Markets chose to see the glass half full

Today we get retail sales, the usual weekly jobless claims and the Philadelphia Fed business sentiment survey. Retail sales is the biggie.

Yesterday’s CPI release was perceived as offering relief. The data is, however, contradictory and quite confusing, so how it’s interpreted depends on how the majority chose the top factors. In the end, the market chose 0.2% m/m for the core and 3.2% y/y. Core had been forecast at 0.3% so 0.2% looks good. See the clarifying chart from ING.

But as Wolf Street notes, beneath the skin, relief is not what you get. The headline CPI is up 2.9% is the worst since July. Annualize the month-over-month, and you get 4.8%, the worst since February nearly a year ago. And core is “stuck” for the 7th month at 3.1-3.3%.

The offset is the 6-month CPI core annualized, now at the lowest in 4 years and under the 2% target.

Markets chose to see the glass half full, although note that the gaggle of Fed speakers were still voicing uncertainty. The first response in the 10-year was a yield dip in the first half hour (from 4.762% at 7:10 am to 4.688% at 8:52 am and down to 4.657% by 10 am). In the end, the 10-year fell a full 15 points before recovering. As of about 7:05 am, it’s down 9 points from yesterday at the same hour.

This suggests meeting the forecast on the core m/m was a favorable outcome, and to hell with the headline and the core y/y. The WSJ headlined “Inflation Rises Again, Hitting 2.9% in December,” suggesting it didn’t bother to check the yield.

Bloomberg writes “traders resumed fully pricing in another rate cut by July—within the first hour after the release. The rally lowered yields by at least 10 basis points on notes maturing in two to 20 years. It erased most of what remained of an increase in yields since Friday, when strong December employment data sowed doubt that the Fed would cut rates at all this year.

“The benchmark 10-year note’s yield declined as much as 13 basis points to 4.66%, the lowest level since Jan. 9, the day before the jobs data. It peaked this week at nearly 4.81% on Tuesday.” One analyst says the 10year “can start to consolidate between 4.50% and 4.80% for a while.” In addition, “ … the market increased its cumulative expectations for rate cuts for 2025 to around 38 basis points."

The CME FedWatch tool shows the probability of at least one cut at the June, meeting at 44.8%, from 42.4% the day before. Adding in those who expect more than one cut by then, it’s 55.5%.

Ah, but that’s before Trump delivers his punches next week. As noted in the Tidbit below, most analysts expect a tariff staircase and not an atomic bomb. In addition, it’s not the CPI that the Fed follows, but rather the PCE, and we don’t get that until Jan 31. The entire picture can change by then.

In fact, it can change today, depending on what retail sales tell us. In Nov, sales rose 3.8% y/y after 2.9% (revised) in Oct. Forecasts are hard to come by but Trading Economics has 4%. Markets don’t usually change positions on a dime, but ever there was an opportunity for just that, retail sales might be it. For information—not useful today—retail sales rose 5.5% y/y in Dec ’23, 5.4% in Dec ’22, and a whopping 15.1% in Dec ’21.

Forecast

Retail sales are arguably more important than CPI inflation because they reveal the mood of the consumer--optimistic or gloomy? Optimistic people buy stuff and that’s a root cause of demand-driven inflation (as well as Chinese imports). If individuals started stocking up in Dec ahead of Trump tariffs, Dec retail sales could be just fine at 4%, as TR forecasts. If not more. It may be sour grapes and wishful thinking at the same time, but we do not see the inflation data yesterday as “good” and we do think retail sales can trump it, restoring the dollar upmove and making the last breakout effort another dud.

Where the breakout looks plenty real is the dollar/yen, as the market is buying into the BoJ raising rates next week (Jan 24). The dollar has fallen below the 20-day and broke the B band bottom, among other signals. The resistance line lies at about 153.18 today. Don’t laugh—it may be old-timey but is often applies as though by magic. It’s also not that far from the 50% retracement line.

Tidbit: Most economists believe tariffs will come in gradually and not all in one fell swoop. Brent Donnelly at Spectramarkets finds that most think tariffs will be delayed, targeted, and/or stepped up gradually as threats are issued. Except for China, which will get hit right away. Canada is at great risk with the probability of 1.40-1.42 pretty high.

“Anything less than shock and awe will see FX implied vols get bludgeoned.“ And yet the majority are long dollars anyway. “Most scaled or targeted tariff plans will leave the market chopping and flopping and gasping for direction.”

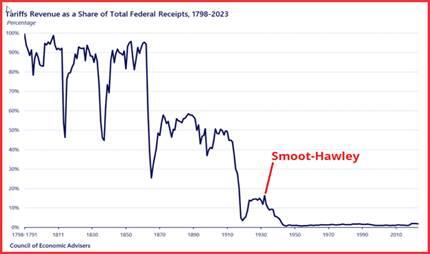

A critical point that we know already—Trump is wrong. “Most economists estimate there is no level of tariffs that could replace income tax in the United States.”

More for fun than anything else is this cute chart about revenue from tariffs going far, far back.

Political Tidbit: Masochists are watching the Senate hearings of Trump’s selection of cabinet leaders. As noted before, not a single one is qualified except maybe Bondi for Justice, and she refuses to say the department will not go after Trump foes (like the Jan 6 Committee members) while at the same time saying there will be no enemies list. Well, not until Trump hands it to her. Today is the guy up for Treasury. This is the one to watch if you have the stomach. Candidate Bessent has said he wants 3-3-3--3% growth, 3% deficit and 3 million more barrels of oil. Gee, if only it were that simple. What about using crypto for reserves, one of Trump’s more stupid ideas?

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat