Lessons from Britain for Japanese Government Debt1

Executive Summary

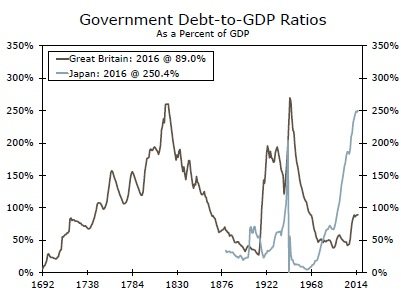

The debt-to-GDP ratio of the British government ballooned to 250 percent, where the Japanese ratio currently stands, twice in the past two centuries. In neither episode did the British government default nor did it actually reduce its outstanding stock of debt. Rather, the government relied on solid nominal GDP growth to de-lever. Raising nominal GDP growth seems straightforward in theory but can be difficult to achieve in practice, especially for a country like Japan which faces a number of constraints. Not only will the Japanese population contract in coming decades, but it is not readily apparent how stronger productivity growth is to be achieved.

Raising inflation would help to boost nominal GDP growth, but the Bank of Japan (BoJ) has had little success doing so over the past two decades. That said, the BoJ is not likely to sell down its massive holding of Japanese government bonds (JGBs) anytime soon. Therefore, JGB yields likely will remain depressed for some time.

Great Britain to Japan: "Been There, Done That"

Thirty years ago the government debt-to-GDP ratio in Japan was only 70 percent. Over the next 30 years, however, the combination of stagnant nominal GDP growth and gaping budget deficit caused the ratio to mushroom to 250 percent (Figure 1). With nearly ¥1300 trillion (almost $12 trillion) worth of debt outstanding, many observers are left wondering how the Japanese government will ever manage to pay it all back.

Figure 1 also makes clear that the current Japanese predicament is not without precedent. Specifically, the British government debt-to-GDP ratio reached similar levels twice in the past 200 years. The ratio in Great Britain stood at roughly 120 percent in the early 1790s, but subsequently climbed to 260 percent over the next 30 years during the Napoleonic Wars. The second episode was associated with another long and costly war. Between 1940 and 1946 the government debt-to-GDP ratio skyrocketed from 120 percent to 270 percent. Yet in both episodes the ratio eventually subsided without default by the British government. Are there lessons to be gleaned from the British experience that are applicable to Japan today?

Lessons from 200 Years of British Economic History

The first lesson is that reducing the debt-to-GDP ratio generally does not happen quickly. As noted above, Great Britain's debt-to-GDP ratio peaked at 260 percent in 1820, but it took about 35 years for it to recede to its pre-war level. The ratio fell more quickly following the Second World War, but it still took until 1960 for it to return to its pre-war level. In other words, investors should not expect the Japanese debt-to-GDP ratio to return to its pre-1990 level anytime soon.

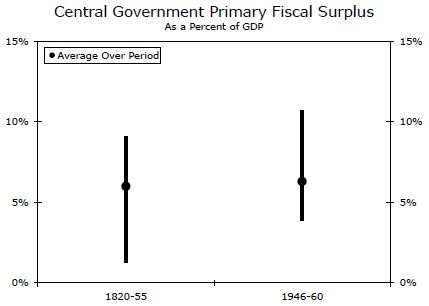

The second lesson is that fiscal restraint played a role in the de-levering process in both episodes, but it was not the primary means by which the reductions in the debt-to-GDP ratio were achieved. As shown in Figure 2, the primary budget surplus ranged between roughly 1 percent of GDP to 9 percent of GDP between 1820, when the debt-to-GDP ratio peaked, to 1855, when the ratio returned to its pre-war level.2 The primary budget surplus averaged 6 percent of GDP, which is a fairly high surplus, over that 35-year period. During the 1946-1960 de-levering episode, the primary surplus ranged from 4 percent to 10 percent with an average value of 6 percent again.

Yet despite a fair amount of fiscal restraint, the British government did not bring down the absolute amount of debt by any meaningful amount when it went through its two long periods of de-levering. The par value of British government debt totaled £838 million in 1820 when the debt-to-GDP ratio peaked, and it was more or less unchanged 35 years later. In the aftermath of World War II, government debt actually rose from about £25 billion in 1946 to £28 billion in 1960. The lesson from these two de-levering episodes in Great Britain is that the Japanese government does not really need to "pay back" its debt in order to de-lever. That is, the Japanese government does not actually need to reduce its ¥1300 trillion worth of outstanding debt to delever. It just needs to make interest payments and roll over its debt as it matures.

Shrinking the Ratio by Raising the Denominator

As noted above, the de-levering episodes that occurred in Great Britain between 1820 and 1855 and again between 1946 and 1960 were not achieved by a reduction in the numerator of the debtto- GDP ratio. Rather, the reductions were achieved primarily by increases in the denominator. That is, Great Britain grew its way out of its debt problems after the Napoleonic Wars and again after World War II.

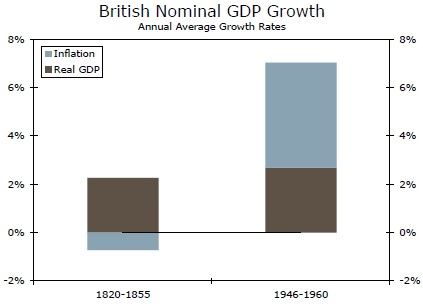

Between 1820 and 1855 real GDP growth in Great Britain averaged 2.3 percent per annum (Figure 3). Because the price level fell at an average rate of 0.7 percent per year during this period, nominal GDP growth averaged only 1.6 percent per annum during this 35-year period. Nevertheless, nominal GDP rose 70 percent between 1820 and 1855, which was enough to bring about a meaningful reduction in the government's debt-to-GDP ratio. The de-levering that occurred after the Second World War occurred more quickly because nominal GDP growth averaged 7 percent per annum between 1946 and 1960. The annual average real GDP growth rate of 2.7 percent in the second de-levering period was a bit stronger than the rate that was achieved during the first period, but it was the inflationary record that really distinguishes the two periods. As previously noted, the price level actually fell between 1820 and 1855. Prices in the United Kingdom rose at an average annual rate of 4.4 percent between 1946 and 1960.

De-levering by the Japanese Government Is Possible, But...

So the task facing Japan is actually quite simple, at least in theory. All Japan needs to do is raise its nominal GDP growth rate to grow its way out of its current debt problem. In practice, however, the task is much more difficult. Nominal GDP in Japan is essentially no higher today than it was in 1997. If the task were so easy, Japanese authorities probably would have figured out how to raise nominal GDP growth a long time ago.

First, there is the issue of real GDP growth. Real GDP in Great Britain grew more than 2 percent per annum during its two de-levering episodes due, at least in part, to positive population growth, which is one of the ingredients of potential GDP growth.3 During its de-levering period in the 19th century the British population grew in excess of 1 percent per annum. Population growth slowed in the 20th century, but the number of U.K. residents grew about 0.5 percent per year between 1946 and 1960.

will continue to decline between now and the end of the century. Despite fewer workers, Japan could still achieve strong real GDP growth if productivity growth were robust. However, Japanese productivity has essentially been stagnant since the global financial crisis, and it is not apparent what will lift it meaningfully in the foreseeable future.

The second issue for Japan is inflation, or rather the lack thereof in recent years. Elevated inflation pushed up British nominal GDP growth in the years following World War II, which contributed to the marked decline in the debt-to-GDP ratio by 1960. In contrast, Japan has been dealing with mild deflation on and off for the past 20 years (Figure 5). Indeed, the consumer price index in Japan has been essentially flat on balance since 1998.

Implications for Japanese Economic Policy

So the overall lesson from two centuries of British economic history is that the Japanese government can de-lever over the next few decades, but it needs some changes in economic policy in order to do so. First, the Japanese government has incurred large primary deficits for the past two decades (Figure 6), which arguably need to be reined in, at least in a non-abrupt fashion. As noted above, the British government ran primary surpluses, which helped to restrain the rise in the absolute amount of debt outstanding, during its two de-levering episodes. Fiscal restraint in Japan would help to reduce the government debt-to-GDP ratio in that country as well. That said, the Japanese government probably would want to phase in fiscal restraint gradually rather than in an abrupt manner. The government raised the consumption tax in 1997, which contributed to the subsequent Japanese recession in 1998. The government raised the consumption tax again in early 2014, and the economy experienced a mild recession later that year. Fiscal consolidation, if implemented too quickly, can be counterproductive. That is, severe austerity can throw an economy into recession, thereby leading to higher deficits and debt.

Second, Japan desperately needs stronger growth in nominal GDP, which can occur via more robust growth in real GDP and/or higher inflation. The demographics in Japan are more or less set for the foreseeable future, but higher labor force participation among females could lead to stronger growth in Japanese real GDP while the transition to a higher participation rate was taking place.4 Acceleration in productivity would also help to lift real GDP growth in Japan. In that regard, some of the proposed structural reforms that originally were part of Abenomics, but which subsequently have not advanced very far, have an important role to play in raising real GDP growth. Stronger real GDP growth in Japan is certainly possible, but it may take some painful adjustments in the Japanese economy to bring it about.

Japan also needs higher inflation to push up its nominal GDP growth rate. Despite a staggering increase in the size of its balance sheet in recent years (Figure 7), the BoJ has not had much success engineering higher inflation. Until inflation starts to rise on a clearly sustainable basis, the BoJ could very well continue to expand the size of its balance sheet. At a minimum, it is not likely to shrink its balance sheet anytime soon. At present, the BoJ holds about 40 percent of all JGBs outstanding. This massive amount of JGB holdings by the BoJ undoubtedly has contributed to the marked decline in their yields in recent yields. With the BoJ not likely to reduce the size of its balance sheet anytime soon, JGB yields likely will remain depressed for the foreseeable future. In other words, Japanese authorities are likely to impose a form of "financial repression" in its de-levering process in coming years.5

Conclusion

The debt-to-GDP ratio of the Japanese government currently stands at 250 percent, the highest ratio among advanced economies at present. The British government has experienced comparable ratios of debt twice during the past two centuries without defaulting on its obligations. So what can the Japanese learn from the two episodes of government de-levering in Great Britain?

First, significant de-levering can take decades. It took 35 years after the Napoleonic Wars for the British government to bring its debt-to-GDP ratio down to the pre-war level. Second, it is not necessary to bring down the absolute amount of debt outstanding to de-lever. The debt-to-GDP ratio can be brought down simply by growing out of the problem (i.e., via nominal GDP growth, which raises the denominator). Fiscal restraint can help hold down the numerator, but it can also be counterproductive if administered too abruptly.

Raising nominal GDP growth seems straightforward in theory but can be difficult to achieve in practice, especially for a country like Japan which faces a number of constraints. Because the population of Japan likely will contract markedly over the next few decades, it will take some combination of higher labor force participation, especially among females, and productivity acceleration to bring about stronger real GDP growth over a sustained period. Higher labor force participation entails less leisure for some individuals, which may not be entirely pleasant for them, and it is not readily apparent how stronger productivity growth is to be achieved.

Higher inflation would help to boost nominal GDP growth, but the BoJ has not had much success engineering higher inflation over the past two decades. However, unless the BoJ totally scraps its view about quantitative easing, which does not seem likely anytime soon, its balance sheet will remain bloated for the foreseeable future. Consequently, JGB yields likely will remain depressed for some time.

Author

Wells Fargo Research Team

Wells Fargo