-up in demand.

Looking ahead, higher financing costs and weaker purchasing power are likely to weigh more visibly on housing activity in the shorter term. House prices should continue to rise modestly, supported by structural factors, but stretched affordability is likely to cap price growth and weigh on mortgage lending.

Energy efficiency moves back up the agenda

However, the Middle East war has affected the eurozone housing market through another channel as well. Higher energy prices have pushed energy efficiency back into the spotlight. Not only as a sustainability issue, but as a question of affordability, resilience and value.

Oil accounts for around 10% of household energy consumption in the EU, but exposure differs widely: from more than a quarter in Belgium and around one-fifth in Germany to less than 1% in the Netherlands. Natural gas remains the more important energy source in most countries.

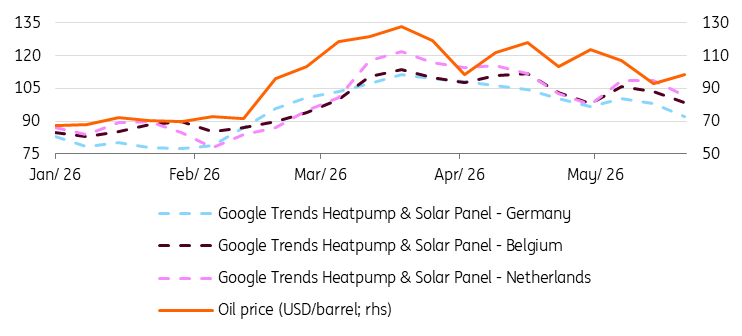

Still, while oil is not the dominant household energy source in most EU countries, the recent rise in oil prices appears to have been enough to revive broader concerns about energy costs. Since the beginning of the war, Google searches for heat pumps and solar panels have risen significantly. In Germany, interest in both has recently reached its highest level since 2023.

Oil prices and Google searches for heat pumps and solar panels

(Index ((week of the 27.02.2026 = 100)) & 3-week moving average for Google Trends).

This pattern also shows that interest fades as oil prices fall, suggesting green renovation is still driven more by cost considerations than by environmental motivation.

Our ING Consumer Survey from last September points in the same direction: among homeowners who renovated in the past three years, energy savings were the primary driver. In Germany and Belgium, more than two-thirds cited this, while in the Netherlands the share was lower but still around 50%.

The 'G-Factor' is staging a comeback

As energy efficiency moves back up the agenda, the “G-Factor”, the degree of greenness of a property, is likely to matter more for house prices again, too.

The 2022 energy crisis showed how quickly energy efficiency can become a decisive pricing factor. In Germany and the Netherlands, the green premium peaked in 2024. In Germany, homes with poor energy efficiency were priced around 40% below A+ properties at the peak, compared with 20% in 2021. Part of this gap is likely to reflect other property characteristics as well, such as build year, construction quality and renovation status, which often coincide with lower energy ratings.

In the Netherlands, by contrast, energy-efficient homes carried a 23% premium per square meter compared with the least efficient homes in 2024, up from 7% in 2021, according to property consultants Brainbay, with these estimates corrected for factors such as build year and construction quality.

Belgium shows a similar pattern. According to a study by the National Bank of Belgium, energy performance has long been an important driver of house prices. Between 2016 and 2022, price differences between energy labels were already sizeable but relatively stable. Since 2023, however, the gap has widened markedly: prices for more energy-efficient homes, those with labels A, B and C, have continued to rise, while prices for less efficient homes, those with labels E and F, have edged down.

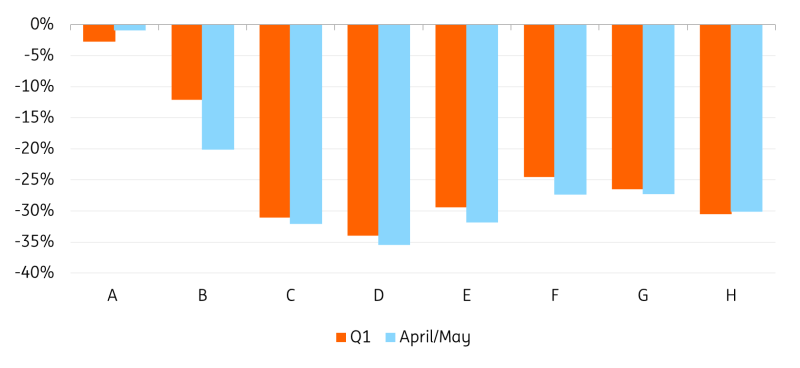

Last year, the premium remained sizeable but narrowed slightly, at least in Germany and the Netherlands. Now, it may be widening again. In Germany, discounts for energy-inefficient homes increased in April and May, averaging 26%, compared with 24% in the first quarter of 2026.

Price deviation of German residential properties by energy-efficiency class relative to A+

(in %)

A cloudier outlook, but a greener direction

For the eurozone housing market, the war in the Middle East has made an already complex outlook even harder to read. In the short term, weaker affordability, renewed inflation pressure and heightened uncertainty are likely to weigh on activity. In the longer term, structural forces, like supply shortages, demographic pressure and the green transition, look set to continue to support prices.

Regulation was already pushing the market in the same direction. Under the EU’s revised Energy Performance of Buildings Directive, member states should reduce the average primary energy use of residential building stock by at least 16% by 2030, compared with 2020 levels, with a significant share of the savings coming from the worst-performing buildings. Implementation will differ across countries, but the direction is clear: greener homes are becoming a structural feature of Europe’s housing markets.

The latest energy shock has only added urgency. As energy prices rise again and memories of the last crisis resurface, the “G-Factor” is moving back to the forefront. The short-term housing outlook has become cloudier, but the long-term direction has become clearer: energy efficiency is no longer a “nice to have”, but an increasingly decisive factor for value and affordability.

The “G-Factor” was already shaping Europe’s housing markets. Now, the latest energy shock is strengthening its role further.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.