Markets on edge amid fragile US-Iran ceasefire

Stocks struggle as ceasefire hangs by a thread

Despite a positive session in European cash markets on Monday, US equities closed largely lower, led by technology, industrials and consumer discretionary. Investors are clearly anxious and are pulling back amid elevated oil prices and rising Treasury yields.

The latest from the Middle East shows that a ‘planned’ attack on Iran was called off by President Trump. On his Truth Social platform, he stated that, following appeals from Gulf allies for additional time, the planned strike – supposedly scheduled for today – would not go ahead. A number of desks were not even aware this was in the works! The fragility of the situation was further demonstrated over the weekend after a drone strike was reported near a UAE nuclear power plant.

Markets whipsawed on what felt like every headline in yesterday's session, with oil benchmarks – WTI and Brent – erasing earlier gains after Trump's social media post. Both markets, however, continue to trade north of US$100/barrel.

In the fixed-income space, I feel that the message is clear: inflation is not going anywhere. Since the onset of the Middle East conflict, the 10-year US Treasury yield has risen by 57 bps and has recently clocked its highest level since early 2025.

UK jobs: Cracks at the edges

In the first of a large batch of UK data this week, we welcomed the March UK jobs report this morning, which showed unemployment rising to 5%, slightly above the 4.9% consensus. Headline wage growth (including bonuses) came in at 4.1%, above the prior reading of 3.8% in February, while ex-bonus pay eased to 3.4% as expected. Payrolled employees fell by a much larger-than-expected 100,000 in April – though this figure is notoriously volatile and prone to material revision.

Traders are now pricing in 55 bps of BoE rate hikes by year-end, though GBP held relatively steady versus the USD at around US$1.34. Overall, with wage growth moderately slowing and unemployment rising, this could help ease concerns about inflationary pressures for the BoE. However, these prints are largely outdated, as a lot has happened since March.

Tomorrow will see the April UK CPI inflation report land at 6:00 am GMT, with economists’ estimates suggesting price pressures to cool across both YY headline and core measures, while the MM prints are expected to accelerate.

Canadian CPI inflation data on deck

Later today, we have the April Canadian CPI inflation report hitting the airwaves at 12:30 pm GMT. Heading into this report, the YY headline number is expected to rise by 3.1% from 2.4% in March (estimate range is between 3.5% and 2.9%). In terms of the BoC’s preferred measures – CPI median and trim – analysts expect these data to come in lower, at 2.2% (from 2.3%) and 2.1% (from 2.2%), respectively. The estimated range for both indicators is narrow, between 2.1% and about 2.3%.

Something I feel that needs to be highlighted is that the current BoC rate pricing could be a little overstretched to the upside. If you look at money market expectations right now, investors have fully priced in two rate hikes this year (+55 bps), with around a 60% probability of the first in September and another in either October or December.

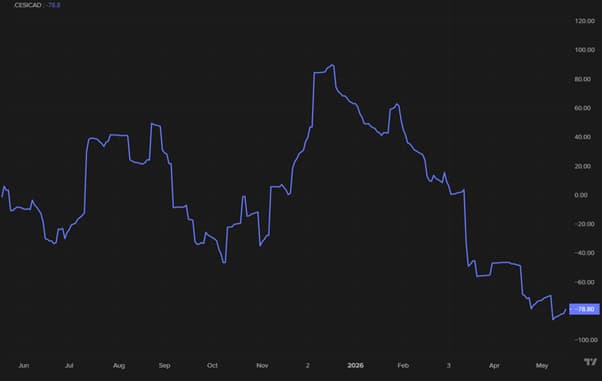

But as you can see from the first chart below – the CESI chart for Canada (LSEG) – data has been surprising to the downside for the best part of this year. Additionally, if you couple this with large-spec positioning still overstretched to the upside (second chart below), I feel this leaves the door open for a push lower in the CAD. Therefore, for me personally, given the hawkish BoC pricing and overstretched CAD positioning, a broad miss in both headline and the noted core measures would likely offer the most bang for your buck.

However, the caveat here, of course, is that if oil prices are rising, this could act as a headwind for CAD downside, given its correlation. A pair worth looking at is EUR/CAD, given the bearish positioning on EUR right now.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,