Market Brief: a trade headline a day keeps the bears away

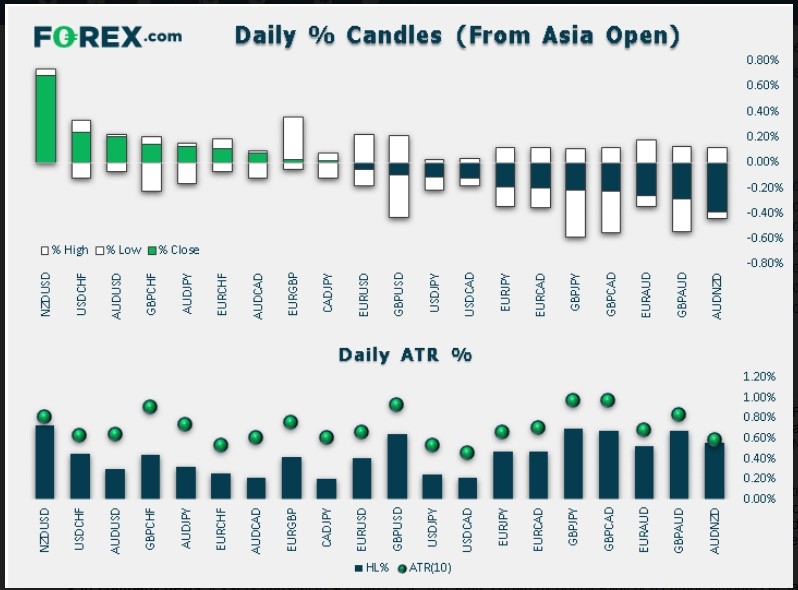

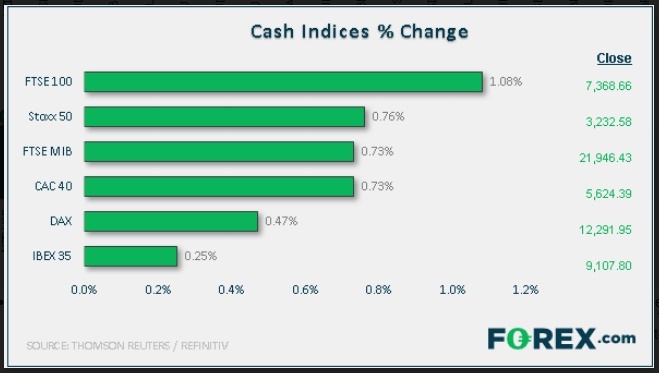

At 13:00 BST, the NZD was the strongest and GBP among the weakest, while stocks were sharply higher in Europe, led by the FTSE 100.

The Dollar Index edged further higher after posting a bullish pattern the day before as the likes of the EUR, CHF and GBP gave way. But NZD stole the show, posting the day’s biggest rise among the major currencies, in an otherwise subdued FX volatility day. The kiwi was given a shot in the arm by RBNZ Governor who downplayed the likelihood of resorting to non-conventional monetary policies (i.e. QE). Up until today, the NZD had been one of the weakest currencies after the RBNZ recently cut interest rates to a record low in order to support a flagging economy.

Stocks have risen sharply today. There’s been very little macro news so far during the European session, so trade-related headlines continued to drive the markets. Reuters reported that China and the US are still discussing details about upcoming trade talks in October, making preparations to ensure "positive progress" is made during the negotiations, according to the Chinese commerce ministry. This comes after Donald Trump tried to divert attention away from the impeachment inquiry to talks on trade by saying that a deal with China “could happen sooner than you think.” The US President also signed a partial trade deal with Japan’s Prime Minister Shinzo Abe on the sidelines of the UN General Assembly in New York.

In company news, it's very unusual to see two FTSE 100 shares down by double-digit percentage amounts at same time – especially on a day when the index itself is up a cool 1%. Yet Pearson shares fell 17% by late morning while Imperial was down about 10%, before both pared some of their losses. Tobacco group Imperial Brands was accused of 'not making a lot of sense' by broker RBC after a new sales forecast following a profit warning. And Pearson's troubled US business strikes again, hitting the outlook.

Coming up: The final US second quarter GDP estimate (13:30 BST) is expected to be left unrevised at an annualised rate of 2.0% q/q; weekly unemployment claims (13:30 BST) are expected to print 210K and pending home sales (15:00) are seen falling 1% month-over-month. Meanwhile FOMC members Bullard (15:00 BST) and Clarida (16:45) will be speaking later, but first it will be ECB’s outgoing President Mario Draghi who is due to deliver a speech (14:30 BST) in Frankfurt.

Author

Fawad Razaqzada

TradingCandles.com

Experience Fawad is an experienced analyst and economist having been involved in the financial markets since 2010 working for leading global FX, CFD and Spread Betting brokerages, most recently at FOREX.com and City Index.