Market Directions: A Sterling Revival?

In the three way tug of war between the European Union, the government of Prime Minister Theresa May and the Tory hardliners that is the Brexit negotiations the only sure loser has been the British Pound.

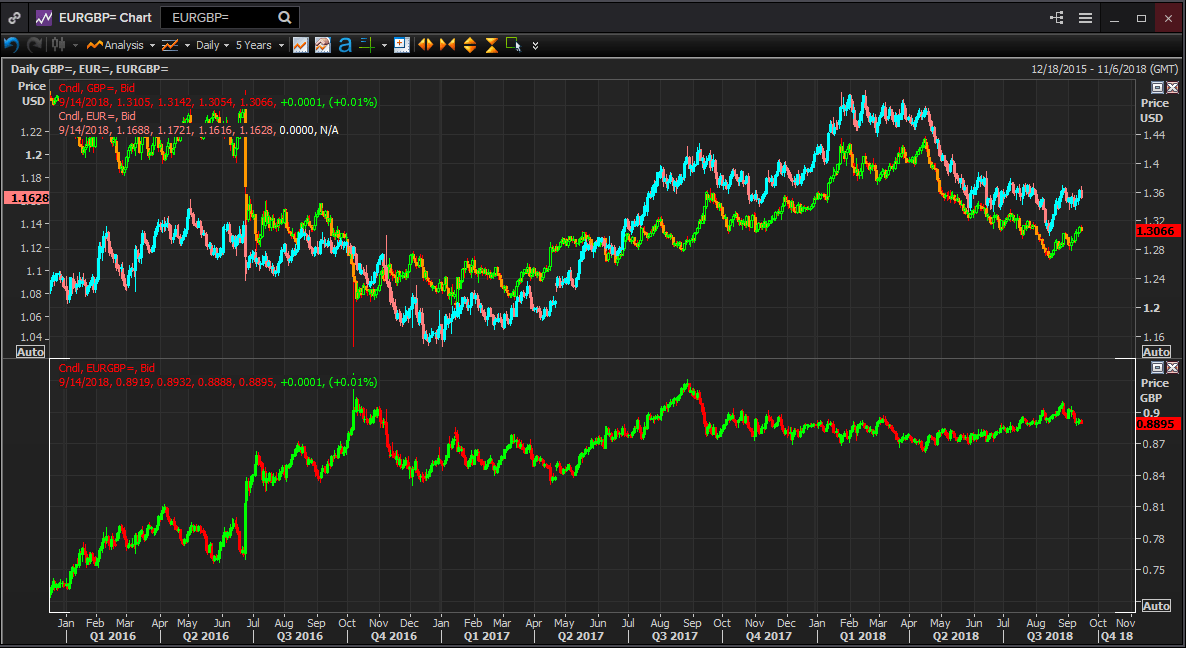

After that June 2016 vote the pound collapsed losing 16 percent against the dollar by October 7th. It reached a final 19 percent low on January 16th of the next year closing at 1.2043.

The euro pummeling was harsher, with the pound losing 18 percent of its euro value in just over three months, closing at 0.9013 on October 7th, with the final low at 0.9264 delayed until August 29th 2017.

The subsequent recovery of the pound which lasted all of 2017 and into the second quarter of this year was more pronounced against the dollar. By April of this year the sterling had regained 79 percent of its dollar loss closing at 1.4286 on April 17th. By the same date the sterling had returned to just 62 percent of its euro value. That disparity has diminished somewhat but it remains intact, to the close on Friday September 14th the sterling is down 16 percent against the euro and 12 percent versus the dollar.

The devaluation of the pound against the euro and the dollar was not predicated on any substantive economic performance but on the notion that the British economy would be seriously damaged by severing its legal and organizational connections to the European Union.

In the summer of 2016, facing the unknown ramifications of the exit vote, the logic of fear seemed reasonable, though it was probably complemented and reinforced by the anti-Brexit world view of the vast majority of market participants.

But in fact the UK economy did not decline, by many measures it equaled or surpassed the performance of the EU over the next year.

In the twelve months following the Brexit vote the British economy averaged 2.55 percent year on year growth, the EU managed just 2.03 percent. Industrial production on the continent averaged a 0.2 percent gain for four quarters starting in July 2016, in the UK the average was 0.15 percent. Unemployment, long an EU difficulty, was double that in Britain, 9.57 percent versus 4.71 percent. Retail sales measured a 0.26 percent average increase on the continent, across the channel the gain was 0.24 percent a month. Inflation averaged 1.71 percent in the UK in these twelve months and 1.07 percent in the ECB jurisdiction.

The interest rate policies of the ECB and the Bank of England reflected the diverging paths of the two economies.

In November 2017 the Bank of England raised its base rate 0.25 percent. Though it was the first increase in over eleven years, the move had been anticipated for many months and was largely priced in by the actual event. Throughout this period the ECB main rate was at zero and the bank supported the Eurozone economies with the liquidity provision of billions in euro bond purchases each month. That program continues until the end of this year.

From the open on June 24th 2016, the morning of the Brexit vote at 0.7654, the pound lost 14.5 percent against the euro over the next four quarters closing at 0.8760 on June 30, 2017. The devaluation came despite the modestly better economic performance of the U.K., the complete lack of negative effects in the U.K. and, in the latter part of the year the speculation of an incipient BOE rate hike.

Nevertheless the markets remained fixated on the potential risks of the separation, responding, often violently, to the rhetoric from the departure talks and the spectre of an abrupt non-negotiated end to the relationship.

The performance of the pound against the dollar in the period from the post-Brexit low in January 2017 to its recent peak in April of this year, a gain for the island currency of 18 percent, is equally divorced from strict economic logic.

Over that period the U.S. economy out-performed the U.K. The U.S. economy averaged 2.44 percent a quarter in annualized growth, the U.K. 2.18 percent of year on year expansion. Annual core inflation was higher in Britain, 2.38 percent to 1.87 percent. Industrial output, job creation, and wage increases all favored the Americans. Most importantly the Federal Reserve was steadily raising rates, adding 1 percent to the Fed Funds rate from December 2016 to March 2018.

In the year following the Brexit vote the sterling shed 14.5 percent of its value against the euro despite the superior performance of the British economy and for latter half of the period the anticipation of higher U.K. rates. In the 16 months from January 2017 to April 2018 the sterling rose 18 percent versus the dollar despite the advantageous performance of the American economy and a steadily tightening Federal Reserve.

With the end of the Brexit negotiations approaching, will the exaggerated fears of the anti-Brexit ‘remainers’ send the sterling plunging again? Or will the somewhat illogical rise of the pound against the dollar since last January be the model?

When the EU--U.K.separation reaches a negotiated end sometime this year or next, the sterling could well soar. It would be a fitting end to the market’s devolution Brexit fantasy.

Charts: Reuters Eikon

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.