Market Directions: Brexit in the Currency Market

Almost any terms on trade and sovereignty that are acceptable to the respective governments will get a positive hearing in the exchange markets. Tory Brexiteers and Brussels bureaucrats may be unhappy but as long as the current economic relationship, or something similar, continues markets will see it as a victory for the both currencies.

If we assume that is the case, a bit more difficult after the EU rejection of British terms and Prime Minister May’s denouncement of EU tactics on Friday, where might the sterling, euro and their cross end up a few weeks or months after the deal? I’ll approach the possible fallout from a ‘clean break’ in my next column.

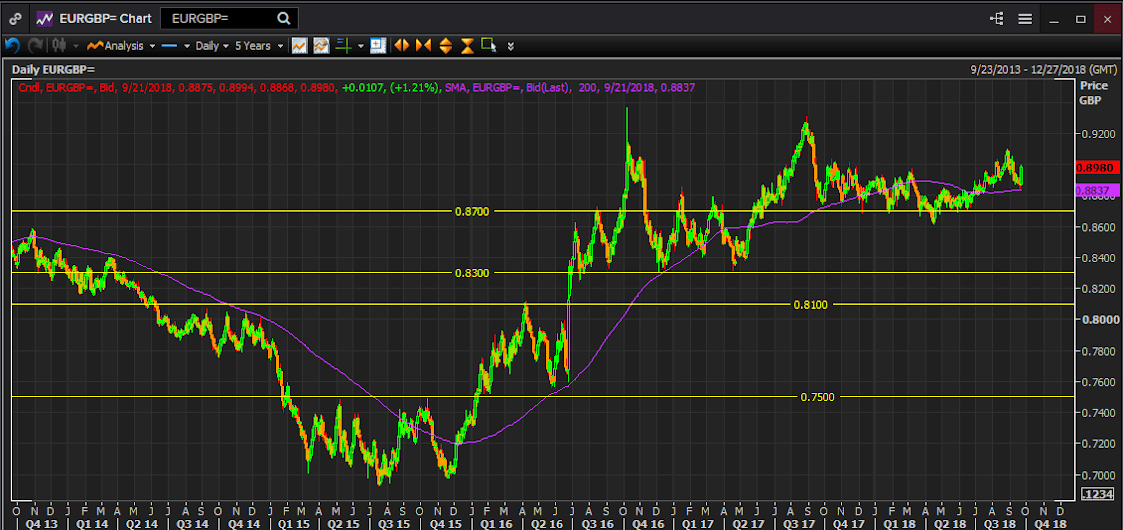

The unexpected result of the Brexit vote on June 24th 2016 profoundly altered the relation between Europe’s leading currencies. For the two years before the departure vote the euro/sterling traded below 0.8100 and below 0.7500 from February 2015 until January 2016, meaning the sterling was strong in relation to the euro. Since the vote the cross has stayed above 0.8300 with a 200 day moving average that has remained over 0.8700 since October of last year and the relationship has reversed with the euro rising in value.

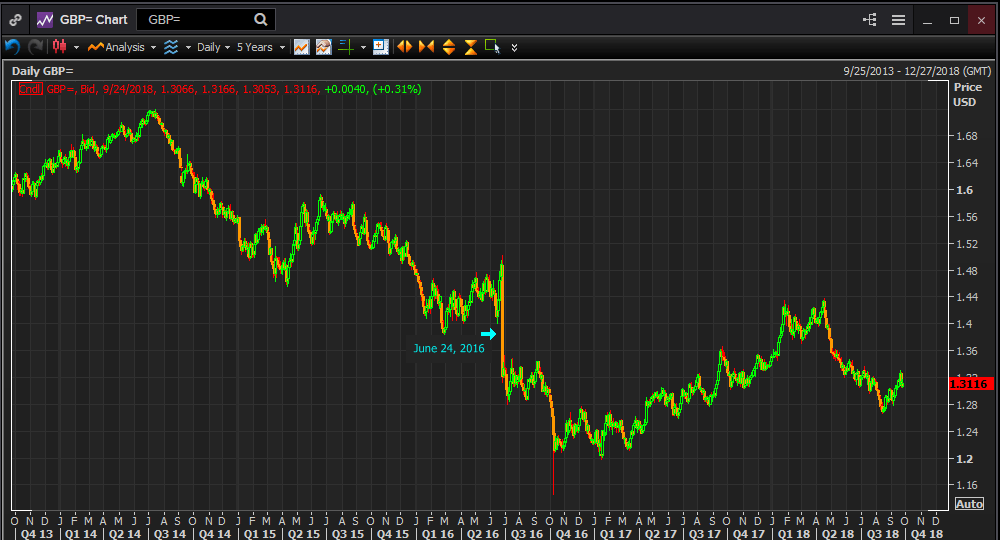

This alteration in value was due largely to the collapse in the pound subsequent to the exit vote. From an open at 1.4870 against the dollar on the day of the vote, the sterling closed at 1.3678 on the day, an 8 percent loss and over the next six months proceeded to an intra-day low of 1.1450 on October 7th and a low close of 1.2043 on January 16th, 2017, a 19 percent drop.

By the time the time the pound had begun to recover against the dollar in the second quarter of last year the euro was rising at an even faster rate. The cross followed it higher to a close of 0.9264 on August 29th, 2017, 21 percent above the 0.7654 open on June 24th.

If a separation agreement is reached, it will not be in time for the Conservative Party conference from September 30-October 3, or the European Council meeting on October 18th. That is when the EU is supposed to judge whether a deal is ready for approval at the EU summit of November 17-18.

From there the agreement would proceed to the British Parliament where Prime Minister May’s Conservatives hold 316 seats in a 650 member lower house and rely on a Northern Irish party for a majority. The European Parliament must also pass the agreement. Its process is more complex but it could hold a vote in its March 11-14 2019 plenary session just before departure date on March 29th.

If there is no deal by January 21, 2019, the European Union Withdrawal Act of 2018 gives the British government five days to make its intentions clear.

Let us propose that despite current appearances both sides make the necessary concessions to obtain an agreement by the end of the year.

Official approval by each side will not be required for a market response though if the legislature on one side or the other appears recalcitrant that will matter as the decision approaches. In the interim period approval will be assumed.

A separation agreement poses two issues for currency markets. The first is how much of the pound’s value at the point of an agreement is a residue of the original shock of the Brexit vote and the fears that Britain would fall out of the EU unregarded.

If in the run up to prospective agreement, progress has been clear and public, or secretive and leaked, then most of the adjustment will have taken place before the public consummation. This would be much as the pound was strong in the first four months of this year, fell on reversing news from April to August and then rallied again until Friday’s speech from Prime Minister Theresa May. It is what can be expected.

The second question cannot take precedence until the first is disposed, that is until there is an agreement. How has the economic, statistical and rate environment between the EMU and the UK changed since the Brexit vote? Can the relationship between the sterling and the euro simply revert to a pre-exit norm?

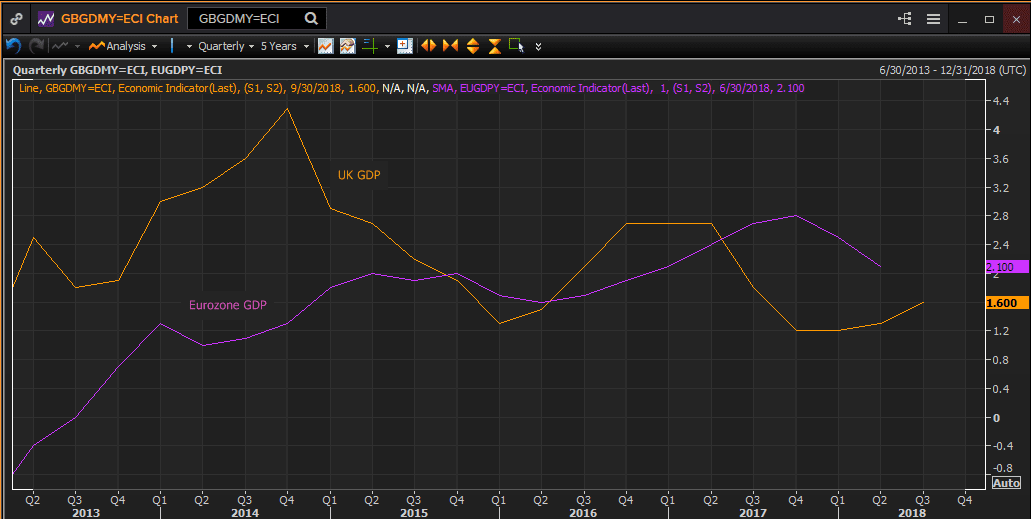

For the first year after the referendum the UK economy grew faster and generally out performed that of the Eurozone. Note that this made little difference to the cross which continued to rise sharply as the euro strengthened relative to the pound for the first six months and, though it retreated in the second half year still maintained a much higher rate than pre-Brexit.

The positions reversed in the second quarter of last year with EMU growth outpacing that of Great Britain but this also had marginal effect on the euro/sterling which traded between 0.9000 and 0.8700 for the majority of the time. Relative growth has again switched this year with the EMU rate falling from 2.8 percent to 2.1 percent and that of the UK rising from 1.2 percent to 1.6 percent. More importantly for central bank policy inflation rates have been stronger in the UK.

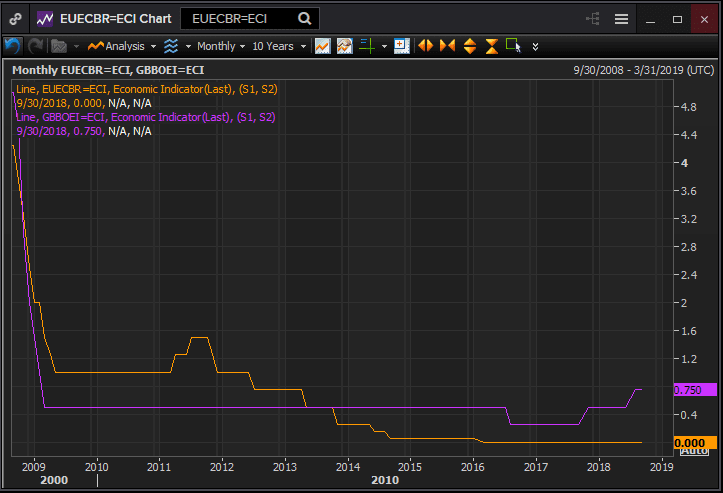

The Bank of England responded to the changing inflation environment with its first rate hike in over a decade last November, followed by a second 25 basis point increase to 0.75 percent in August. That first hike and the anticipation of further increases was one of the factors behind the rapid sterling gain in first four months of this year.

The ECB will finish its liquidity bond purchases at the end of this year. Its next policy move, at an unknown remove, will likely be a rate increase. The market anticipation that powers currency rates will return to EMU economic performance and specifically inflation. Mr. Draghi's comment in his speech to the European Parliament on Monday that there is "a relatively vigorous pick-up in underlying inflation" sent the euro close to a figure higher. In the background is the gradual and general return of central banks to a more normal rate environment.

When market focus withdraws from the complications of Brexit, inflation and the potential next policy change at the ECB should be enough to keep the euro at a new higher level against the pound. The sterling will recover but it will not return to its dominance of 2014 and 2015.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.