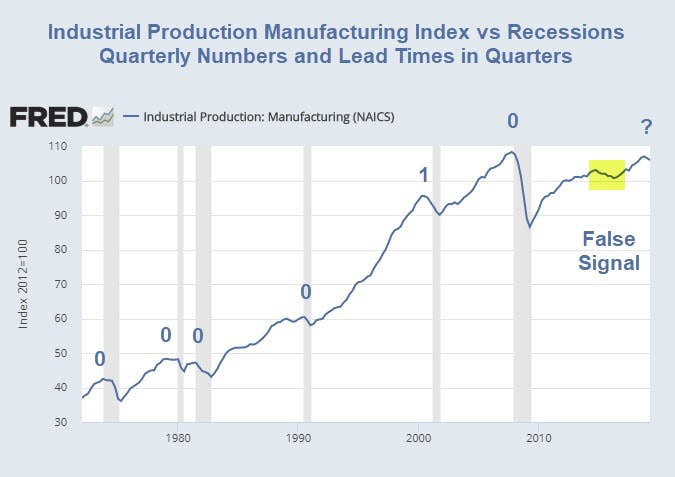

Manufacturing Recessions vs Real Recessions: How Much Lead Time Do You Expect?

Manufacturing matters more than most think. A very reliable recession indicator is flashing rapidly.

Caroline Baum, one of my favorite economic writers and author of "Just What I Said" penned an excellent column yesterday: Manufacturing isn’t the whole economy, but it’s important enough to get the Fed’s attention.

Manufacturing output contracted in both the first and second quarters of this year, according to the Federal Reserve’s report on industrial production. That was the first back-to-back decline since the soft patch in 2015 and 2016 — and one of the key factors, along with trade frictions and slowing global growth, driving the Federal Reserve to lower interest rates next week.

Manufacturing isn’t the economy, as Goldman Sachs economists pointed out in a report last week. Its share of gross domestic product has fallen to 10%, according to Goldman’s calculations.

Baum Disputes Goldman Claim

Baum disagrees with Goldman Sachs, and so do I, for even more reasons.

Here are some of Baum's reasons.

- Unlike the services sector, manufacturing tends to be cyclical. Manufacturers can choose to postpone capital investment projects when the future doesn’t look bright, but the public still needs teachers, nurses and firefighters, even in recession.

- “In real terms, growth in manufacturing has kept up with growth in the rest of the economy over the last 70 years,” according to a 2017 study by economists at the St. Louis Fed. Its “share of real GDP has been fairly constant since the 1940s, ranging from 11.3% to 13.6%.” So the often touted “shrinking share” is really a function of the change in the price level.

- Four of the 10 components in the Conference Board’s index of leading economic indicators are manufacturing-related. Ranked in order of importance, they are: average weekly hours in manufacturing; the ISM new orders index, which was added in 2012, replacing the ISM vendor deliveries index; manufacturers’ new orders for consumer goods and materials; and manufacturers’ new orders for non-defense capital goods excluding aircraft.

- Things can always change, but it seems safe to say that as manufacturing goes, so goes the nation. Judging from a century of data, it seems safe to say that what happens in manufacturing doesn’t stay in manufacturing. Instead, it has spilled over to the economy at large. So ignore the small yet significant manufacturing sector at your own peril.

GDP Illusion

In Is the US Economy Close to a Bust, Pater Tenebrarum at the Acting Man Blog points out:

One thing that we cannot stress often enough is that the manufacturing sector is far more important to the economy than its contribution to GDP would suggest. Since GDP fails to count all business spending on intermediate goods, it simply ignores the bulk of the economy’s production structure. However, this is precisely the part of the economy where the most activity actually takes place. The reality becomes clear when looking at gross output per industry: consumer spending at most amounts to 35-40% of economic activity. Manufacturing is in fact the largest sector of the economy in terms of output.

In The GDP Illusion Tenebrarum writes …

Sure enough, in GDP accounting, consumption is the largest component. However, this is (luckily) far from the economic reality. Naturally, it is not possible to consume oneself to prosperity. The ability to consume more is the result of growing prosperity, not its cause. But this is the kind of deranged economic reasoning that is par for the course for today: let’s put the cart before the horse!

In addition to what Tenebrarum states, please note that government transfer payments including Medicaid, Medicare, disability payments, and SNAP (previously called food stamps), all contribute to GDP.

Nothing is “produced” by those transfer payments. They are not even funded. As a result, national debt rises every year. And that debt adds to GDP.

Manufacturing's Share of GDP is Hugely Underestimated

Thus, in addition to Baum's excellent comments on the the cyclical nature of manufacturing, manufacturing's share of GDP as attributed by economists is simply wrong.

For further discussion, please see Debunking the Myth “Consumer Spending is 67% of GDP”.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc